Weekly Market Roundup

_20260315071925394_f6893c.jpeg?width=950&height=450&format=Webp)

MG News | March 15, 2026 at 12:25 PM GMT+05:00

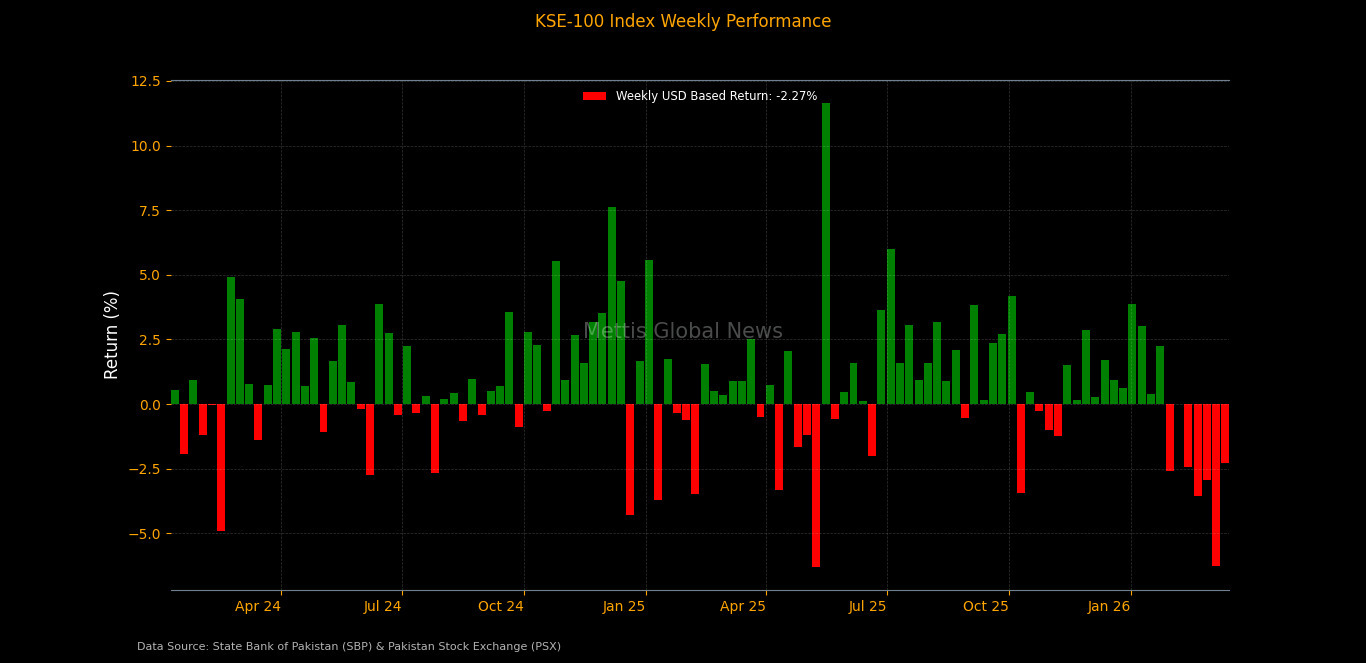

March 15, 2026 (MLN): Pakistan’s equity market

remained under selling pressure during the outgoing week, as the benchmark KSE‑100

Index closed at 153,866.17, compared to 157,496.10 recorded on March

6, 2026.

The index shed 3,629.93 points over the week,

translating into a decline of 2.30% week-on-week (WoW).

Investor sentiment weakened during the week amid uncertainty

surrounding the review talks with the International Monetary Fund (IMF)

and rising global oil prices following escalating geopolitical tensions in the

Middle East.

The uncertain external environment prompted investors to

adopt a cautious stance, ._20260315071934314_0bc61d.jpeg)

Market Capitalization

Market capitalization also declined in line with the

benchmark index. The total listed market cap fell to Rs4.51 trillion on

March 13, 2026, compared to Rs4.62tr recorded on March 6, 2026, marked

a contraction of Rs112bn or 2.42% WoW.

