hbl News

.png)

.jpeg)

.png)

.jpeg)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

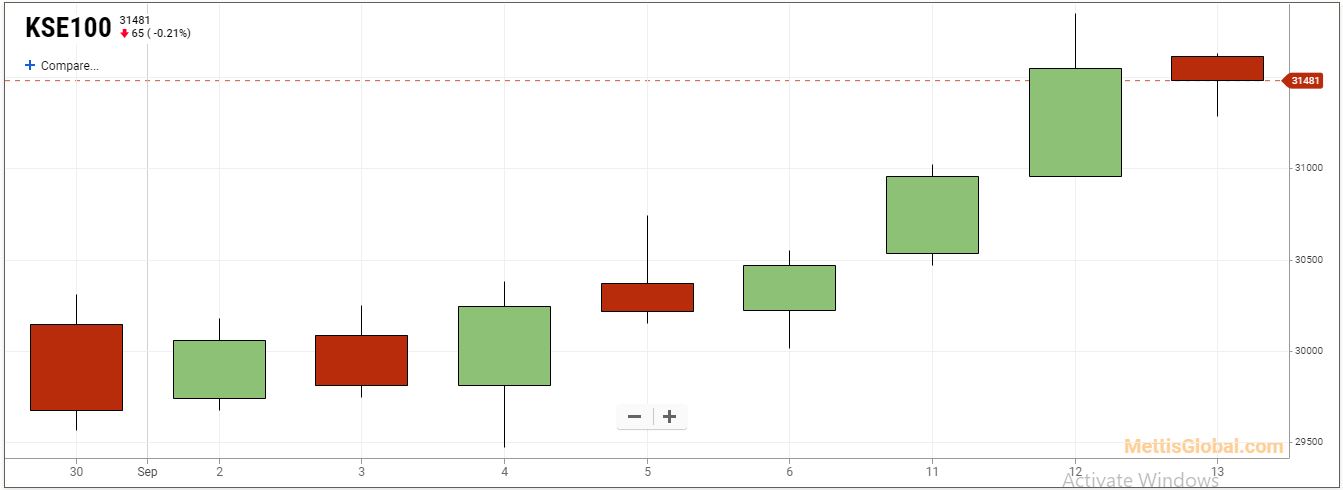

| KSE100 | 136,502.54 259.91M |

1.64% 2202.77 |

| ALLSHR | 85,079.90 838.35M |

1.26% 1061.74 |

| KSE30 | 41,552.62 97.27M |

1.81% 738.33 |

| KMI30 | 193,330.76 84.69M |

0.39% 741.60 |

| KMIALLSHR | 56,315.31 366.02M |

0.43% 243.06 |

| BKTi | 38,498.08 37.91M |

4.13% 1526.33 |

| OGTi | 28,138.38 5.66M |

-0.36% -101.89 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 120,370.00 | 123,615.00 118,675.00 |

1840.00 1.55% |

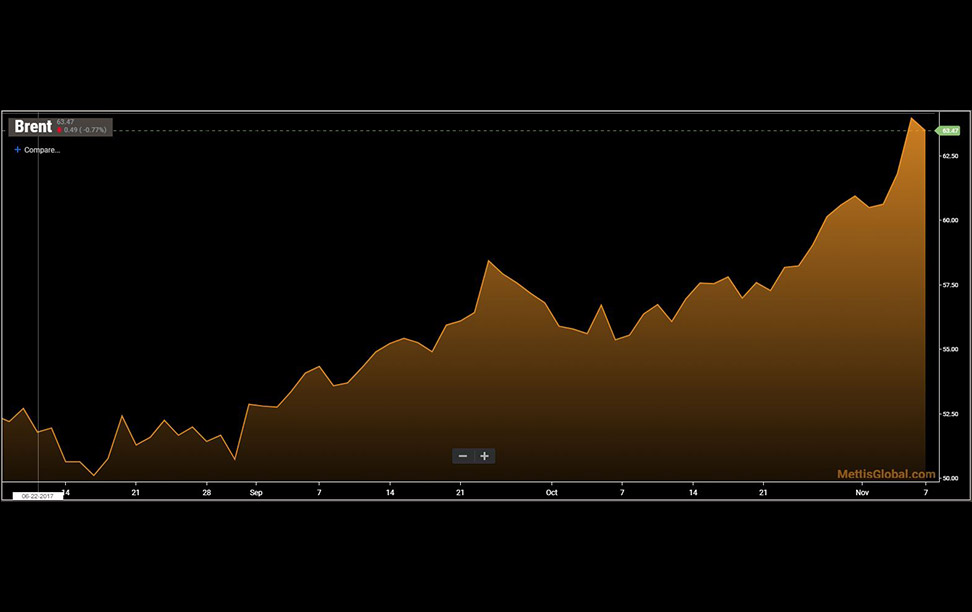

| BRENT CRUDE | 69.16 | 71.53 69.08 |

-1.20 -1.71% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

0.25 0.26% |

| ROTTERDAM COAL MONTHLY | 106.50 | 106.60 106.50 |

-2.20 -2.02% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.90 | 69.65 66.84 |

-1.55 -2.26% |

| SUGAR #11 WORLD | 16.31 | 16.67 16.27 |

-0.26 -1.57% |

Latest News

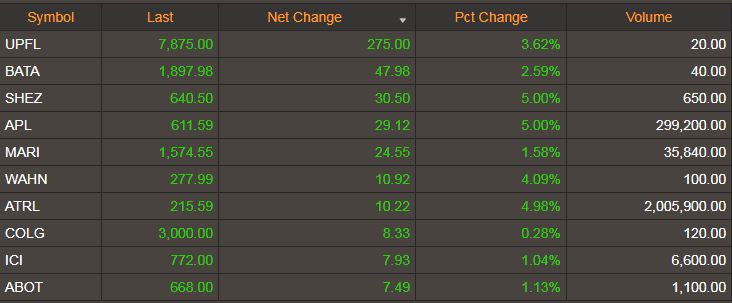

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|---|---|

| 3223 | Pr32ice | Chan2ge |

| Name | Last | Chg/%Chg |

|---|