CPI Preview: Inflation to soar past 30% in December

Abdur Rahman | December 26, 2023 at 04:52 PM GMT+05:00

December 26, 2023 (MLN): December’s inflation is expected to surge above the 30% mark, as the impact of the recent gas price hike and the unfavorable base effect continue to weigh on the consumer price index (CPI).

The headline inflation for December is anticipated to settle at around 30.11% YoY and 1.18% MoM compared to the previous month’s 29.2% YoY and 2.7% MoM.

This monthly inflation pace would be far below the 12-month average of 2.17% MoM.

Accordingly, this will take the average yearly inflation of 6MFY24 to 28.87% YoY compared to 25.05% YoY in 6MFY23.

This jump is fueled by the unfavorable base effect and the surge in gas prices, which were not fully felt in the previous month.

| National Consumer Price Index | ||||||

|---|---|---|---|---|---|---|

| Dec 2023E | Indices | |||||

| Weight | YoY | MoM | Dec-2023E | Nov-2023 | Dec-2022 | |

| Headline CPI | 100% | 30.11% | 1.18% | 256.13 | 253.15 | 196.86 |

| Food & Non-alcoholic Bev. | 34.58% | 27.76% | -0.29% | 282.13 | 282.95 | 220.82 |

| Alcoholic Bev.& Tobacco | 1.02% | 81.77% | -0.07% | 362.61 | 362.87 | 199.49 |

| Clothing & Footwear | 8.60% | 20.24% | 0.18% | 220.78 | 220.38 | 183.62 |

| Housing, Water, Electricity, Gas & Fuels | 23.63% | 41.18% | 6.19% | 236.49 | 222.69 | 167.51 |

| Furnishing & Household Equipment Maintenance | 4.10% | 31.34% | 0.00% | 258.02 | 258.02 | 196.45 |

| Health | 2.79% | 22.25% | -0.20% | 231.82 | 232.28 | 189.63 |

| Transport | 5.91% | 22.41% | -4.04% | 297.81 | 310.34 | 243.28 |

| Communication | 2.21% | 7.25% | -0.08% | 120.08 | 120.18 | 111.96 |

| Recreation & Culture | 1.59% | 38.29% | -0.11% | 255.86 | 256.14 | 185.02 |

| Education | 3.79% | 13.34% | 0.07% | 185.75 | 185.62 | 163.89 |

| Restaurants & Hotels | 6.92% | 30.42% | 0.49% | 259.58 | 258.31 | 199.03 |

| Miscellaneous | 4.87% | 30.66% | 0.25% | 267.83 | 267.18 | 204.99 |

On the other hand, food inflation is anticipated to record a marginal decline of 0.29% MoM, primarily driven by the fall in prices of Tomatoes, Potatoes, Chicken, and Oil.

Moreover, the transport index is projected to experience around a 4% MoM decrease, primarily attributed to the relief in petrol and HSD prices.

Outlook

After December, inflation is anticipated to start declining at a comparatively faster pace on the back of favorable base effect, lagged impact of monetary tightening, and other administrative measures.

The December's increase is attributed to the remaining effect of the long-overdue gas price hike.

It is important to mention that unforeseen climate events, volatility in global commodity prices, especially oil, and external account pressures are some important upside risks to the inflation outlook.

Global oil prices are starting to climb back up amid red sea shipping woes, which can pose a threat to the inflation outlook.

Furthermore, the successful completion of the IMF review, along with additional loan programs, is crucial.

The remaining amount of $1.8bn under the SBA is still yet to be released.

