MARI to hit Rs3,000/share by end of CY24

MG News | December 22, 2023 at 02:13 PM GMT+05:00

December 22, 2023 (MLN): Mari Petroleum Company Limited (PSX: MARI) is poised for substantial growth, with its share price expected to reach Rs3,000 by the end of December 2024, offering a notable upside of 44% from current levels, as per a report by JS Global Capital Limited.

The brokerage firm has designated the company's stock as one of its top picks in the Exploration and production sector as in addition to the robust upside, the stock provides an FY24E dividend yield of 9%.

To note, MARI is currently trading at an FY24E Price to Earnings (P/E) of 3.9x, compared to the company’s own 10-year average P/E of 8x.

.jpeg)

MARI has demonstrated consistent production growth, with total gas production expected to end the year at 860MMCFD (FY24E), a CAGR of 4% since FY16 (compared to the industry’s annual decline of 3%).

To note, the company significantly increased its production profile during the outgoing year (+13%), largely marked by the full commissioning of the SGPC facility during 4QFY23 (+110 MMCFD).

Further, with the onset of Shewa-1 (+50 MMCFD) by late FY24 alongside inclusions of several wells from Mari Ghazij and horizontal reservoirs (Mari 122- 124H) by FY24/25E, JS Global expects the company’s total gas production to top the 900MMCFD mark by FY25F.

Adding further to the positive signals, the company's expansion of its exploration acreage has been one of the most aggressive in the industry, with the company acquiring 16 blocks in the last three years, including the Abu Dhabi block (with consortium of OGDC, PPL and GHPL).

This aggressive development and exploration strategy has led to the discovery of four major producing reservoirs (Mari Horizontal in HRL, Ghazij, Bannu West, Hilal & Iqbal) since July 2020, culminating to a reserve replacement ratio of over 100% during FY21-23.

Moreover, MARI continues to actively develop its flagship reservoir i.e. Mari HRL through the Mari Revitalization program to extend the field’s recoverable base.

Overall, Mari Gas Field in Sindh boasts total recoverable reserves of 4.37 TCF, resulting in an estimated production life of 15 years, assuming production of 800MMCFD annually.

Although, circular debt concerns remain contained seeing MARI's outstanding receivables grow at a rapid pace over the past 12 months (1QFY24: Rs60.8bn, up 81% YoY), especially after initiation of supplying pipeline gas to SNGPL (+100MMCFD since FY22), liquidity concerns similar to those seen in gas heavy E&P companies have taken shape.

Concerns, however, seem to be somewhat overplayed since major gas-price rationalization efforts have already begun, with bi-annual consumer gas price reviews in effect (on persistence by IMF).

Going forward, MARI’s permeate gas supplies are important for the fertilizer sector, and subsequently for the country’s food security sustainability.

JS Global believes authorities to be up to the task of ensuring prioritized gas collections for the company to support the field development.

Finally, the affected revenues towards the problematic gas utility only account for 15-20% of total sales, compared to OGDC and PPL: with over 45%.

Hence future pay-outs (FY24-25E payout: 40%) and operational activities are expected to remain unaffected going forward.

Due to major expansion, the company is exposed to an additional 15% royalty charge on gas revenues from the field post renewal in 1HFY25.

This development leads to a negative impact of 8%/-18% for FY25/26 earnings, respectively.

Annualized growth in earnings, however, continues to remain robust, with a CAGR of +7% between FY25-FY30F, primarily driven by dollarized revenues alongside strong production life.

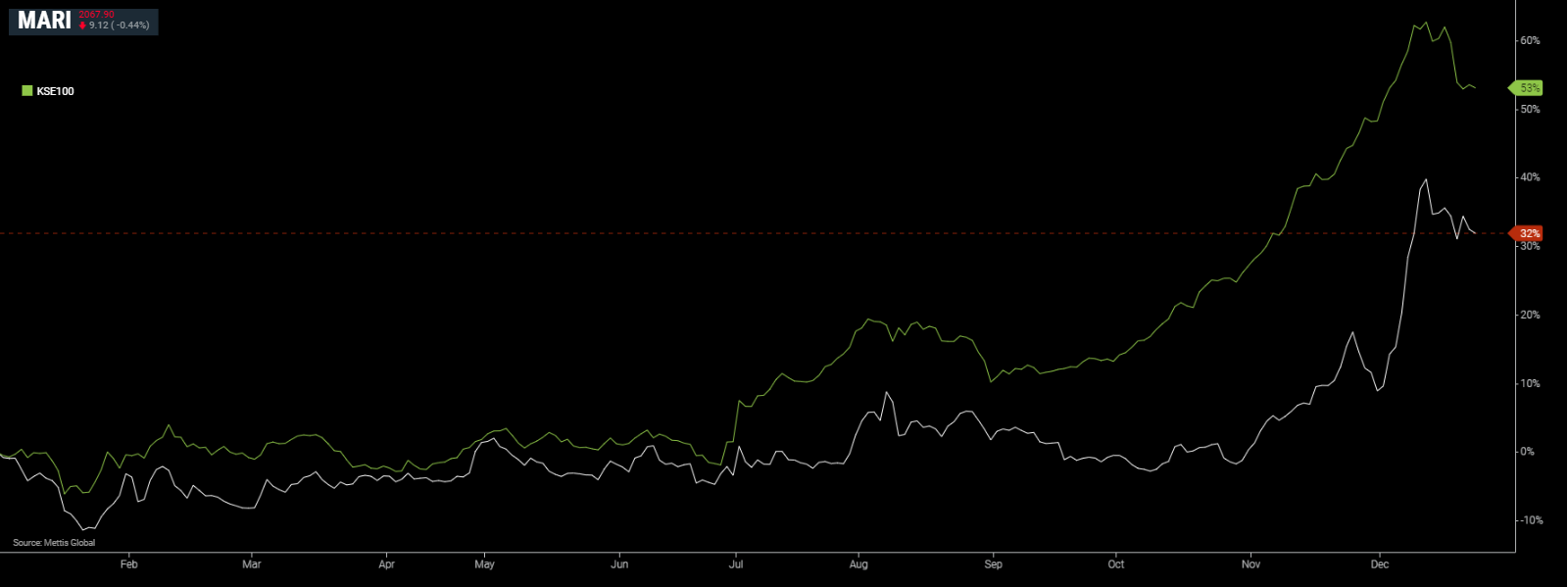

MARI and KSE-100 YTD Performance

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,405.00 | 64,405.00 63,875.00 | 190.00 0.30% |

| BRENT CRUDE | 98.70 | 101.19 95.13 | -1.99 -1.98% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 121.10 121.10 | 0.70 0.58% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.47 | 92.83 87.68 | -1.72 -1.87% |

| SUGAR #11 WORLD | 14.76 | 14.79 14.54 | 0.07 0.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|