Weekly Market Roundup

MG News | April 11, 2026 at 01:15 PM GMT+05:00

April 11, 2026 (MLN): Pakistan’s equity market

staged a strong rebound after weeks of persistent decline, as the benchmark

KSE-100 Index closed at 167,191.38 on 10 April 2026, up sharply from 150,398.71

recorded on 3 April 2026.

The index gained 16,792.67 points, translating into an

11.17% week-on-week (WoW) increase.

Investor sentiment was strongly lifted by

Pakistan-facilitated peace talks between the United States and Iran, which

eased regional geopolitical tensions and reduced risk premiums across emerging

markets, driving broad-based buying activity in the local equity market._20260411081051712_849964.jpeg)

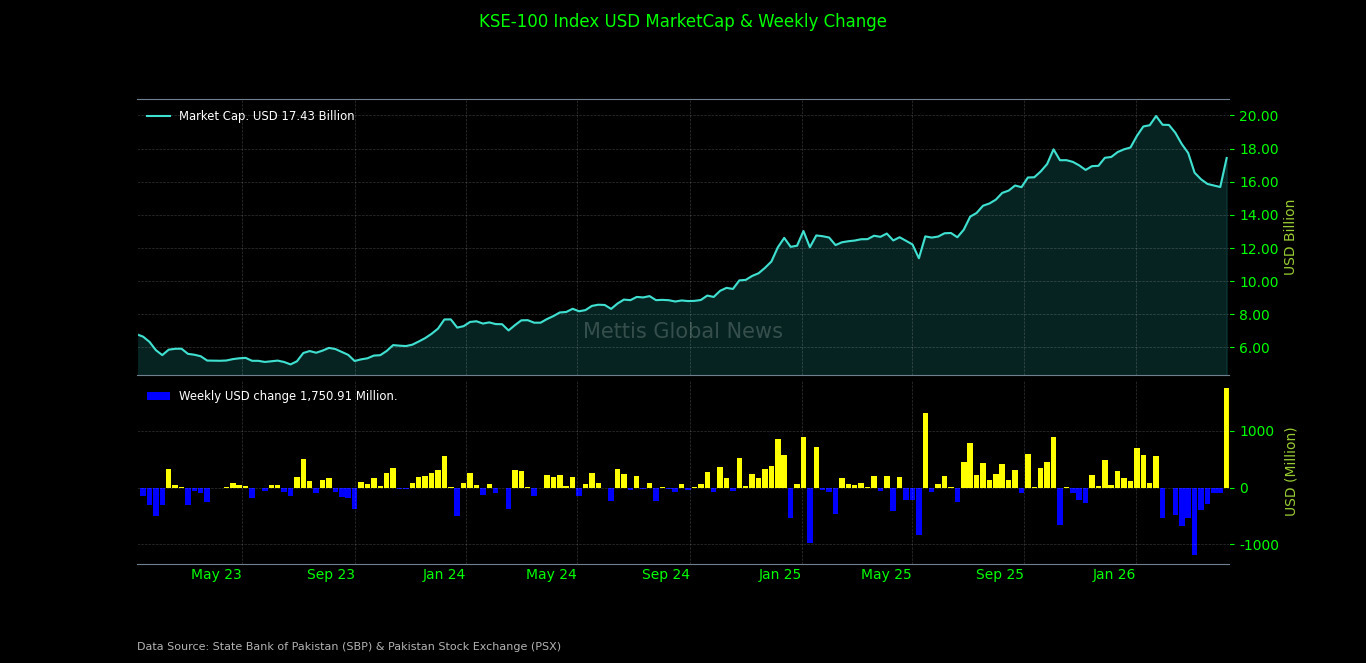

Market Capitalization

Total market capitalization witnessed a significant increase

in line with the sharp recovery in the benchmark index. On 10 April 2026,

market cap surged to Rs4.863 trillion, compared to Rs4.376tr on 3 April 2026,

reflecting a substantial gain of Rs487.09bn or 11.13% WoW.

In USD terms, market capitalization rose to $17.43bn from

$15.68bn in the previous week, indicating improved foreign investor confidence

alongside currency stability.

Dollar-adjusted returns improved significantly, moving from

-0.8376% to +11.2019% WoW, reflecting a strong recovery both in local currency

and dollar terms._20260411081018731_191a13.jpeg)

On the macroeconomic front, National Savings inflows slowed

in February 2026, with net mobilisation dropping 23%

MoM to Rs20.69bn amid weaker contributions across key schemes.

