Positive shift expected for Pakistan’s credit rating: Goldman Sachs

MG News | March 07, 2024 at 10:11 AM GMT+05:00

March 07, 2024 (MLN): There is potential for an improvement in Pakistan's credit rating alongside its USD bonds, with expectations for the yield curve to steepen, according to a report by Goldman Sachs.

The report also sees potential gains for Pakistan's currency, which offers both value and carry.

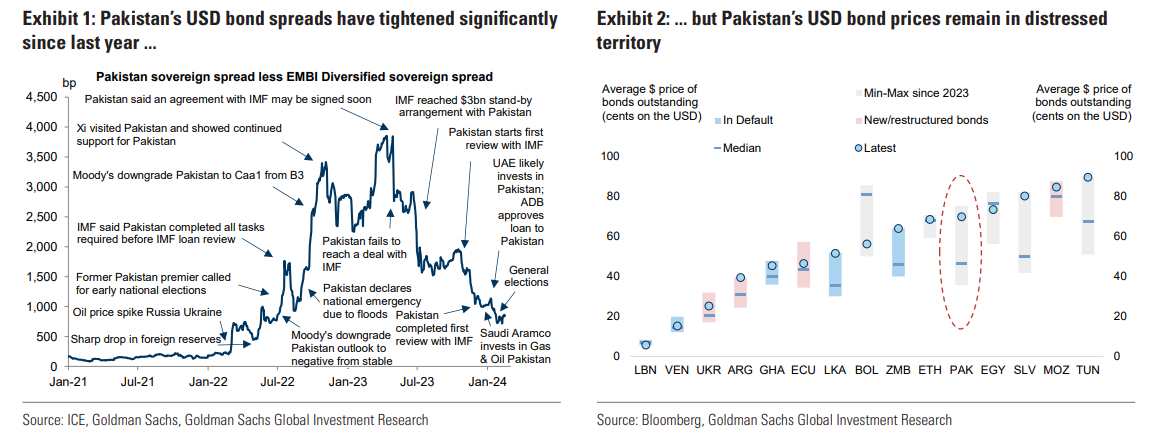

After being at distressed levels since 2022, Pakistan’s USD bonds delivered some of the highest returns in the EMBI Global Diversified index last year.

This was driven by a combination of an improving global macro backdrop, with lower inflation and the end of the Fed’s hiking cycle, and renewed lending by the IMF.

That said, although Pakistan’s USD bond spreads are now tighter than similarly rated peers, last year’s outsized returns have not been enough to bring its USD bonds out of distress, and for the country to regain market access.

Pakistan’s near-term external vulnerabilities appear to be manageable.

Looking at its near-term external vulnerabilities, the report highlighted that Pakistan’s gross FX reserves exceed the 2024 liabilities stemming from the current account and short-term external debt, and Pakistan screens as better value than other EM credits, such as Kenya and Egypt, where USD bond prices are higher.

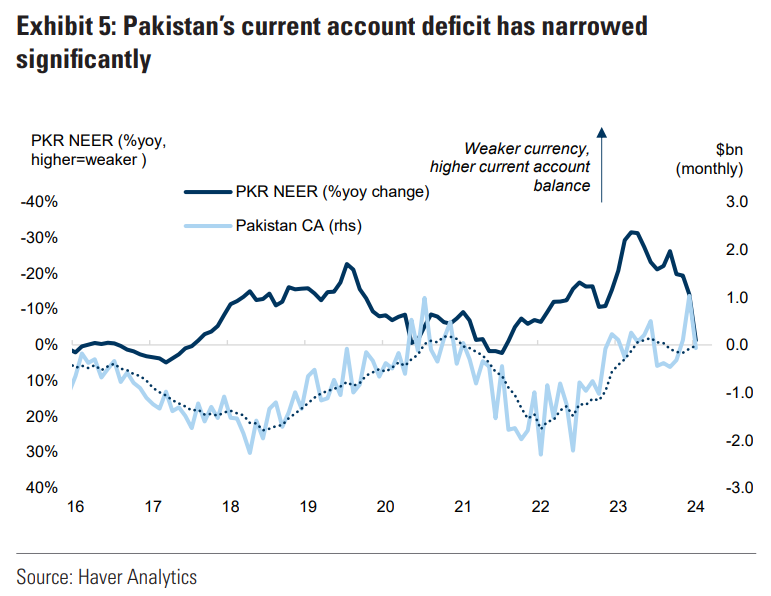

The gross FX reserve decline that began in 2022 has stalled, and reversed slightly in 2023, largely reflecting improved balance of payment dynamics.

