PKR FY26 Review: A Year of Unbroken Strength

Hafiz Muhammad Abdullah Hashim | July 01, 2026 at 11:27 AM GMT+05:00

July 01, 2026 (MLN): The Pakistani rupee wrapped up fiscal year 2026 as one of the best-performing and most stable currencies in the region, extending its longest winning streak on record against the US Dollar.

The Pakistani rupee closed fiscal year 2026 at 278.16

against the US Dollar, an improvement of Rs5.60 or 2.01% compared to the

closing rate of 283.76 for FY25.

This marks PKR's strongest and steadiest fiscal-year

performance in over a decade, as the currency became the only unit in the past

13 fiscal years to post gains in all 12 months of the year July through June

without a single monthly decline.

The rupee's appreciation this year was not the product of a

few sharp swings but a prolonged, uninterrupted winning streak. By the close of

the fiscal year, PKR had strengthened for 187 consecutive interbank sessions

against the Dollar, an unmatched run compared to the sharp volatility seen in

years such as FY22 and FY23, when the currency lost 23.09% and 28.37%

respectively over the same 12-month span.

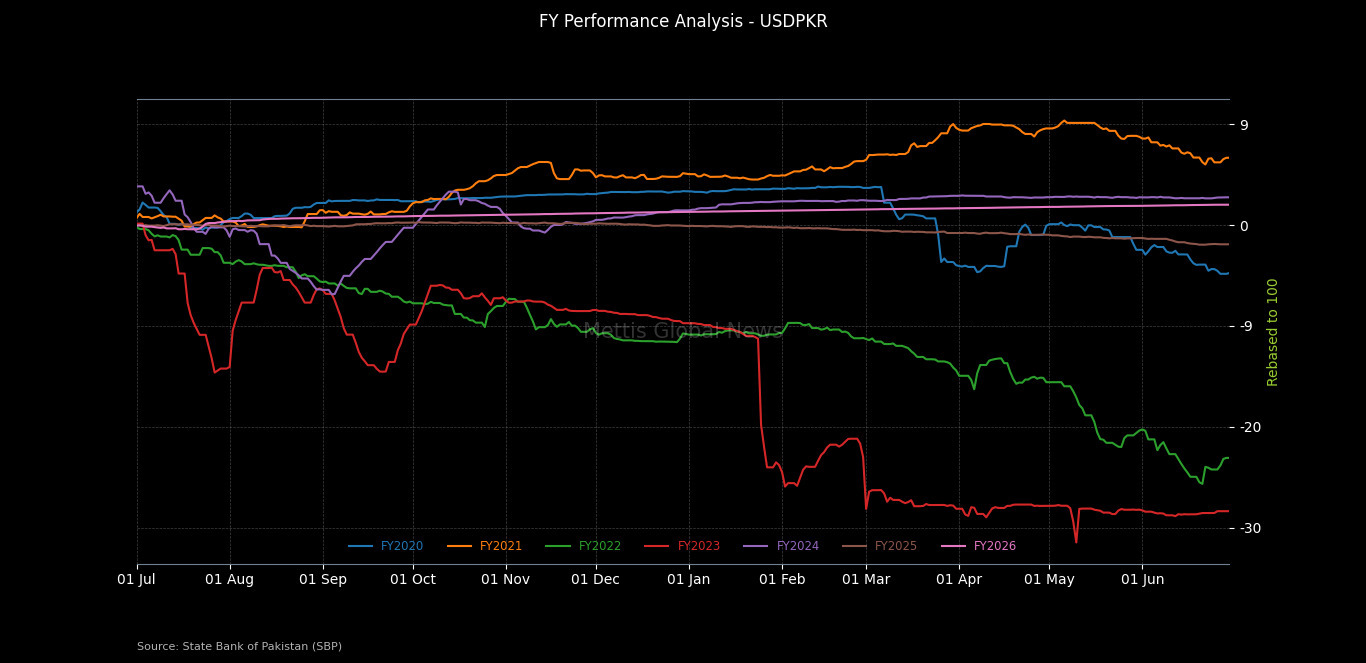

Fiscal-Year comparison

A comparison of fiscal-year performance trends since FY2020

highlights just how distinct FY26 has been.

On a rebased-to-100 basis, the rupee's FY26 trajectory

traces a smooth, near-uninterrupted upward path from July through June, moving

in a narrow band without any sharp reversals throughout the year.

The rupee's appreciation this year was not the product of a

few sharp swings but a prolonged, uninterrupted winning streak.

