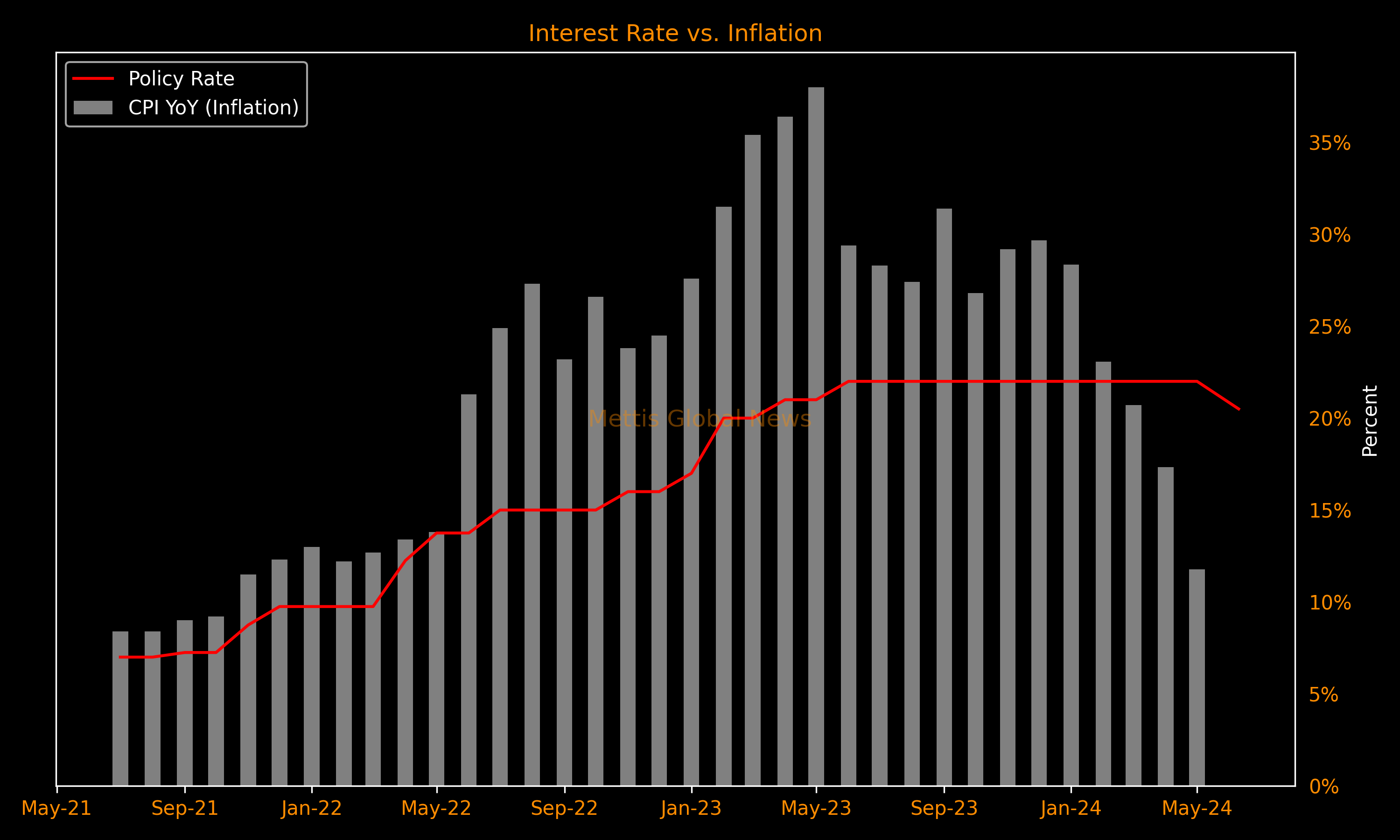

SBP cuts policy rate by 150bps to 20.5%

MG News | June 10, 2024 at 04:19 PM GMT+05:00

June 10, 2024 (MLN): The State Bank of Pakistan (SBP) lowered its key policy rate by 150 basis points to 20.5% on Monday, a bigger margin than expected by market analysts.

The reduction is the first in almost four years and comes ahead of the country’s annual budget 2024-25.

The central bank had kept borrowing costs at a record 22% since June 2023.

The Monetary Policy Committee in a press statement noted that while the significant decline in inflation since February was broadly in line with expectations, the May outturn was better than anticipated earlier.

The Committee assessed that underlying inflationary pressures are also subsiding amidst tight monetary policy stance, supported by fiscal consolidation.

This is reflected by continued moderation in core inflation and ease in inflation expectations of both consumers and businesses in the latest surveys.