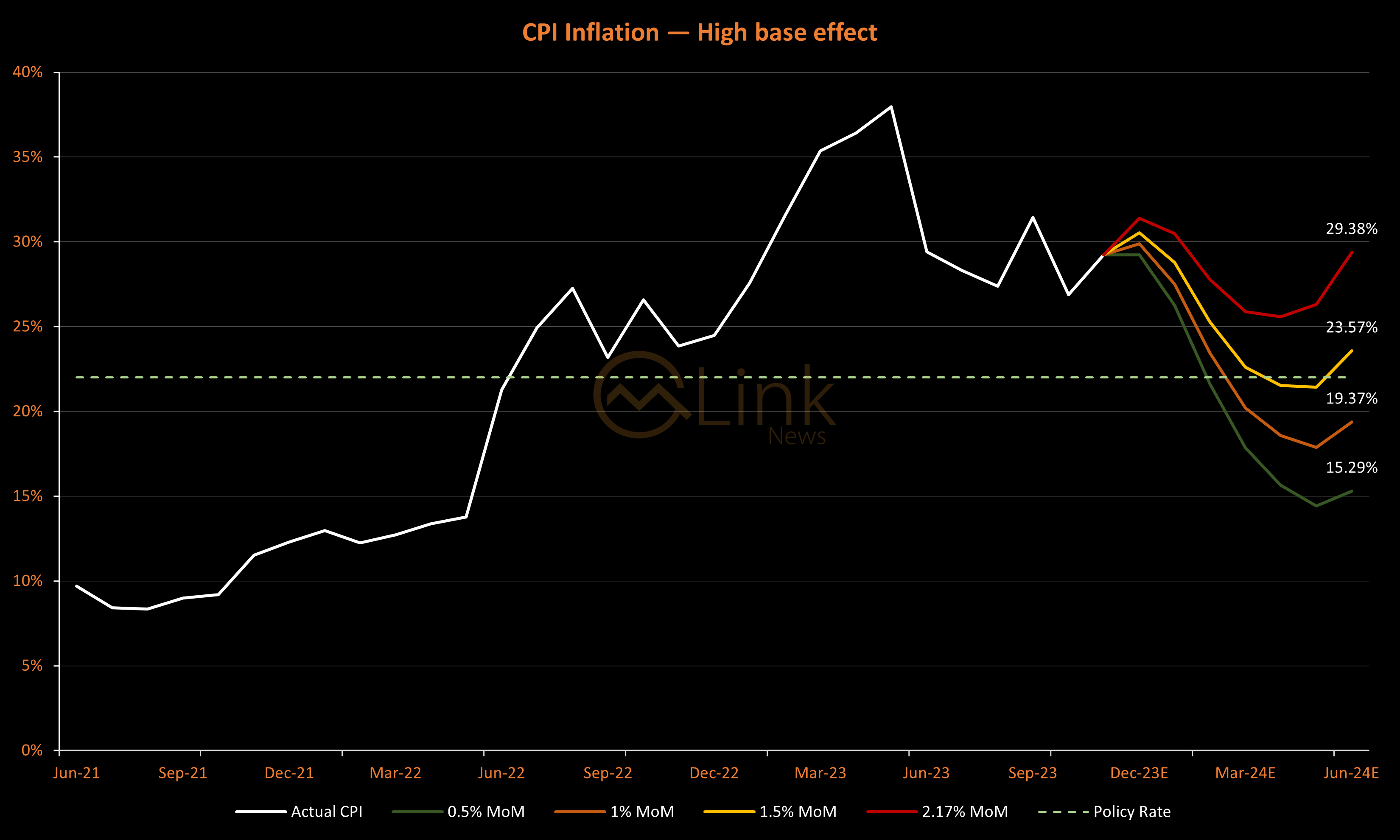

High Base Effect

The following chart maps out the yearly inflation trajectory if 0.5%, 1%, 1.5%, and the 12-month average of 2.17% MoM is taken.

At 0.5% and 1% MoM CPI, yearly inflation will drop below the 22% policy rate by February-March 2024.

Meanwhile, by the end of FY24, with 0.5% and 1% MoM CPI, it will decline towards 15.29% and 19.37% respectively, significantly up from the last month's forecasts of 12.9% and 17.5%.

If the last 12-month average of 2.17% MoM is taken, it shows that the real interest rate would still remain in negative territory by the end of FY24.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,846.68 370.24M | -0.81% -1463.60 |

| ALLSHR | 108,777.96 842.70M | -0.57% -624.36 |

| KSE30 | 53,571.08 118.45M | -0.81% -434.78 |

| KMI30 | 253,007.72 126.35M | -1.06% -2717.47 |

| KMIALLSHR | 69,727.55 549.62M | -0.70% -488.73 |

| BKTi | 52,178.22 35.92M | -0.12% -62.01 |

| OGTi | 35,518.90 13.54M | -0.77% -274.36 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,800.00 | 63,810.00 63,760.00 | 200.00 0.31% |

| BRENT CRUDE | 89.35 | 90.03 86.60 | 1.63 1.86% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -4.00 -3.65% |

| ROTTERDAM COAL MONTHLY | 122.00 | 122.00 122.00 | 0.75 0.62% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.23 | 84.61 81.27 | 1.10 1.34% |

| SUGAR #11 WORLD | 16.74 | 16.75 16.33 | 0.27 1.64% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|