The higher oil climbs, the harder Pakistan’s market falls

MG News | May 25, 2026 at 02:29 PM GMT+05:00

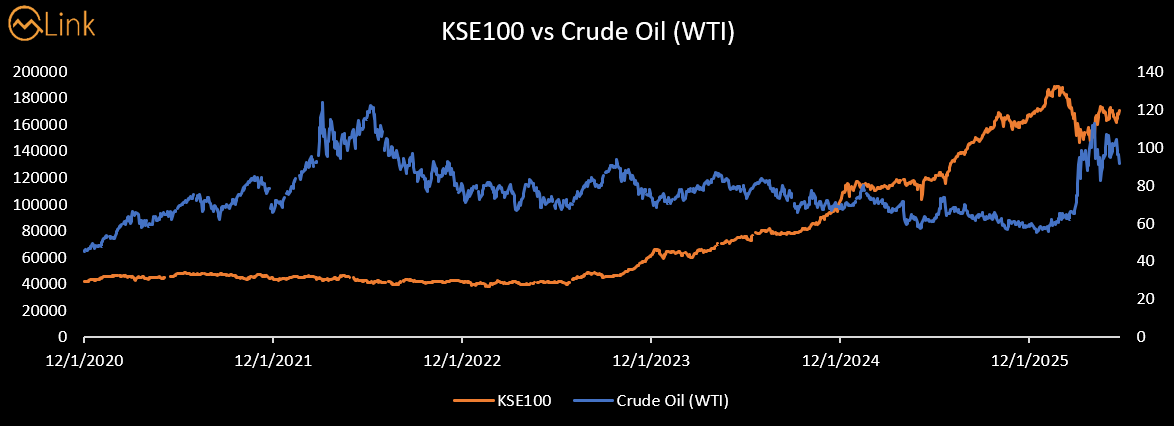

May 25, 2026 (MLN): The Pakistan Stock Exchange's benchmark KSE-100 index has delivered one of the most spectacular emerging-market returns of the past half-decade. Since December 2020, the index has gained more than 300%, transforming it into a global outlier at a time when most frontier and emerging markets struggled for momentum.

Yet behind that headline number lies a story.

The defining engine of Pakistan's bull run has been a remarkably consistent inverse relationship between global oil prices and domestic equities. Pakistan imports most of its energy needs.

When crude costs rise, the economy imports inflation, burns

through foreign exchange reserves, widens its current account deficit, and

forces interest rates higher, a cocktail that strangles the

equity risk premium and sends investors to the sidelines. When crude falls, the

opposite occurs with striking speed.

That logic played

out with textbook precision between 2022 and 2025. As West Texas Intermediate

(WTI) crude retreated from its post-Ukraine peak, Pakistani equities were

unleashed, crossing 100,000 points in 2024 and reaching a peak of 189,166 on

January 22, 2026.

The bull run was

not simply sentiment, it was macroeconomically grounded in

a genuine improvement in Pakistan's external account, inflation trajectory, and

real interest rates.

Today, that

runway has been violently cut short.

The escalating military standoff between Iran and the United States has injected a massive risk premium into global energy markets. Fear of disruptions to Strait of Hormuz shipping lanes triggered an oil price shock that pushed WTI from $58.64 in December 2025 to a peak of $112.41 per barrel in early April 2026, a 91.7% surge in just four months.

The KSE-100,

which had set an all-time high only week earlier, crashed 22.6% in response

before staging a partial recovery to its current level of 170,509.

