CPI Preview: Gas price surge to push inflation above 28%

Abdur Rahman | November 27, 2023 at 11:15 AM GMT+05:00

November 27, 2023 (MLN): The relief that the masses had just started to feel from the surging inflation last month now faces uncertainty, at least for November, as this month brings another wave of inflationary pressure on the back of a long-overdue gas price hike.

The headline inflation for November is anticipated to settle at around 28.73% YoY and 2.2% MoM compared to the previous month’s 26.9% YoY and 1.1% MoM.

November's monthly inflation pace surpasses the 12-month average of 2.01% MoM.

Accordingly, this will take the average yearly inflation of 5MFY24 to 28.54% YoY compared to 25.16% YoY in 5MFY23.

This jump is fueled by the surge in gas prices, compounded by the heightened costs of other key inflation components.

| National Consumer Price Index | ||||||

|---|---|---|---|---|---|---|

| Nov 2023E | Indices | |||||

| Weight | YoY | MoM | Nov-2023E | Oct-2023 | Nov-2022 | |

| Headline CPI | 100% | 28.73% | 2.22% | 252.18 | 246.69 | 195.89 |

| Food & Non-alcoholic Bev. | 34.58% | 29.63% | 2.28% | 286.66 | 280.27 | 221.14 |

| Alcoholic Bev.& Tobacco | 1.02% | 83.85% | 0.73% | 364.88 | 362.24 | 198.46 |

| Clothing & Footwear | 8.60% | 18.77% | 0.57% | 216.54 | 215.31 | 182.32 |

| Housing, Water, Electricity, Gas & Fuels | 23.63% | 27.67% | 6.54% | 213.82 | 200.7 | 167.48 |

| Furnishing & Household Equipment Maintenance | 4.10% | 33.37% | 0.00% | 255.85 | 255.85 | 191.84 |

| Health | 2.79% | 22.56% | -0.20% | 227.98 | 228.44 | 186.02 |

| Transport | 5.91% | 27.24% | -3.18% | 312.07 | 322.33 | 245.27 |

| Communication | 2.21% | 8.02% | 0.66% | 120.86 | 120.07 | 111.89 |

| Recreation & Culture | 1.59% | 54.67% | 0.87% | 258.00 | 255.78 | 166.8 |

| Education | 3.79% | 11.59% | -0.73% | 182.40 | 183.74 | 163.45 |

| Restaurants & Hotels | 6.92% | 31.05% | 0.40% | 257.52 | 256.5 | 196.51 |

| Miscellaneous | 4.87% | 32.15% | 0.00% | 263.00 | 263 | 199.01 |

The SPI data released by the Pakistan Bureau of Statistics (PBS) this month showed that gas prices skyrocketed 480% to Rs1,711/mmbtu, from Rs295/mmbtu last month.

Moreover, food inflation is also anticipated to record a significant jump of 2.28% MoM, primarily driven by the inflated prices of Tomatoes, Onions, Potatoes, Eggs, Tea, and Chicken.

On the flip side, the transport index is projected to experience around a 3.2% MoM decrease, primarily attributed to the relief in petrol and HSD prices.

Nevertheless, it is important to highlight that inflation has been on a downward trajectory since reaching its peak in May 2023, and the economy has started to show some early signs of improvement following a rough year.

In a recent development, Pakistan has secured initial approval from the International Monetary Fund (IMF) for the release of the next loan tranche under the current $3bn loan program.

To note, towards the end of FY23, the IMF being a last resort saved Pakistan from a sovereign debt default with a $3bn Stand-by Arrangement (SBA).

The initial disbursement of $1.2bn from the IMF, alongside $3bn bilateral inflows from the Arab countries gave a substantial boost to the depleting foreign reserves held by the country.

Consequently, in the current fiscal year, total liquid foreign reserves have increased by $3.14bn or 34.3%.

Moreover, the caretaker finance minister, Dr. Shamshad Akhtar has hinted at Pakistan receiving funds worth $1.5 billion from global lenders upon the IMF's approval of the loan tranche.

Additionally, the government-backed administrative measures have helped the Pakistani Rupee (PKR) to completely recover all year-to-date losses against the USD and strengthen significantly to 285.4 per USD.

To recall, Pakistan’s economy faced multifaceted challenges in the latter half of FY22 and throughout FY23 owing to higher global commodity prices, strong global inflation, second-round effects, continuous PKR depreciation, supply chain disruptions due to floods, soaring trade deficits, and rapid reserve depletion.

The impact of these challenges pushed the CPI inflation to a multi-decade high of 29.2% during FY23.