At the same time, the MPC viewed some upside risks to the near-term inflation outlook associated with the upcoming budgetary measures and uncertainty regarding future energy price adjustments.

Notwithstanding these risks and today’s decision, the Committee noted that the cumulative impact of the earlier monetary tightening is expected to keep inflationary pressures in check

The MPC noted the following key developments since its last meeting.

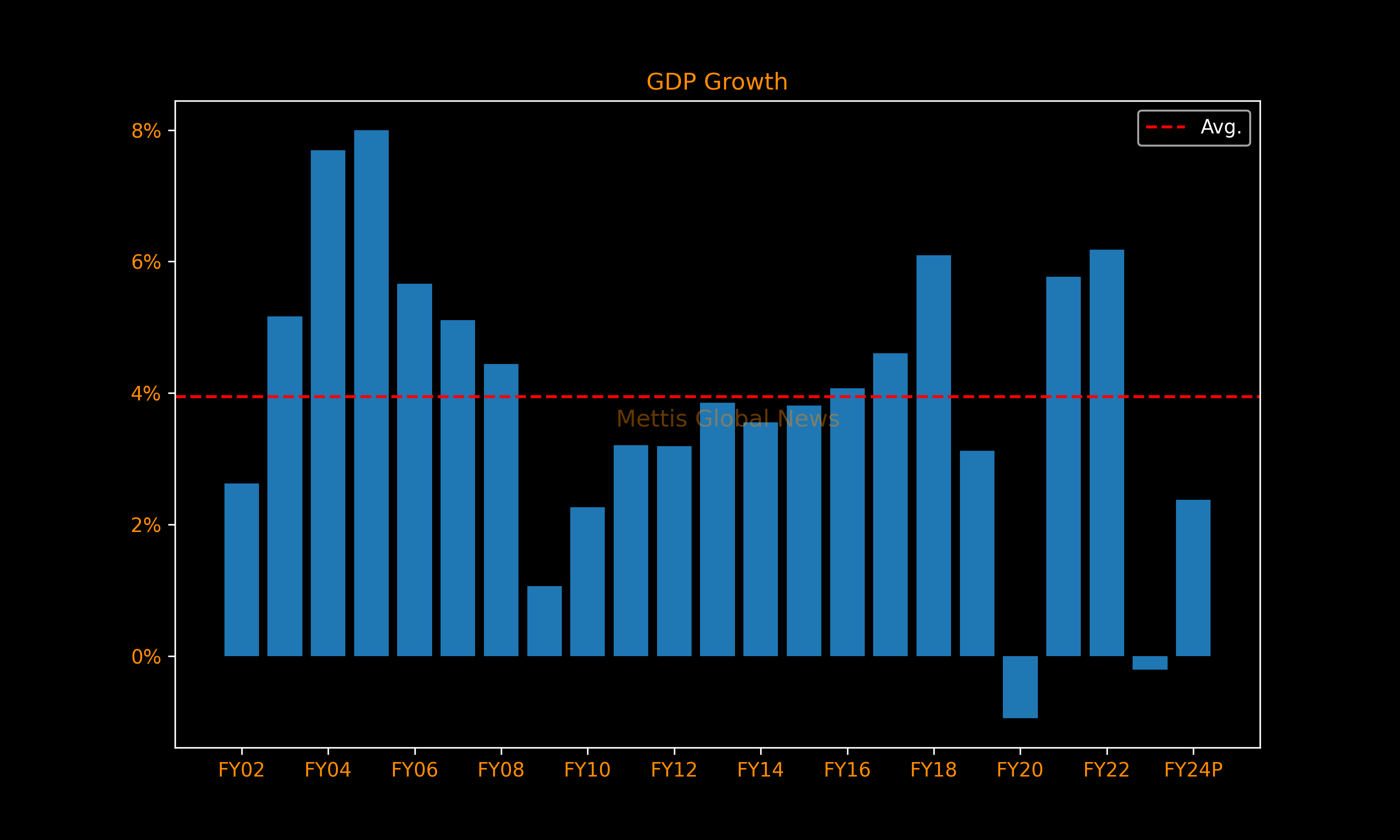

First, real GDP growth remained moderate at 2.4% in FY24 as per provisional data, with subdued recovery in industry and services partially offsetting the strong growth in agriculture.

Second, reduction in the current account deficit has helped improve the FX reserves to around $9 billion despite large debt repayments and weak official inflows.

The government has also approached the IMF for an Extended Fund Facility program, which is likely to unlock financial inflows that will help in further build-up of FX buffers.

