PIBTL target price set at Rs23 amid earnings turnaround

MG News | June 24, 2026 at 03:22 PM GMT+05:00

June 24, 2026 (MLN): Pakistan International Bulk Terminal Limited (PIBTL) has received a 'Buy' rating from JS Global Capital with a June 2027 DCF-based target price of Rs23 per share, implying 30% upside from the current market price of Rs17.70, as the brokerage initiates coverage on the Port Qasim-based bulk terminal operator.

The investment case rests on three pillars: high operating

leverage tied to throughput recovery, an ongoing balance sheet deleveraging

cycle, and long-term volume visibility anchored by both cyclical coal demand

and structural upside from mining-related cargo flows.

PIBTL operates Pakistan's first mechanised bulk terminal at

Port Qasim under a 30-year Build-Operate-Transfer concession agreement signed

with Port Qasim Authority in November 2010.

The terminal, developed with an investment exceeding $300m

including financing support from the International Finance Corporation, has an

annual handling capacity of 12m tons for imported coal and 4m tons for clinker

and cement exports.

The company is a flagship project of the Marine Group of

Companies.

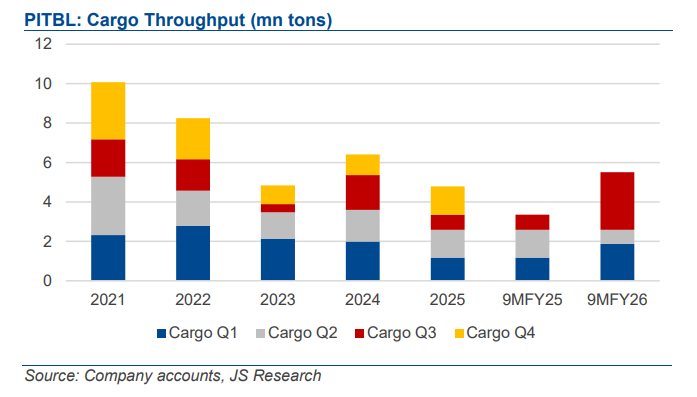

The company delivered a strong earnings turnaround in

9MFY26, posting a net profit of Rs2.1bn compared to a marginal loss in the

corresponding period last year.

The recovery was driven by a 57% year-on-year increase in

cargo volumes to 5.5m tons, showing stronger demand for imported coal across

key industrial sectors. Revenue rose 57% YoY to Rs11.7bn, while gross profit

more than doubled to Rs3.9bn, emphasizing significant operating leverage from

improved throughput and better capacity utilization.

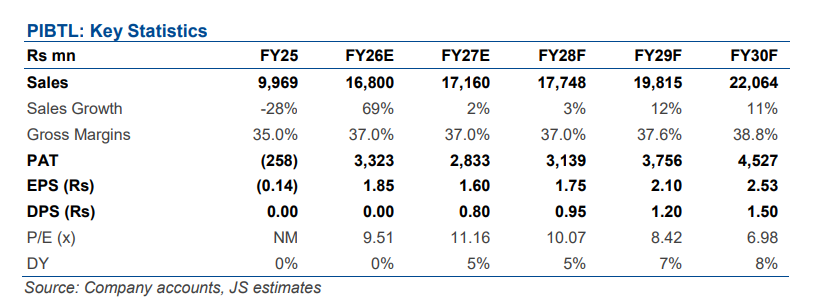

JS Global projects full-year FY26 net profit at Rs3.3bn,

recovering from a net loss of Rs258m in FY25, with revenue estimated to surge

69% to Rs16.8bn.

Earnings are forecast to scale further over FY27–FY31E, with

net profit reaching Rs4.5bn by FY30F as volumes normalise and the balance sheet

continues to deleverage.

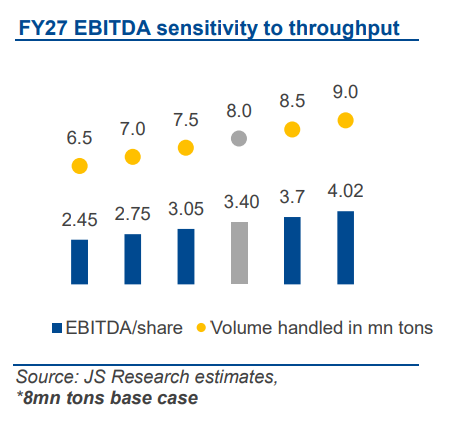

JS Global's sensitivity analysis highlights a near-linear

relationship between throughput volumes and earnings. EBITDA per share is

estimated to rise from Rs2.45 at 6.5m tons to Rs4.02 at 9m tons, implying

approximately Rs0.31 of EBITDA accretion per additional million ton of cargo

handled.

The brokerage's base case assumes 8 million tons of

throughput for FY27, with volumes projected to normalise to the 8–9m ton range

through FY28E.