In dollar terms, total market capitalization declined

by $395.73m, reaching $16.15bn compared to $16.54bn in the

previous week._20260315071916270_a8295d.jpeg)

Meanwhile, dollar-adjusted returns stood at negative

2.27%, compared to negative 6.26% in the prior week, suggesting that

the latest decline was relatively milder compared to the sharp sell-off

witnessed earlier.

![]()

On the macroeconomic front, car sales in Pakistan, including

LCVs, vans, and jeeps, increased

41.7% YoY to 17,121 units in February 2026 from 12,084

units a year earlier, according to the Pakistan Automotive Manufacturers

Association (PAMA).

However, sales fell 25.7% MoM from 23,055 units in

January, while 8MFY26 sales rose 43.2% YoY to 128,489 units.

Pakistan received $3.29bn

in workers’ remittances in February 2026, down 5.1% MoM from $3.46bn

in January, according to data released by the State Bank of Pakistan

(SBP), while cumulative inflows during 8MFY26 rose 10% YoY to $26.5bn.

The UAE emerged as the largest source with $696.24m,

followed by Saudi Arabia ($685.50m), the UK ($532.03m), and the USA

($319.46m).

Pakistan’s Business Confidence Index (BCI) slightly

declined to 55.3

in February 2026, according to a survey by the State Bank of

Pakistan (SBP) and Institute of Business Administration (IBA), as

weaker services sector sentiment offset improved industry confidence.

Pakistan’s Consumer Confidence Index (CCI) rose

1.4 points to 43 in February 2026 from 41.6 in January,

according to a survey released by the State Bank of Pakistan (SBP), as

households’ financial conditions and expectations about economic conditions

improved while inflation expectations eased.

The State Bank of Pakistan’s MPC held the policy

rate at 10.5% on March 9, 2026, citing Middle East tensions driving global

fuel prices and uncertainty, even as domestic inflation rose to 7% and FY26 GDP

growth remains on track at 3.75–4.75%.

