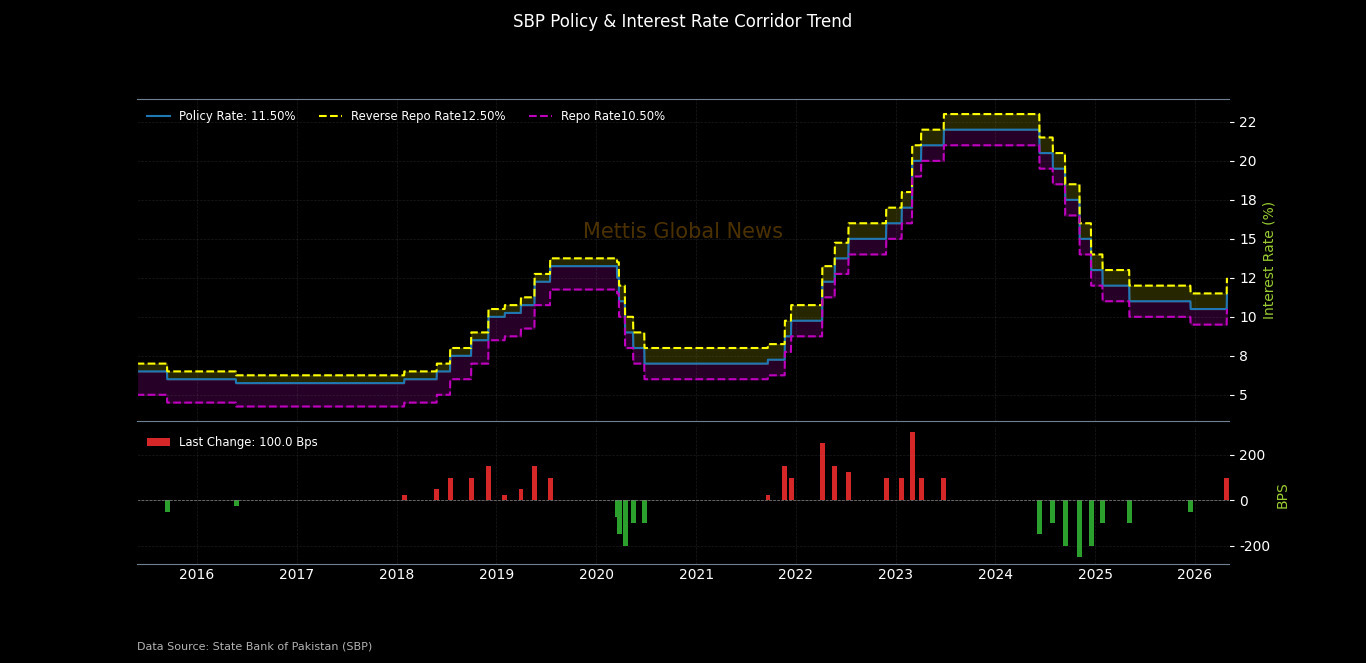

SBP hikes policy rate by 100bps to 11.5%

MG News | April 27, 2026 at 03:45 PM GMT+05:00

April 27, 2026 (MLN): The Monetary Policy Committee has decided to increase the policy rate by 100 bps to 11.5% in its meeting held on April 27, 2026.

The decision was primarily driven by mounting inflationary pressures and a significant rise in petrol prices, both of which have contributed to an deteriorating inflation outlook that warranted a firm monetary policy response.

This marks a notable shift from the Committee's previous stance. In its last meeting held on March 9, 2026, the MPC had kept the policy rate unchanged at 10.5%, opting at the time to monitor economic developments before taking further action. However, the subsequent surge in inflation and fuel prices prompted the Committee to adopt a more aggressive tightening posture at this latest sitting.

The 100 bps hike reflects the MPC's commitment to anchoring inflation expectations and restoring price stability in the economy, marking the first rate increase in nearly three years, since the emergency hike to 22% in June 2023.

The move also aligns with the IMF's latest assessment, which signaled support for the SBP's current stance and stressed that monetary policy must remain appropriately tight and responsive to data, warning that renewed spikes in global food and energy prices particularly amid ongoing geopolitical tensions could fuel price pressures and unanchor inflation expectations.

The Committee cited the prolonged Middle East conflict as

having materially intensified risks to Pakistan's macroeconomic outlook, with

global energy prices, freight charges, and insurance premiums continuing to

hold significantly above pre-conflict levels.

While incoming data has broadly aligned with earlier

projections, the MPC assessed that inflation is likely to rise and remain above

the target range for several quarters ahead, making a tighter policy stance

necessary to anchor expectations and contain second-round effects of the

ongoing supply shock.

Geopolitical Overhang Drives Rate Decision

The MPC noted that supply chain disruptions stemming from

the Middle East conflict have compounded prevailing uncertainty, with their

impact on key economic indicators expected to become increasingly visible in

the months ahead.

The Committee drew comfort from the fact that Pakistan's

macroeconomic fundamentals including

external buffers and fiscal discipline are considerably stronger at the onset of this

shock than during comparable episodes in the recent past, most notably the

Russia-Ukraine war of 2022.

The MPC also highlighted the successful staff-level

agreement reached with the IMF on March 27, 2026, alongside Pakistan's re-entry

into international capital markets after a gap of over four years through a

Eurobond issuance, as evidence of improved macroeconomic credibility.