Lastly, international oil prices have declined, whereas non-oil commodity prices have continued to inch up.

Based on these developments, the Committee, on balance, viewed that it is now an appropriate time to reduce the policy rate.

The Committee noted that the real interest rate still remains significantly positive, which is important to continue guiding inflation to the medium-term target of 5 – 7%.

Real Sector

The Committee also emphasized that the future monetary policy decisions will remain data-driven and responsive to evolving developments related to the inflation outlook.

Latest estimates indicate real GDP growth at 2.1% in Q3-FY24 against a contraction of 1.1% in the same quarter last year.

While agriculture was already showing strong growth, industry also witnessed positive growth in Q3. Also, initial growth estimates for both Q1 and Q2 for FY24 were revised upward.

Taking into account the developments in the first nine months, FY24 growth is provisionally estimated by PBS at 2.4% against a contraction of 0.2% in FY23.

Almost two-thirds of this recovery was explained by improvement in the agriculture sector.

These developments are in line with the MPC’s earlier expectations. For FY25, the MPC expects economic growth to remain moderate.

This assessment takes into account the impact of expected moderation in agriculture output and ongoing stabilization policies.

External Sector

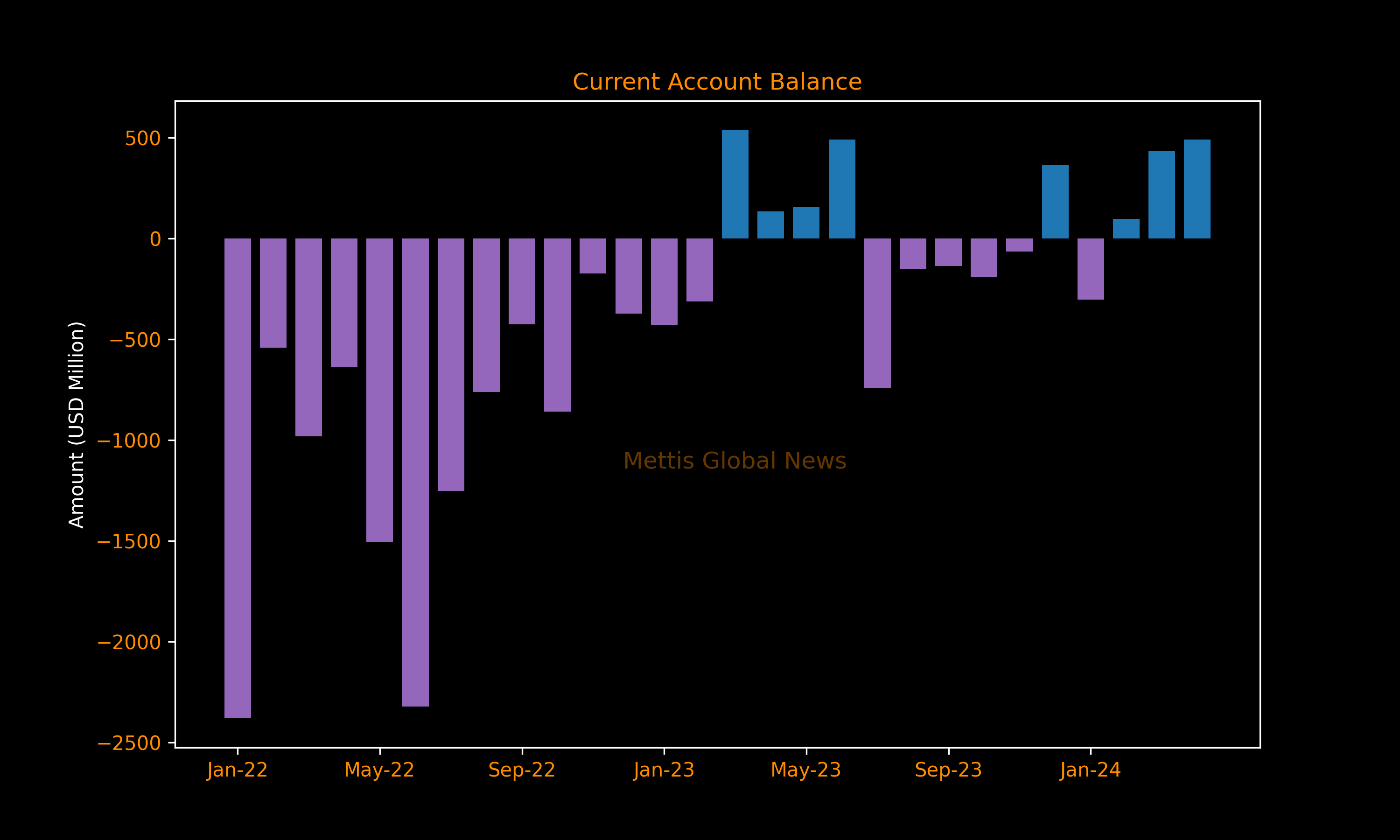

The current account posted a surplus for the third consecutive month in April on the back of robust growth in remittances and exports, which more than offset the uptick in imports.

