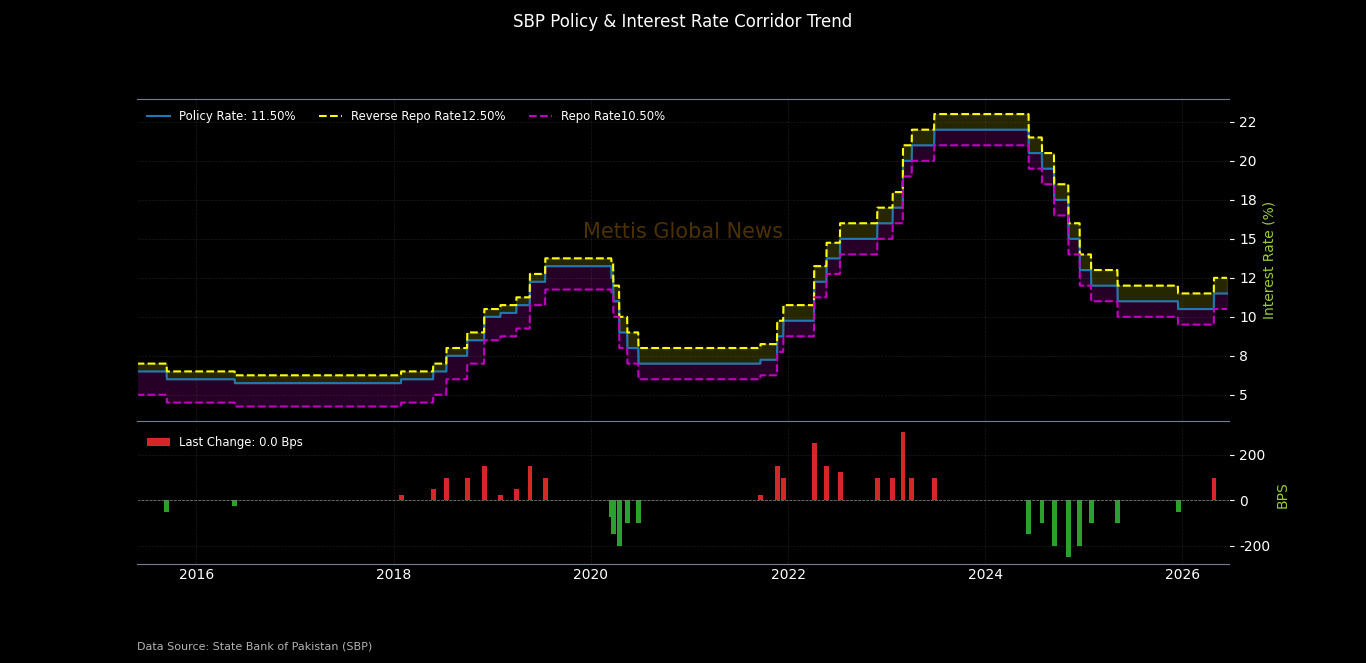

SBP keeps policy rate unchanged at 11.5%

MG News | June 15, 2026 at 03:43 PM GMT+05:00

June 15, 2026 (MLN): The Monetary Policy Committee decided to keep the

policy rate unchanged at 11.5% in its meeting held on June 15, 2026.

The Committee noted that global oil prices have eased following recent positive geopolitical developments, though they remain elevated compared to pre-conflict levels.

As

anticipated in the previous meeting, the impact of the Middle East conflict is

now visible in key economic indicators, with headline inflation rising to

double digits in April and May and core inflation also edging up.

Economic activity is showing signs of moderation amid elevated prices, austerity measures, and prevailing uncertainty, while external account pressures remain moderate.

Having evaluated these developments, the MPC observed that the macroeconomic

outlook is broadly unchanged from its last meeting and assessed that the

current monetary policy stance remains appropriate to guide inflation toward

the medium-term target range of 5-7%.

The Committee

highlighted several key developments since its last meeting.

Real GDP growth for

FY26 has been provisionally estimated by the PBS at 3.7%, up from 3.2% in FY25.

Consumer and business confidence recovered marginally in the latest sentiment

surveys, with inflation expectations easing somewhat.

The successful

completion of IMF reviews under the EFF and RSF programmes, along with ongoing

purchases, lifted SBP's FX reserves to $17.2 billion as of June 5, 2026. The

government has estimated a primary balance surplus of 2.5% of GDP for FY26 and

is targeting 2.0% of GDP for FY27.

The MPC also noted

that the Middle East conflict has begun affecting macroeconomic conditions

across economies, prompting a rising number of central banks to raise policy

rates.