By the close of the fiscal year, PKR had strengthened for

187 consecutive interbank sessions against the Dollar, an unmatched run

compared to the sharp volatility seen in years such as FY22 and FY23, when the

currency lost 23.09% and 28.37% respectively over the same 12-month span.

This stands in contrast to FY2023, which recorded the most

volatile path in the six-year comparison a steep decline through

July-September, a brief recovery into October, followed by a sharp collapse in

late January that pushed the currency to its steepest point of weakness for the

period, before stabilizing at a depreciated level through the rest of the year.

FY2022 also shows a pattern of sustained and continuous

weakening, extending from July through June without any meaningful recovery

phase.

FY2021 followed an opposite trajectory, climbing steadily

from the early months and accelerating through February-April before easing

slightly into June. FY2020 remained comparatively range-bound for most of the

year before a sharp shift around February-March, followed by a partial

recovery.

FY2024 and FY2025 both stayed closer to the zero line

throughout their respective years, showing relatively lower volatility

compared to FY2021-FY2023, though neither matched the consistency of FY26's

performance.

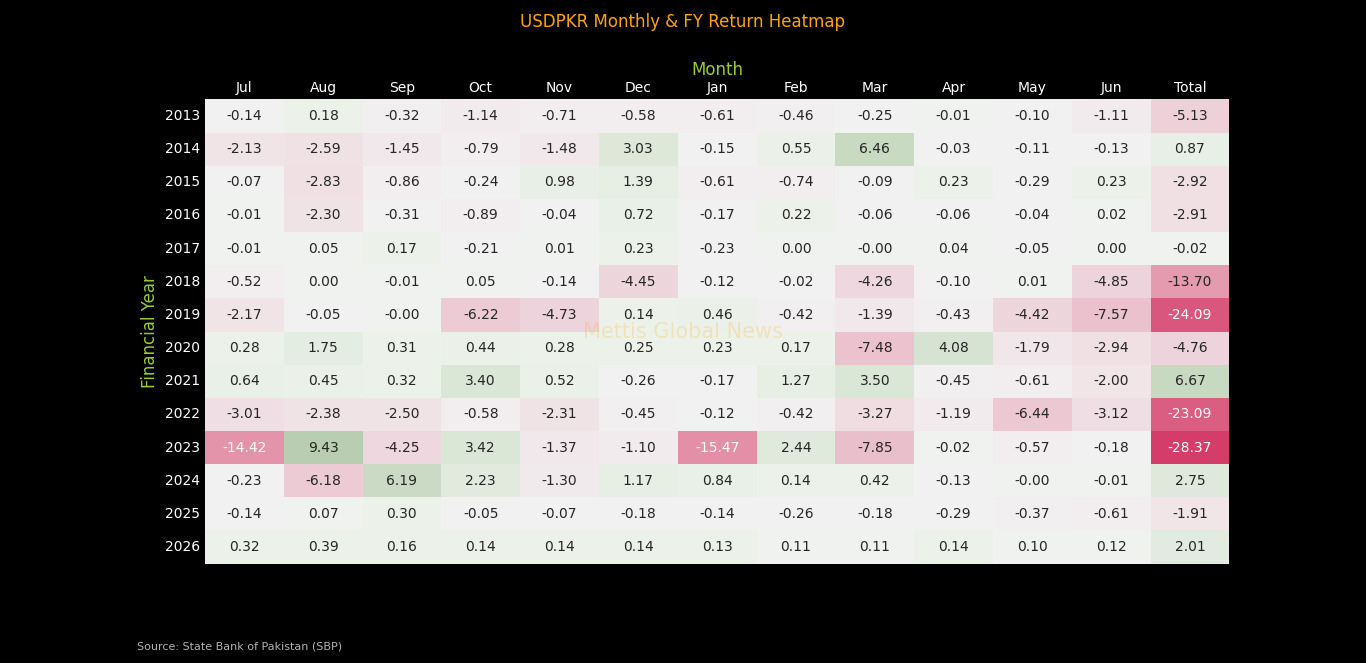

Historical comparison

The monthly and fiscal-year return heatmap spanning FY2013

to FY2026 places this year's performance in a clearer historical context.

Across the past 13 fiscal years, every single year recorded

at least one month, and in most cases several months, of rupee depreciation

against the Dollar.

FY2026 stands alone as the only year in this entire dataset

with a clean sweep of positive months Jul (0.32%), Aug (0.39%), Sep (0.16%),

Oct (0.14%), Nov (0.14%), Dec (0.14%), Jan (0.13%), Feb (0.11%), Mar (0.11%),

Apr (0.14%), May (0.10%), and Jun (0.12%) compounding to a full fiscal-year

gain of 2.01%.