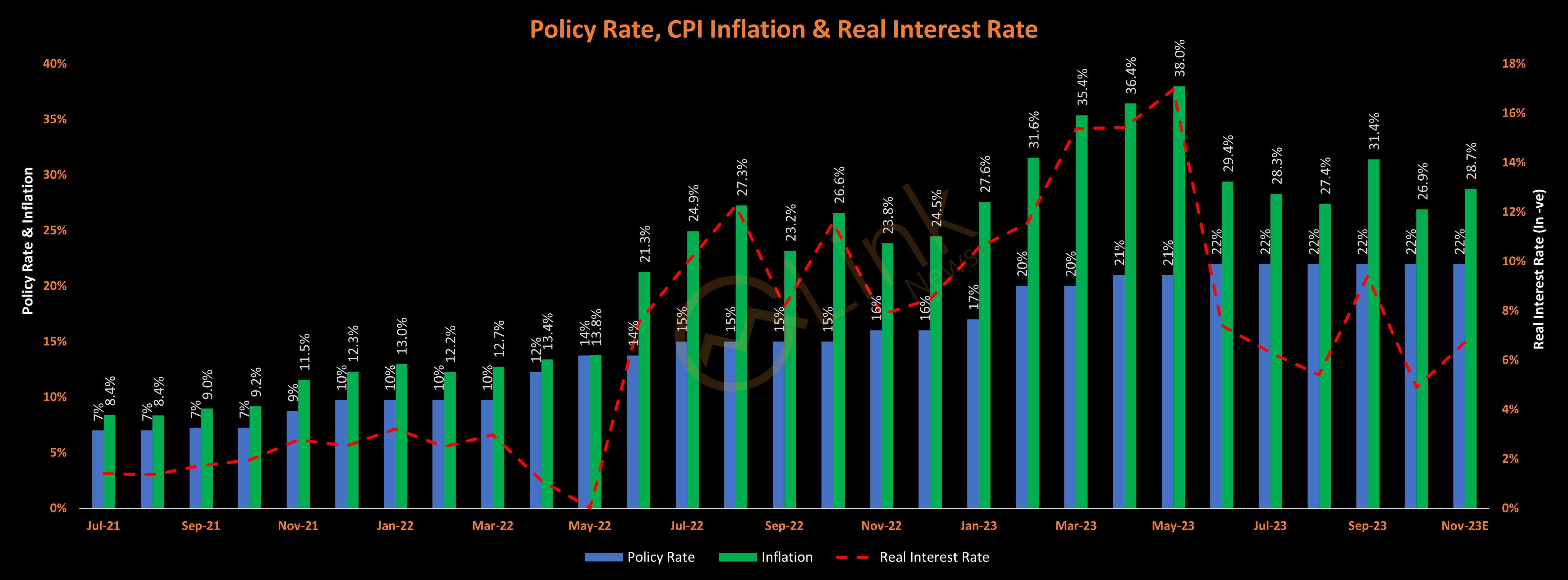

On the policy front, the State Bank of Pakistan (SBP) responded to these escalating macroeconomic challenges by continuing the contractionary monetary policy that it had started in September 2021.

Resultantly, the SBP raised the policy rate by a cumulative 825 basis points (bps) during FY23, on top of a 675 bps increase in the previous fiscal year.

While the cumulative increase in the policy rate since September 2021, when the SBP started contracting the economy is 1,500bps, taking the policy rate from 7% to 22%.

Though the central bank has now kept the policy rate unchanged at 22% since June 2023, foreseeing a downward trend in inflation.

Outlook

After November, inflation is anticipated to continue to start steadily declining on the back of the high base effect, lagged impact of monetary tightening, and other administrative measures.

The November's surge is attributed to a long-overdue gas price hike that the government had previously failed to implement.

Additionally, a steadier decrease is projected for the second half of FY24, starting from January.

It is important to mention that unforeseen climate events, volatility in global commodity prices, especially oil, and external account pressures are some important upside risks to the inflation outlook.

Furthermore, the successful completion of the IMF review, along with additional loan programs, is crucial.

The remaining amount of $1.8bn under the SBA is still yet to be released, with around $700m set to be unlocked by around December.

High Base Effect

The following chart maps out the yearly inflation trajectory if 0.5%, 1%, 1.5%, and the 12-month average of 2.01% MoM is taken.

This is what is referred to as the — high base effect.

At 0.5% and 1% MoM CPI, yearly inflation will drop below the 22% policy rate by February 2024.

Moreover, by the end of FY24, with 0.5% and 1% MoM CPI, it will decline towards 12.9% and 17.5% respectively.

Meanwhile, if the last 12-month average of 2.01% MoM is taken, it shows that the real interest rate would still remain in negative territory by the end of FY24.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,485.78 112.17M | -0.16% -290.82 |

| ALLSHR | 109,289.27 238.82M | -0.02% -19.22 |

| KSE30 | 54,261.92 44.17M | -0.24% -129.91 |

| KMI30 | 255,568.05 34.21M | -0.22% -566.72 |

| KMIALLSHR | 69,995.45 134.79M | -0.04% -28.89 |

| BKTi | 52,352.53 17.74M | -0.03% -15.19 |

| OGTi | 35,381.16 2.71M | 0.22% 78.34 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,350.00 | 64,685.00 64,290.00 | -270.00 -0.42% |

| BRENT CRUDE | 83.75 | 84.44 83.06 | 1.26 1.53% |

| RICHARDS BAY COAL MONTHLY | 107.75 | 0.00 0.00 | 2.20 2.08% |

| ROTTERDAM COAL MONTHLY | 116.25 | 116.50 116.25 | 0.20 0.17% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 78.26 | 78.77 77.73 | 0.97 1.26% |

| SUGAR #11 WORLD | 15.58 | 15.60 14.98 | 0.43 2.84% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|