The MPC said

proactive macroeconomic management, underpinned by forward-looking monetary

policy and consistent fiscal consolidation, has helped sustain stability

despite the prolonged conflict.

The Committee

reiterated the need to accelerate structural reforms to strengthen the

economy's resilience to supply shocks, enhance productivity, and support

higher, more sustainable growth.

Real Sector

According to

provisional PBS estimates, real GDP grew by 3.7% in FY26, up from 3.2% in FY25.

The MPC noted this reflects the impact of the Middle East conflict and

austerity measures, with pre-conflict growth momentum having been notably

higher.

Growth was primarily

driven by the services and industry sectors, with a meaningful contribution

from agriculture.

Large-scale

manufacturing posted growth of 6.5% during July-March FY26, though it is

expected to moderate in Q4-FY26 based on recent high-frequency indicators.

The MPC expects

spillover from the conflict to continue moderating industrial and services

activity in the coming months, while subdued agriculture prospects amid

challenging weather conditions for the Kharif crop may weigh on the FY27 growth

outlook.

External Sector

The current account

turned into a deficit of $0.3 billion in April, taking the cumulative deficit

to $0.2 billion during July-April FY26, mainly due to a widening trade deficit

amid a surge in energy imports that offset resilient workers' remittances.

Sizable remittances

during May are likely to keep the FY26 current account deficit near the lower

end of the earlier projected range.

Increased official

inflows provided critical support in meeting external obligations, facilitating

ongoing FX purchases and a buildup in reserves, which are projected to reach

$18 billion by end-June 2026.

Despite some

expected widening in the FY27 current account deficit, the MPC said reserve

buildup is expected to continue through FX purchases and timely realisation of

planned official inflows.

Fiscal Sector

Fiscal consolidation

remained broadly on track during July-March FY26, primarily driven by

expenditure restraint, even as revenue growth moderated compared to the same

period last year.

The FBR has revised

its FY26 target to around Rs13 trillion.

Despite the downward

revision, the government expects to achieve a primary balance surplus of 2.5%

of GDP for FY26 by containing expenditures, and is targeting 2.0% of GDP for

FY27.

The MPC emphasized

the importance of continued fiscal consolidation and reiterated the need for

timely structural reforms, particularly broadening the tax base and reforming

public sector enterprises.

Money and Credit

Broad money (M2)

growth moderated to 14.3% y/y as of May 29, 2026, from 14.5% on April 10,

entirely due to a deceleration in NDA growth reflecting lower net budgetary

borrowing from the banking system.

Private sector

credit grew by around 13%, with increases across working capital, fixed

investment and consumer financing, while improvement in the external position

accelerated NFA growth.

Currency in

circulation growth rose, partly reflecting seasonal Eid-related cash

withdrawals, pushing up the currency-to-deposit ratio.

Inflation

Headline inflation

rose sharply from 7.3% in March to 10.9% in April and 11.7% in May, driven by

base effects as well as the direct and indirect impact of the Middle East

conflict on energy, transportation and production costs.

Core inflation rose

to 8.2% in April and 8.7% in May, while an unanticipated surge in wheat and

wheat product prices pushed up food inflation significantly over the last two

months.

The MPC assessed

that inflation may remain in double digits for the next few months before

gradually easing, with the outlook subject to risks including geopolitical

developments, the pass-through of global prices to domestic fuel, adjustments

in power and gas tariffs, potential fiscal slippages, and weather-related food

price uncertainty.

Copyright Mettis Link News

Related News

_20251223102454789_a58e54.webp?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,846.68 370.24M | -0.81% -1463.60 |

| ALLSHR | 108,777.96 842.70M | -0.57% -624.36 |

| KSE30 | 53,571.08 118.45M | -0.81% -434.78 |

| KMI30 | 253,007.72 126.35M | -1.06% -2717.47 |

| KMIALLSHR | 69,727.55 549.62M | -0.70% -488.73 |

| BKTi | 52,178.22 35.92M | -0.12% -62.01 |

| OGTi | 35,518.90 13.54M | -0.77% -274.36 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,775.00 | 64,610.00 63,260.00 | -345.00 -0.54% |

| BRENT CRUDE | 89.14 | 90.03 86.60 | 1.42 1.62% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -4.00 -3.65% |

| ROTTERDAM COAL MONTHLY | 122.00 | 122.00 122.00 | 0.75 0.62% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.40 | 84.61 81.27 | 1.27 1.55% |

| SUGAR #11 WORLD | 16.74 | 16.75 16.33 | 0.27 1.64% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|