The Committee reiterated that sustaining structural reforms

to enhance external account resilience remains critical to navigating the

evolving global landscape.

Inflation Rising, Double-Digit Risk Materialising

Headline inflation climbed to 7.3% in March 2026, while core

inflation edged up to 7.8%.

The MPC noted that even before the onset of the Middle East

conflict, inflation was projected to approach the upper bound of the 5–7%

target range, driven by adverse base effects.

The energy price shock has since added further upward

pressure, with higher fuel costs already feeding into core inflation through

transport fares. The Committee assessed that headline inflation could breach

double digits in the coming months, before gradually easing thereafter.

Nonetheless, inflation is expected to remain above the upper bound of the

target range for most of FY27.

Contained food inflation, supported by ample supplies, is

expected to provide only partial relief. The MPC flagged the duration and

intensity of the conflict, the extent of energy price pass-through to the

domestic economy, and potential fiscal slippages as key risks to the inflation

outlook.

Economic Activity Moderating After Strong First Half

Real GDP grew by 3.9% in Q2-FY26, bringing cumulative growth

in the first half of FY26 to 3.8% more

than double the 1.9% recorded in the same period last year. Large-scale

manufacturing posted robust growth of 5.9% during July–February FY26, and

high-frequency indicators across industrial and services sectors showed strong

momentum through February.

However, early signs of moderation emerged in March. In

agriculture, growth prospects have been tempered by lower-than-anticipated

wheat production as per first estimates from the Federal Committee on

Agriculture.

The spillover of the ongoing conflict on industrial and

services activity in Q4 is expected to bring full-year GDP growth for FY26

closer to the lower bound of the earlier projected range.

The moderation in economic activity is expected to extend

into FY27, with the outlook remaining subject to multiple risks tied to the

conflict's trajectory.

External Sector Resilient, Reserves Holding

Consecutive current account surpluses in February and March

resulted in a small cumulative surplus during July–March FY26, supported

primarily by resilient workers' remittances.

The current account for FY26 is now expected to remain

closer to the lower bound of the earlier projected range, despite a significant

worsening in terms-of-trade.

On the financing

side, the government proactively secured external funding through enhanced

bilateral arrangements and the Eurobond issuance, which cushioned the impact of

recent debt and liability repayments on SBP's foreign exchange reserves.

As of April 24, 2026, SBP's FX reserves stood at

approximately $15.8 billion, with the reserve target now revised upward to

above $18 billion by June 2026. The Committee emphasised the continued need to

strengthen foreign exchange buffers amid uncertain global economic conditions.

Fiscal Pressures Mount, Tax Shortfall Widens

FBR tax collection fell short of target in March, pushing

the cumulative shortfall to Rs611 billion during July–March FY26.

Despite this, financing-side data suggests the fiscal

deficit remained contained through March.

However, the Middle East conflict has complicated fiscal

management, as the pass-through of higher international oil prices to domestic

consumers has necessitated targeted subsidies for vulnerable groups.

The MPC noted that achieving the full-year primary surplus

target may require a larger reduction in expenditures.

The Committee stressed the importance of sustained fiscal

reforms, including broadening the tax base and curtailing state-owned

enterprise losses, to reinforce long-term fiscal sustainability and resilience.

Money and Credit

Broad money growth decelerated to 14.5% as of April 10, down

from 16.0% recorded on February 20, driven primarily by a slowdown in net

budgetary borrowing from the banking system.

Private sector credit continued to expand at around 13%, in

line with improving economic activity and the lagged impact of earlier policy

rate reductions.

During July–March FY26, credit flows grew across working

capital, fixed investment, and consumer finance. Sectoral concentration

remained in textiles, wholesale and retail trade, and chemicals, while a

sustained rise in consumer financing pointed to a gradual recovery in household

demand.

On the liability side, both currency in circulation and

deposits recorded some deceleration since the last MPC meeting.

The Committee reaffirmed that a positive real policy rate,

combined with prudent fiscal management, remains essential to preserving

macroeconomic stability and supporting sustainable long-term growth.

Copyright Mettis

Link News

Related News

_20260126115701440_af4631.webp?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,776.60 345.77M | 0.98% 1761.66 |

| ALLSHR | 109,308.50 789.13M | 0.86% 936.37 |

| KSE30 | 54,391.82 176.06M | 1.06% 570.01 |

| KMI30 | 256,134.77 127.57M | 1.02% 2587.38 |

| KMIALLSHR | 70,024.34 435.42M | 0.77% 532.38 |

| BKTi | 52,367.72 86.35M | 1.01% 524.10 |

| OGTi | 35,302.82 9.03M | 1.44% 500.16 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,550.00 | 64,590.00 64,490.00 | -70.00 -0.11% |

| BRENT CRUDE | 83.08 | 83.77 78.92 | 3.63 4.57% |

| RICHARDS BAY COAL MONTHLY | 107.75 | 0.00 0.00 | 2.20 2.08% |

| ROTTERDAM COAL MONTHLY | 116.25 | 116.50 116.25 | 0.20 0.17% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 78.11 | 78.21 77.80 | 0.82 1.06% |

| SUGAR #11 WORLD | 15.58 | 15.60 14.98 | 0.43 2.84% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|