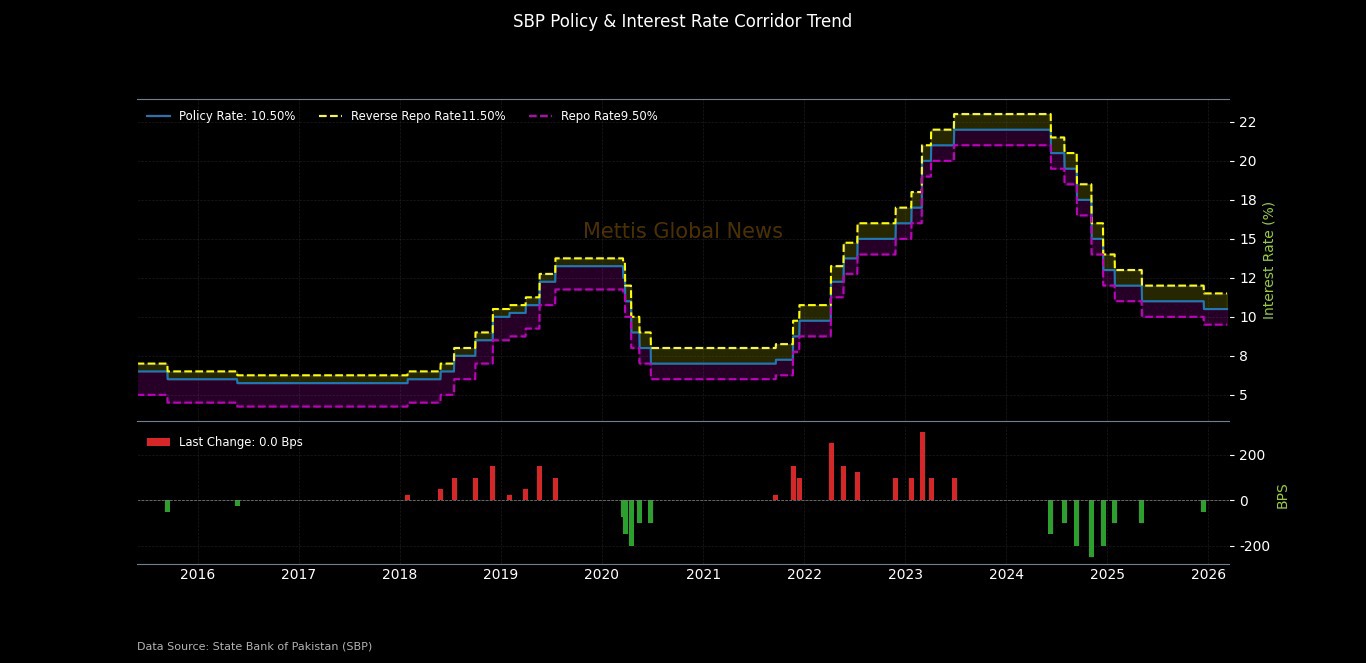

SBP keeps policy rate unchanged at 10.5%

_20260126121902577_b63c19.webp?width=950&height=450&format=Webp)

MG News | March 09, 2026 at 02:58 PM GMT+05:00

March 09, 2026 (MLN): The Monetary Policy Committee

has decided to keep the policy rate unchanged at 10.5% in its meeting

held on March 9, 2026.

Geopolitical Shock Dominates MPC Deliberations

The MPC noted that the Middle East conflict has triggered a sharp rise in global fuel prices, freight and insurance costs, and has disrupted cross-border trade and travel flows. The Committee acknowledged that both the intensity and duration of the conflict will be critical determinants of the eventual impact on Pakistan's economy.

In a measured assessment, the MPC drew comparisons to the Russia-Ukraine war of 2022, noting that Pakistan's macroeconomic fundamentals particularly on inflation, foreign exchange reserves, and fiscal buffers are considerably stronger today.

The Committee's initial assessment suggests that key macroeconomic variables for FY26 remain within earlier projected ranges, though risks have increased significantly.