Following table

tracks WTI crude oil and the KSE-100 at annual intervals from December 2020

through the present day, with key 2026 events highlighted.

|

Date |

WTI

(USD/bbl) |

WTI

Change |

KSE-100

Level |

KSE-100

Change |

Note |

|

Dec 1, 2020 |

$45.28 |

— |

42,027 |

— |

|

|

Dec 1, 2021 |

$66.50 |

+46.9% |

43,234 |

+2.9% |

|

|

Dec 1, 2022 |

$79.98 |

+76.6%* |

42,150 |

+0.3%* |

|

|

Dec 3, 2023 |

$73.04 |

-8.7% vs '22 |

62,493 |

+48.3% vs '22 |

|

|

Dec 1, 2024 |

$68.10 |

-14.8% vs '22 |

103,275 |

+144.8% vs '22 |

|

|

Dec 1, 2025 |

$58.64 |

-26.7% vs '22 |

167,642 |

+297.5% vs '22 |

|

|

Jan 22, 2026 |

$59.36 |

-25.8% vs '22 |

189,166 |

+348.7% vs '20 |

ALL TIME HIGH |

|

Apr 5-6, 2026 |

$112.41 |

+91.7% vs Dec'25 |

~151,000 |

-20.2% from ATH |

Oil

Peak

in 2026 |

|

May

24, 2026 |

$91.53 |

+56.1% vs Dec'25 |

170,509 |

+1.7% vs Dec'25 |

|

*

WTI Change and KSE-100 Change in rows for Dec 2021 and Dec 2022 are measured

from Dec 1, 2020 baseline. Subsequent rows show change versus Dec 2022 (Phase 2

baseline) unless otherwise noted. Oil peak of $112.41 was reached on April 5-6,

2026.

Phase

Summary: Three Acts of a Decade-Defining Divergence

|

Phase |

Period |

WTI

Move |

KSE-100

Move |

|

Phase

1 |

Dec 2020 – Dec

2022 |

$45.28 →

$79.98 (+76.6%) |

42,027 →

42,150 (+0.3%) |

|

Phase

2 |

Dec 2022 – Dec

2025 |

$79.98 →

$58.64 (-26.7%) |

42,150 →

167,642 (+297.5%) |

|

Phase

3 |

Dec 2025 – May

2026 |

$58.64 →

$112.41 peak (+91.7%) |

167,642 →

170,509 (+1.7%) |

Phase

1 (Dec 2020 – Dec 2022):

The KSE-100 sat

at 42,027 in December 2020, and the subsequent two years would prove to be an

exercise in frustration for equity investors. As WTI crude climbed steadily

from $45.28 to $66.50 by December 2021, and then to $79.98 by December 2022, a cumulative rise of 76.6% the macroeconomic environment for Pakistan

deteriorated markedly.

Critically, this

table does not capture the full severity of the 2022 oil shock. In the wake of

Russia's invasion of Ukraine, WTI crude reached approximately $120 per barrel

in June 2022 before retreating. At those levels, Pakistan's monthly import bill

ballooned, its foreign exchange reserves fell to dangerously low levels, and

the Pakistan Rupee came under severe pressure.

Against this

backdrop, the KSE-100 effectively flatlined, ending December 2022 at 42,150, a gain of just 0.3% over two years. Capital

did not flee outright, but it refused to commit.

Phase

2 (Dec 2022 – Dec 2025):

The inflection

point came as global oil markets cooled and Pakistan's macroeconomic

stabilization program began to take hold. As WTI retreated from its 2022 highs falling to $73.04 by December 2023, then

$68.10 by December 2024, and finally $58.64 by December 2025 the pressure on Pakistan's external account

evaporated with remarkable speed.

This was not oil

alone. The International Monetary Fund's Extended Fund Facility provided a

critical policy anchor, restoring investor confidence in Pakistan's fiscal

trajectory.

The State Bank of

Pakistan began an aggressive rate-cutting cycle as inflation moderated from its

2023 peak. The Pakistani Rupee stabilized. With real interest rates turning

more favourable and external account pressures easing, capital rotated

aggressively into Pakistani equities.

The KSE-100's

trajectory in this period was extraordinary. From 42,150 in December 2022, the

index reached 62,493 by December 2023, a 48.3% gain driven largely by

normalizing macro conditions.

By December 2024,

it had crossed the historic 100,000-point barrier to reach 103,275, an

additional 65.3% gain.

And by December

2025, with WTI at its lowest point in years, the KSE-100 stood at 167,642, up

297.5% from its Phase 1 endpoint. It was one of the strongest multi-year equity

rallies recorded in any major emerging market.