During July-April FY24, the current account deficit narrowed significantly to $202 million. In the same period, exports grew by 10.6%, mainly driven by increased quantum of rice and HVA textile exports.

Conversely, imports decreased by 5.3% during the same period due to lower international commodity prices, better domestic agriculture output and moderate economic activity.

Workers’ remittances also remained robust in recent months, reaching an all-time high of $3.2bn in May 2024.

The resultant lower current account deficit, along with improved FDI and the disbursement of SBA tranche in April, has facilitated ongoing large debt repayments and supported the SBP's FX reserves.

Going forward, the Committee stressed that timely mobilization of financial inflows is essential to meet the external financing requirements and further strengthen FX buffers for the country to effectively respond to any external shocks and support sustainable economic growth.

Fiscal sector

Fiscal indictors continued to show improvement during July-March FY24.

The primary surplus increased to 1.5% of GDP, while the overall deficit remained almost at last year’s level.

A large part of this improvement reflected the impact of increase in tax and PDL rates, higher SBP profit, and lower energy sector subsidies.

Considering there has been limited progress in addressing the structural weaknesses to broaden the tax base and initiate energy sector reforms, FY25 budgetary measures are also expected to be largely rate-based.

In this backdrop, the Committee emphasized that fiscal consolidation through broadening the tax base and reforming loss-making public sector enterprises would help achieve fiscal sustainability on a more durable basis.

This is also imperative to keep inflation on a downward trajectory and contain external account pressures.

Money and credit

The broad money (M2) growth decelerated to 15.2% YoY on May 24, 2024 from 17.1% as of end-March 2024.

This reduction was primarily due to deceleration in growth of net domestic assets of the banking system.

On the other hand, the growth contribution of net foreign assets in M2 remained positive.

From the liability side, deposits remained the mainstay in M2 growth, while currency in circulation growth decelerated.

As a result, reserve money growth observed a steep decline from 10.0% to 4.3% during the period.

The MPC noted that these developments in monetary aggregates are consistent with the tight monetary policy stance and have favorable implications for the inflation outlook.

Inflation outlook

Headline inflation decelerated to 11.8% in May 2024 from 17.3% in April.

Besides the continued tight monetary policy stance, this sharp reduction was also driven by a sizeable decline in prices of wheat, wheat flour, and some other major food items, along with the downward adjustment in administered energy prices.

Core inflation also decelerated to 14.2% from 15.6%.

The Committee noted that the near-term inflation outlook is susceptible to risks emanating from the FY25 budgetary measures and future adjustments in electricity and gas tariffs.

The MPC foresees a risk of inflation to rise significantly in July 2024 from current levels, before trending down gradually during FY25.

The MPC also observed that sharp wheat price reductions have historically proved to be temporary.

On balance, the Committee assessed that the current monetary policy stance remains appropriate to ensure that inflation stays on a downward trajectory.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 178,922.76 458.03M | -1.36% -2475.46 |

| ALLSHR | 107,850.27 1,038.22M | -1.24% -1356.82 |

| KSE30 | 53,308.95 263.66M | -1.46% -789.54 |

| KMI30 | 255,193.17 241.09M | -1.46% -3789.62 |

| KMIALLSHR | 69,955.81 579.69M | -1.31% -930.18 |

| BKTi | 48,839.93 52.13M | -1.20% -593.67 |

| OGTi | 36,450.04 22.36M | -1.87% -693.83 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,535.00 | 64,825.00 62,315.00 | 1590.00 2.53% |

| BRENT CRUDE | 79.31 | 82.30 79.24 | -1.26 -1.56% |

| RICHARDS BAY COAL MONTHLY | 115.00 | 0.00 0.00 | 0.00 0.00% |

| ROTTERDAM COAL MONTHLY | 125.50 | 0.00 0.00 | -0.65 -0.52% |

| USD RBD PALM OLEIN | 1,157.50 | 1,157.50 1,157.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 75.57 | 78.14 74.98 | -0.28 -0.37% |

| SUGAR #11 WORLD | 14.14 | 0.00 0.00 | 0.01 0.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|