Coal throughput at PIBTL has benefited from disruptions in

Afghan coal trade flows, with border closures and security-related frictions

reducing the competitiveness of Afghan-origin coal.

This has pushed cement manufacturers in the North to

increasingly rely on imported coal routed through PIBTL.

JS Global conservatively assumes a 23% decline in coal

volumes for cement applications once Afghan supply routes gradually reopen,

though it does not anticipate the border reopening in the near term, with any

meaningful resumption expected to take at least nine months.

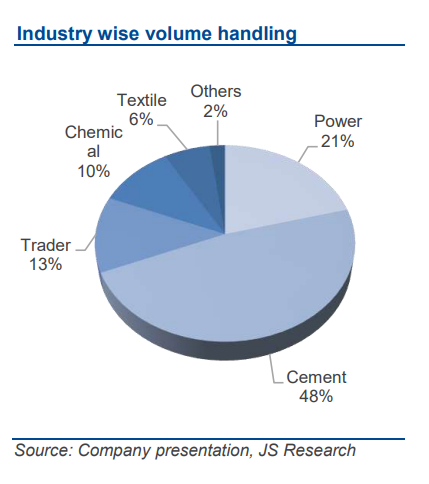

In FY25, PIBTL handled 4.8m tons of cargo, with the cement

sector accounting for the largest share at 2.3m tons or 48% of total volumes.

The power sector contributed 1.0m ton, followed by traders

at 0.6 million tons, chemicals at 0.5m tons, and textiles at 0.3m tons.

Beyond cyclical recovery, JS Global identifies Reko Diq as

the key long-term volume catalyst. PIBTL has secured a supplemental

implementation agreement with Port Qasim Authority granting it rights to

handle, store, and export copper-gold concentrates and other mineral

commodities on a non-exclusive basis.

Reko Diq Mining Company has designated PIBTL as its

preferred export terminal, with Phase 1 export volumes expected at up to

800,000 tons and Phase 2 at up to 1.8m tons annually, with project commencement

expected in FY29.

JS Global's base case assumes 1m tons of incremental

mining-related volume in FY29, rising to 2m tons annually thereafter,

contributing to an estimated 10% volume growth in cargo handled over the next

five years.

The brokerage also notes PIBTL's recently secured

copper-gold export concession and Port Access Agreement with Reko Diq as

additional catalysts supporting earnings visibility.

PIBTL is approaching a significant balance sheet inflection

point. Foreign debt is expected to be fully retired by June 2026, with

remaining local borrowings projected to be extinguished over the subsequent one

to two years.

The company's debt-to-asset ratio is estimated to decline

sharply from 42% in FY23 to 12% in FY26E and further to near-zero by FY28F.

This transition is expected to materially reduce finance

costs, eliminate foreign exchange-related volatility from reported earnings,

and strengthen free cash flow generation.

As the balance sheet normalises, JS Global anticipates

reinstatement of dividend payouts from FY27F onward, with a DPS of Rs0.80

projected for FY27 and Rs0.95 for FY28F.

Applying a 100% payout ratio consistent with the practice of

close peer Pakistan International Container Terminal (PICT) implies a FY27E

dividend yield of approximately 8.5%.

JS Global's model conservatively assumes a flat

USD-denominated tariff throughout the forecast horizon with no upward revision

for inflation, improved cargo mix, or enhanced bargaining power from

higher-value mining cargo.

Approximately 35% of revenue is payable to Port Qasim

Authority as royalty under the BOT agreement.

It noted that any future tariff revision would provide

direct upside: a 1% increase in the average tariff lifts the target price to

Rs27.24 from the base case of Rs23.

On the currency side, PIBTL's USD-linked revenue model

provides a natural hedge against PKR depreciation, with a 5% depreciation in

the PKR/USD rate estimated to lift EPS by around 11%.

At 9.5x FY26E price-to-earnings, PIBTL trades at an

approximately 50% discount to the regional peer average of 18.9x.

The DCF-based valuation employs a 12% risk-free rate, 6%

equity risk premium, and an equity beta of 1.0, resulting in an 18% cost of

equity. JS Global values the company on free cash flows through FY45E, covering

the remaining life of the BOT concession.

JS Global flags macro and geopolitical risks that could

weigh on industrial activity and cargo demand, slower-than-expected throughput

recovery, delays in Reko Diq-linked cargo materialisation due to security

concerns, and the inability to revise terminal tariffs all of which could limit

earnings upside relative to estimates.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,355.00 | 64,470.00 63,875.00 | 140.00 0.22% |

| BRENT CRUDE | 98.70 | 101.19 95.13 | -1.99 -1.98% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 121.10 121.10 | 0.70 0.58% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.47 | 92.83 87.68 | -1.72 -1.87% |

| SUGAR #11 WORLD | 14.76 | 14.79 14.54 | 0.07 0.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|