Inflation Picks Up, Pressures Remain Manageable

Headline inflation rose to 5.8% in January 2026 and climbed further to 7% year-on-year in February, largely driven by the phasing out of favorable base effects in food and energy prices, alongside a rationalization of fixed charges on household electricity bills. Core inflation also edged higher to around 7.6%.

Despite the uptick, the MPC assessed that improved supply conditions for key food items and better agricultural prospects may partially offset pressures from higher domestic energy prices.

The Committee also noted that anchored inflation expectations should limit second-round effects. However, the MPC cautioned that inflation is likely to remain above 7% through the remaining months of FY26 and into FY27, with significant risks attached to the geopolitical situation and potential adjustments in administered energy prices.

Economic Activity Sustains Momentum

Economic activity continued to strengthen heading into 2026. High-frequency indicators including auto sales, cement dispatches, electricity generation, and POL sales (excluding furnace oil) all recorded higher growth during July–January FY26.

Large-scale manufacturing grew 0.4% year-on-year in December 2025, with cumulative LSM growth reaching 4.8% during July–December FY26. Recent policy measures, including the reduction in the Cash Reserve Requirement, lower markup rates on export loans, and downward adjustments in industrial energy tariffs, have further supported manufacturing prospects.

In agriculture, wheat sowing targets have largely been met and input conditions remain favorable, with positive spillover effects expected for wholesale, retail trade, and transport services.

Against this backdrop, the MPC maintained its GDP growth projection for FY26 at 3.75–4.75%, though the outlook is subject to downside risks from unfolding geopolitical developments.

External Sector Holds Steady

The current account posted a surplus of $121m in January 2026, containing the cumulative deficit to $1.1bn in July–January FY26. Imports declined in January while exports and workers' remittances stabilized at December levels.

Continued SBP interbank purchases helped lift foreign exchange reserves to $16.3bn as of February 27.

Looking ahead, the current account deficit is expected to remain within the 0–1% of GDP range for FY26. The MPC stressed the importance of timely realization of planned official inflows to achieve the $18bn reserve target by June 2026, while flagging global trade fragmentation and geopolitical uncertainty as key risks.

Fiscal and Monetary Conditions

On the fiscal side, the overall balance remained in surplus and the primary surplus held close to last year's levels, driven by contained expenditures and lower interest payments. However, FBR tax collection rose only 10.6% during July–February FY26 well below the pace needed to meet the annual target further widening the cumulative shortfall.

Broad money (M2) growth eased to 16% as of February 20, as net budgetary borrowing from the banking system fell sharply.

Private sector credit expanded by Rs790bn through February 20, with growth particularly notable in textiles, wholesale and retail trade, chemicals, and consumer financing.

The MPC reaffirmed the importance of fiscal consolidation through tax base-broadening measures and structural reforms, and emphasized that a positive real policy rate combined with prudent fiscal policy remains essential to sustaining macroeconomic stability and long-term growth.

Copyright Mettis Link News

Related News

_20260101112329999_0153db_20260209062258909_9180ec.webp?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,776.60 345.77M | 0.98% 1761.66 |

| ALLSHR | 109,308.50 789.13M | 0.86% 936.37 |

| KSE30 | 54,391.82 176.06M | 1.06% 570.01 |

| KMI30 | 256,134.77 127.57M | 1.02% 2587.38 |

| KMIALLSHR | 70,024.34 435.42M | 0.77% 532.38 |

| BKTi | 52,367.72 86.35M | 1.01% 524.10 |

| OGTi | 35,302.82 9.03M | 1.44% 500.16 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,430.00 | 64,590.00 64,415.00 | -190.00 -0.29% |

| BRENT CRUDE | 83.08 | 83.77 78.92 | 3.63 4.57% |

| RICHARDS BAY COAL MONTHLY | 107.75 | 0.00 0.00 | 2.20 2.08% |

| ROTTERDAM COAL MONTHLY | 116.25 | 116.50 116.25 | 0.20 0.17% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 78.08 | 78.21 77.80 | 0.79 1.02% |

| SUGAR #11 WORLD | 15.58 | 15.60 14.98 | 0.43 2.84% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|