Phase

3 (2026):

The KSE-100

entered 2026 with extraordinary momentum. In the first weeks of January, as WTI

remained subdued near $57–59 per barrel, the index surged to an all-time high

of 189,166 on January 22, 2026. At that level, the KSE-100 had gained 348.7%

from its December 2020 starting point. Investor sentiment was euphoric; the

consensus expected the index to cross 200,000 before mid-year.

The rupture came

swiftly and without warning. In the final days of February and first week of

March 2026, news of military hostilities between Iran and the United States

sent shockwaves through global energy markets.

In just five

trading sessions between February 26 and March 5, WTI crude surged from $67 to

$90.90 per barrel, a 35% spike that immediately recalibrated

Pakistan's entire macroeconomic outlook. By March 8, with WTI at $94.77, the

KSE-100 had crashed to 146,480, erasing 22.6% from its all-time high in under

six weeks.

The months that

followed were defined by extreme volatility tied directly to oil price

movements. When WTI briefly retreated to $82.59 on April 16, the KSE-100

bounced sharply to 173,939, briefly recovering above December 2025 levels.

When oil climbed

again toward $106-107 in late April and early May, the index tumbled back below

166,000. Each swing in crude produced an almost mirror-image move in Pakistan within

days compressing what had been an annual-timescale macro relationship

into a near-daily oscillation.

WTI crude reached

its peak of $112.41 on April 5-6, 2026, at which point the KSE-100 had fallen

to approximately 151,000, a 20.2% drop from its all-time high. As of May 24,

2026, with WTI settling at $91.53, the index has stabilized at 170,509 up a mere 1.7% since December 2025, versus

oil's 56.1% surge over the same period. The bull market has not broken, but it

is pinned.

The KSE-100's

near-term trajectory is now almost entirely a function of geopolitics rather

than domestic fundamentals. Two distinct scenarios define the path ahead.

In a

de-escalation scenario, a ceasefire or diplomatic

settlement between Iran and the United States, WTI could retreat meaningfully

toward the lower range, reopening the macroeconomic runway that drove the

2023-2025 bull run.

Under those

conditions, the KSE-100's all-time high of 189,166 would come quickly back into

view, and a move toward 200,000 would be realistic. Pakistan's improving fiscal

position, ongoing IMF support, and a benign interest rate environment would

once again dominate the investment narrative.

In an

entrenchment scenario where the conflict persists and oil sustains above $90

per barrel the calculus changes fundamentally. Pakistan's monthly petroleum

import bill would balloon, foreign exchange reserves would face renewed

pressure, and the State Bank of Pakistan would be constrained from continuing

its rate-cutting cycle.

The Monetary Policy Committee had

decided to increase the policy rate by 100 bps to 11.5% in its meeting held on

April 27, 2026, marking the first rate increase in nearly three years, since

the emergency hike to 22% in June 2023.

Inflation

expectations would be revised upward. Corporate earnings forecasts across the

cement, automobile, energy, and consumer sectors would be cut. In that

environment, investor risk appetite would erode and the KSE-100's hard-won

gains above 170,000 could come under sustained pressure.

As it stands, the market may be

getting the relief it desperately needed. Today, the benchmark KSE-100 opened

the week on a strong positive note, climbing 3,611.88 points to reach

171,456.12, after President Donald Trump revealed that the critical Strait of

Hormuz will be reopened as part of a sweeping Middle East peace agreement on

the verge of formation, following intensive Oval Office negotiations with

regional leaders, which caused West Texas Intermediate (WTI) crude futures to

fall by 5.66%, to $90.94.

Copyright Mettis

Link News

Related News

_20250922121949099_e67d18.webp?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,700.00 | 64,825.00 63,875.00 | 485.00 0.76% |

| BRENT CRUDE | 98.70 | 101.19 95.13 | -1.99 -1.98% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 121.10 121.10 | 0.70 0.58% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.47 | 0.00 0.00 | 1.16 1.30% |

| SUGAR #11 WORLD | 14.76 | 14.79 14.54 | 0.07 0.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|