By comparison, FY2023 delivered the worst single-month

reading in the dataset, with a 15.47% plunge in January alone, part of a

cumulative annual loss of 28.37% the steepest fiscal-year decline on record.

FY2019 followed with a 24.09% annual loss, driven by heavy

monthly declines including a 7.57% drop in May and a 6.22% fall in October.

FY2018 and FY2022 also posted double-digit annual losses of

13.70% and 23.09%, respectively, showing sustained periods of currency

weakness.

Even in years where the rupee ultimately closed higher, such

as FY2021 (up 6.67%) and FY2024 (up 2.75%), the path to that gain was uneven,

with individual months such as March 2021 (-3.27%) or August 2024 (-6.18%)

still registering losses along the way.

This makes FY2026 the first fiscal year in over a decade

where the rupee's appreciation was not interrupted by a single negative month, emphasizing the consistency behind this year's performance rather than any

one-off rally._20260701055123073_0805c7.jpeg)

Performance against other currencies

The rupee's gains during FY26 extended across most major

currencies, though the strength was not uniform. Against the Euro, PKR

appreciated by Rs15.73 or 4.96% over the fiscal year, while it gained Rs20.84

or 5.66% against the British Pound.

The currency advanced Rs11.71 or 3.41% against the Swiss

Franc and strengthened by 14.94% against the Japanese Yen, its sharpest gain

among major currencies.

Against regional and Gulf currencies, the rupee firmed by

Rs1.59 or 2.15% against the Saudi Riyal and by Rs1.53 or 2.02% against the UAE

Dirham.

The Chinese Yuan was the exception, with the rupee losing

Rs1.39 or 3.40% against it over the fiscal year — the only major currency

against which PKR depreciated during FY26.

Key drivers

Workers'

remittances reinforced the currency's external position, with the 11MFY26

tally reaching Rs38.1bn, up 3.8% YoY, providing sustained dollar inflows

through formal channels.

The

current account posted a surplus of Rs255m in 11MFY26, narrowing from Rs1.62bn

in the same period last year, though remaining in positive territory.

Economic activity picked up pace, with GDP growing 3.7% YoY

in FY26, led by the industrial sector at 3.5%, services at 3.1%, and

agriculture at 2.9%.

Inflation

averaged 6.7% in 11MFY26 against 4.6% in the same period last year, with

the uptick attributed to rising oil prices amid escalating geopolitical

tensions.

The State Bank of Pakistan held the policy rate at 11.0%

through most of the first half of FY26, before a 50bps cut in December 2025 on

the back of contained inflation and improving economic activity.

A resurgence in inflationary pressure, driven by higher oil

prices, prompted a 100bps hike in May 2026, after which the rate was held unchanged

in June, closing the fiscal year at 11.5%.

Record remittances

exceeding Rs38bn, a stronger external account, continued support under the

IMF program, and sovereign credit rating upgrades reinforced macroeconomic

stability through the year, while market liquidity remained robust on the back

of strong participation from both institutional and retail investors.

Progress on power sector reforms, privatization, taxation

measures, and development at the Reko Diq project further strengthened the

investment outlook.

Despite intermittent volatility stemming from tensions in

the Middle East, investor sentiment stayed resilient as geopolitical risks

eased and lower oil prices improved the inflation and external account outlook.

Pakistan's diplomatic role as a mediator between the United

States and Iran, including hosting talks in Islamabad that helped bring about a

ceasefire, further supported the country's regional standing and added to

overall confidence during the period.

Political stability, the successful FY27 budget, and a

decline in Pakistan's CDS-implied default probability added to overall

confidence.

Going forward, structural reforms, rising foreign direct

investment, continued engagement with the IMF, and the government's shift from

stabilization toward growth are expected to support corporate earnings in the

year ahead.

Outlook

The rupee enters FY27 on a firmer footing than it has in

years, with the stability built through FY26 setting a constructive tone for

the period ahead.

Continued engagement with the IMF, sustained remittance

inflows, and a government increasingly focused on growth rather than crisis

management are expected to keep the external account anchored.

Progress on structural reforms, privatization, and

large-scale investment projects should further reinforce confidence, while

improving credit ratings and a declining default risk profile point to a

steadily strengthening macroeconomic base.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,965.00 | 65,570.00 63,875.00 | 750.00 1.17% |

| BRENT CRUDE | 92.41 | 93.60 89.58 | -4.37 -4.52% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 0.00 0.00 | 0.85 0.71% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 85.03 | 86.20 83.10 | -4.28 -4.79% |

| SUGAR #11 WORLD | 14.76 | 0.00 0.00 | -0.01 -0.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|