In particular, Pakistan’s current account moved from a deficit to balance after a significant weakening of the PKR led to a contraction in goods imports.

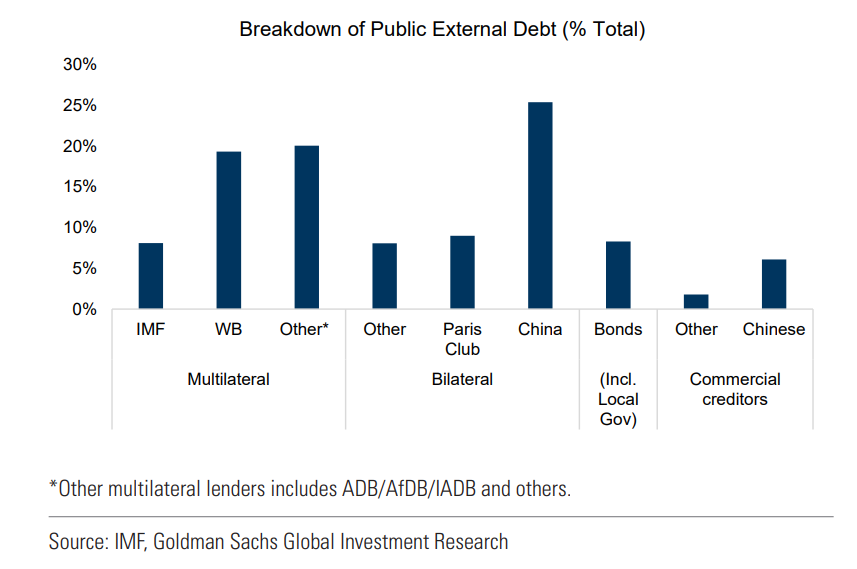

While flow dynamics have improved, total external debt remains high at $130 billion (~50% of GDP), and most of this is public sector debt.

However, looking at the breakdown of this debt, the report noted that ~85% of it is owed to multilateral and bilateral lenders, with China the single-largest creditor.

Conversely, private and commercial debt is relatively small, and the upcoming liability profile on Pakistan’s international USD bonds alone appears manageable.

Goldman Sachs viewed the heavy tilt towards bilateral and multilateral lending as important in assessing Pakistan’s external funding pressures, as it is often easier to renegotiate lending terms with a single creditor than a group of creditors (as is the case with bond holders), and the incentive structures for lending are different.

For example, multilateral creditors such as the IMF largely work to avert balance of payments crises, and bilateral ending can be highly political.

To note, Pakistan currently has a modal rating of ~CCC by the three rating agencies, Moody’s, Fitch and S&P.

Commentary by the three agencies on Pakistan’s rating has indicated that Pakistan’s rating will be upgraded if the country’s fiscal and external positions improve, as the above analysis suggests that it has and should continue to do.

Goldman's EM Sovereign Ratings Model suggests that Pakistan’s CCC rating is roughly in line with Pakistan’s fundamentals of 2023, which saw negative growth rates, high inflation, and high external vulnerabilities.

However, using the IMF’s forecast for 2025, which sees a normalisation in Pakistan’s real growth rate and inflation back towards the central bank’s target range, alongside a decline in public debt levels, the model suggests that this should be consistent with rating upgrades back towards the single B-rated bucket.

Goldman Sachs also flagged several risks. First, Pakistan’s IMF program is due to expire in April, and the sustainability of its external balances depends on a renewal of this program.

The renewal of this program is likely, but it will ultimately depend on the newly elected government.

Second, while fiscal risks look manageable in the near to medium term, the revenue base of the country remains limited, undermining the potential to fund the spending required on many services, suggesting that current and past spending patterns may not be sustainable in the long run.

The report noted the most significant risk to be the lack of sustainable growth, especially export growth.

In the last two decades, the country has essentially relied on exporting human capital and funding domestic demand through remittances, a pattern that is unlikely to be sustainable in the long run.

Copyright Mettis Link News

Related News

.png?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,495.00 | 64,550.00 63,875.00 | 280.00 0.44% |

| BRENT CRUDE | 98.70 | 101.19 95.13 | -1.99 -1.98% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 121.10 121.10 | 0.70 0.58% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.47 | 92.83 87.68 | -1.72 -1.87% |

| SUGAR #11 WORLD | 14.76 | 14.79 14.54 | 0.07 0.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|