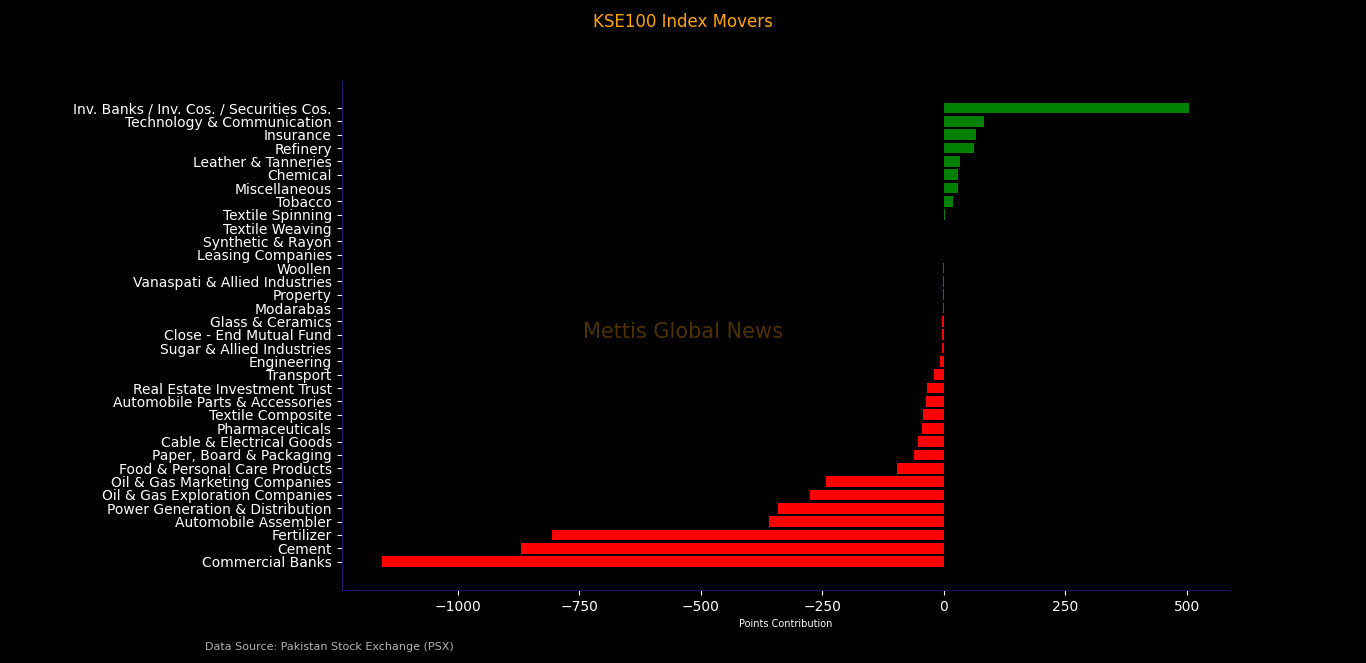

Index Movers

Sector-wise performance highlighted broad-based pressure

across the market.

Commercial banks emerged as the largest drag on the

benchmark, wiping out 1,156.27 index points, followed by cement,

which shaved 869.99 points.

Fertilizer stocks reduced the index by 806.34

points, while automobile assemblers trimmed 359.91 points.

Other major negative contributors included power

generation and distribution (-341.49 points), oil and gas exploration

companies (-274.34 points), and oil marketing companies (-241.82 points).

Additional pressure came from food and personal care

products, paper and packaging, cable and electrical goods, pharmaceuticals,

textile composite, and automobile parts, reinforcing the broad-based nature

of the weekly decline.

On the positive side, only a few sectors managed to provide

support to the benchmark.

Investment banks and securities companies added 504.84

points, followed by technology and communication (83.23 points), insurance

(65.94 points), and refineries (61.50 points).

Smaller positive contributions also came from chemical,

leather and tanneries, miscellaneous, and tobacco sectors.

At the company level, a handful of stocks managed to record

positive contributions.

Among the gainers, ENGROH added 514.93 points,

followed by SYS which contributed 139.80 points, while AICL

added 65.94 points.

Other notable positive contributors included BAHL (49.07

points), ATRL (48.86 points), HINOON (42.92 points), SRVI

(32.85 points), LOTCHEM (23.74 points), and TRG (23.44 points).

Despite these gains, the benchmark remained under

significant pressure due to steep declines in several heavyweight stocks.

UBL emerged as the largest drag on the index, wiping

out 899.42 points, followed by FFC, which erased 618.89 points.

Other major negative contributors included LUCK (-362.37

points), HUBC (-309.99 points), SAZEW (-208.84 points), PSO

(-197.98 points), FCCL (-136.04 points), DGKC (-127.05 points).

PPL (-119.77 points), FATIMA (-106.18 points),

NBP (-104.74 points), and MCB (-92.26 points).

The heavy losses across large-cap stocks reflected strong

selling pressure in key index-heavy sectors._20260315071854749_a86f77.jpeg)

FIPI / LIPI

Foreign investment flows continued to exert pressure on the

market during the week.

Under Foreign Portfolio Investment (FIPI), foreign

investors remained net sellers with an outflow of $13.43m.

The majority of the selling came from foreign corporates,

which offloaded $18.61m worth of equities.

Meanwhile, overseas Pakistanis provided buying support of

$5.19m, while foreign individuals recorded a marginal net outflow of

$14k.

On the other hand, local investors absorbed the entire

foreign outflow, resulting in a matching net inflow of $13.43m under Local

Portfolio Investment (LIPI).

Among local participants, individual investors emerged as

the largest buyers with net purchases of $11.65m, followed by banks and

DFIs ($10.76m) and other organizations ($6.39m).

Mutual funds also recorded net buying of $2.86m,

while insurance companies posted a marginal inflow of $34k.

Meanwhile, companies recorded the largest selling with an

outflow of $16.47m, followed by broker proprietary trading desks

($1.51m) and NBFCs ($0.28m)._20260315071902288_c6419e.jpeg)

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

_20260711124603464_8ff65f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,210.00 | 64,680.00 62,605.00 | -875.00 -1.37% |

| BRENT CRUDE | 78.44 | 79.80 77.28 | 2.43 3.20% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.76 | 75.08 72.61 | 2.35 3.29% |

| SUGAR #11 WORLD | 14.71 | 14.98 14.65 | -0.17 -1.14% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|