NCCPL to collect up to 50% CGT from clearing members, PMEX on September 12

MG News | September 05, 2023 at 03:53 PM GMT+05:00

September 05, 2023 (MLN): National Clearing Company of Pakistan Limited (NCCPL) will collect Capital Gain Tax (CGT) from Clearing Members and the Pakistan Mercantile Exchange by up to 50% on September 12.

The maximum applicable CGT of 50% is for company-owned funds that are classified under the Mutual Funds Association Of Pakistan (MUFAP).

The aggregate amount of Capital Gain Tax (CGT) arising on the disposal of shares at the Pakistan Stock Exchange for the period July 01, 2023, to July 31, 2023, through respective settling banks of the Clearing Members.

Further, the aggregate amount of CGT arising on the trading of future commodity contracts at the Pakistan Mercantile Exchange for the same period would also be collected from the Pakistan Mercantile Exchange on the said date.

Moreover, the aggregate amount of CGT arising on redemption of units of open-end mutual funds has also been finalized for the period.

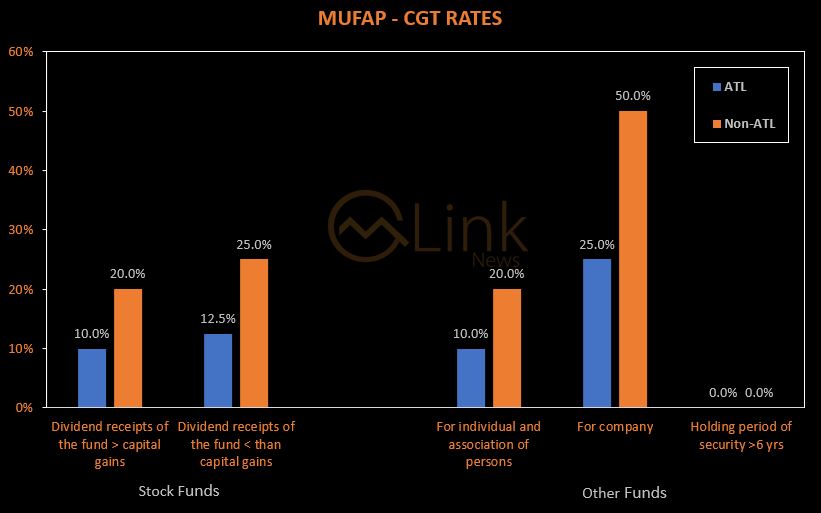

CGT Rates

The rate of 0% tax shall be charged on capital gain arising on disposal where the securities are acquired before the first day of July 2013.

Further, the applicable capital gain tax rates effective from July 01, 2023, are reproduced below for ready reference:

.png)

Additionally, for PMEX Future commodity contracts entered into by members of Pakistan Mercantile Exchange, 5% for ATL and 10% for Non ATL.

Except for PMEX and MUFAP:

- The reduced rates of tax on capital gain arising on disposal shall apply where the securities are acquired on or after the first day of July, 2022; and

- The rate of 12.5% tax shall be charged on capital gain arising on disposal where the securities are acquired on or after the first day of July, 2013 but on or before the 30th day of June, 2022.

Super Tax on Capital Gains (For All Markets)

NCCPL shall also compute and collect Super Tax under section 4C at the rates specified in Division IIB of Part I of the First Schedule on the amount of capital gains computed as below:

.png)

Super tax will be computed and collected if net capital gain of an investor exceeds above mentioned threshold.

If net capital gain is further increased or decreased in following months, super tax will be re-computed and differential tax amount will be collected or refunded.

Copyright Mettis Link News

Related News

_20260529073616622_a5048c_20260724102330512_417f90.webp?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 177,484.73 442.49M | -0.44% -777.60 |

| ALLSHR | 107,418.71 864.89M | -0.39% -418.73 |

| KSE30 | 53,079.95 103.93M | -0.50% -267.72 |

| KMI30 | 250,561.68 138.07M | -0.38% -948.68 |

| KMIALLSHR | 68,927.90 563.21M | -0.36% -245.96 |

| BKTi | 50,733.20 19.97M | -0.65% -331.53 |

| OGTi | 34,999.13 5.62M | -0.71% -249.29 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,465.00 | 64,810.00 63,035.00 | -1500.00 -2.31% |

| BRENT CRUDE | 85.93 | 88.06 84.70 | -2.43 -2.75% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 120.00 | 0.00 0.00 | 0.25 0.21% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 80.70 | 82.43 79.80 | -1.91 -2.31% |

| SUGAR #11 WORLD | 14.57 | 14.70 14.54 | -0.01 -0.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|