Despite the dip, cumulative FY26 inflows remain strong at

Rs203.8bn, highlighting a sustained recovery from the heavy outflows of

previous years.

Workers’ remittances rose 16.5%

MoM to $3.83bn in March 2026, led by strong inflows from Saudi Arabia,

though remaining 5% lower on a yearly basis.

Central government debt

rose 9.4% YoY to Rs79.88tr in February 2026, driven by increased domestic

and external borrowing to finance the fiscal deficit.

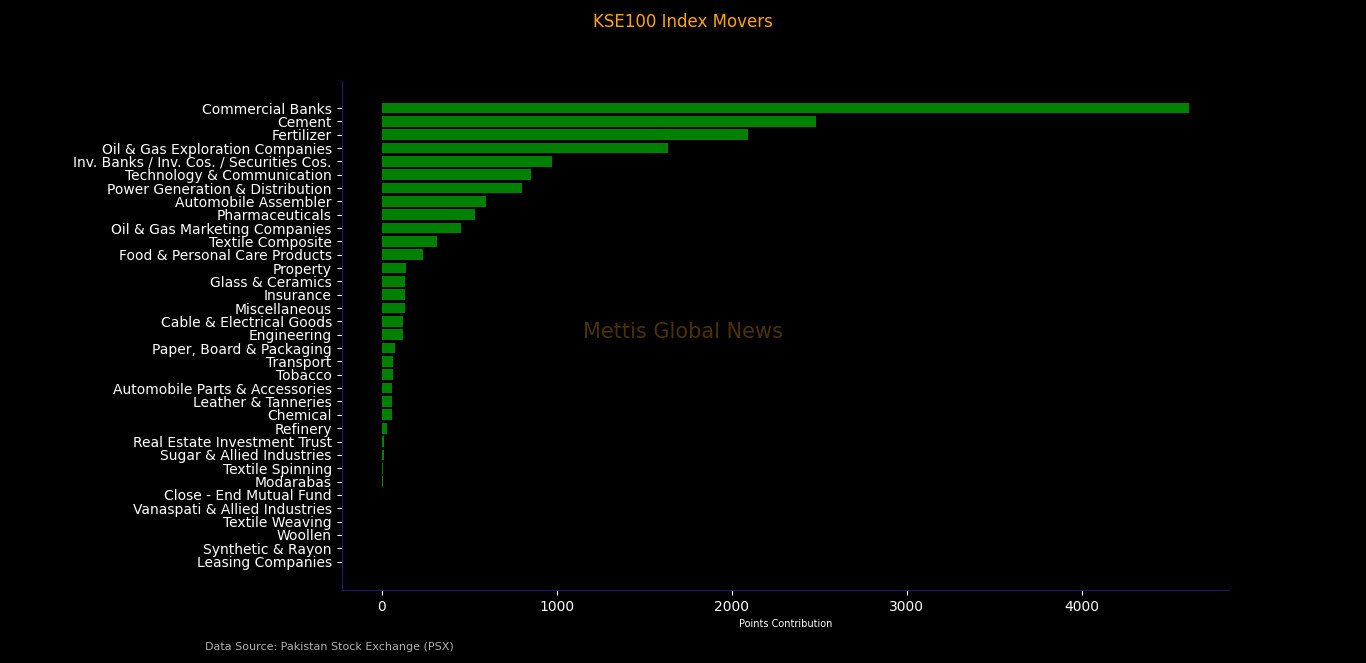

Index Movers

Sector-wise, commercial banks emerged as the largest

positive contributor, adding 4,613.06 points to the benchmark, driven by strong

gains in major banking stocks amid attractive valuations and earnings

expectations.

Cement followed as the second-largest contributor, adding

2,479.71 points, supported by improved sentiment on construction activity and

declining input cost expectations.

Fertilizer added 2,091.60 points, while oil & gas

exploration companies contributed 1,633.75 points, benefiting from stable

energy prices and strong earnings outlook.

Investment banks, investment companies, and securities

companies added 970.72 points, while technology & communication (+851.58

points) and power generation & distribution (+801.18 points) also provided

notable support.

Other key contributors included automobile assemblers

(+596.31 points), pharmaceuticals (+534.66 points), oil & gas marketing

companies (+452.32 points), textile composite (+313.33 points), and food &

personal care products (+237.13 points), showing broad-based participation

across sectors.

Even smaller sectors such as insurance, engineering, cable

& electrical goods, and transport posted gains, highlighting the strength

of the rally. Leasing companies remained the only marginal laggard.

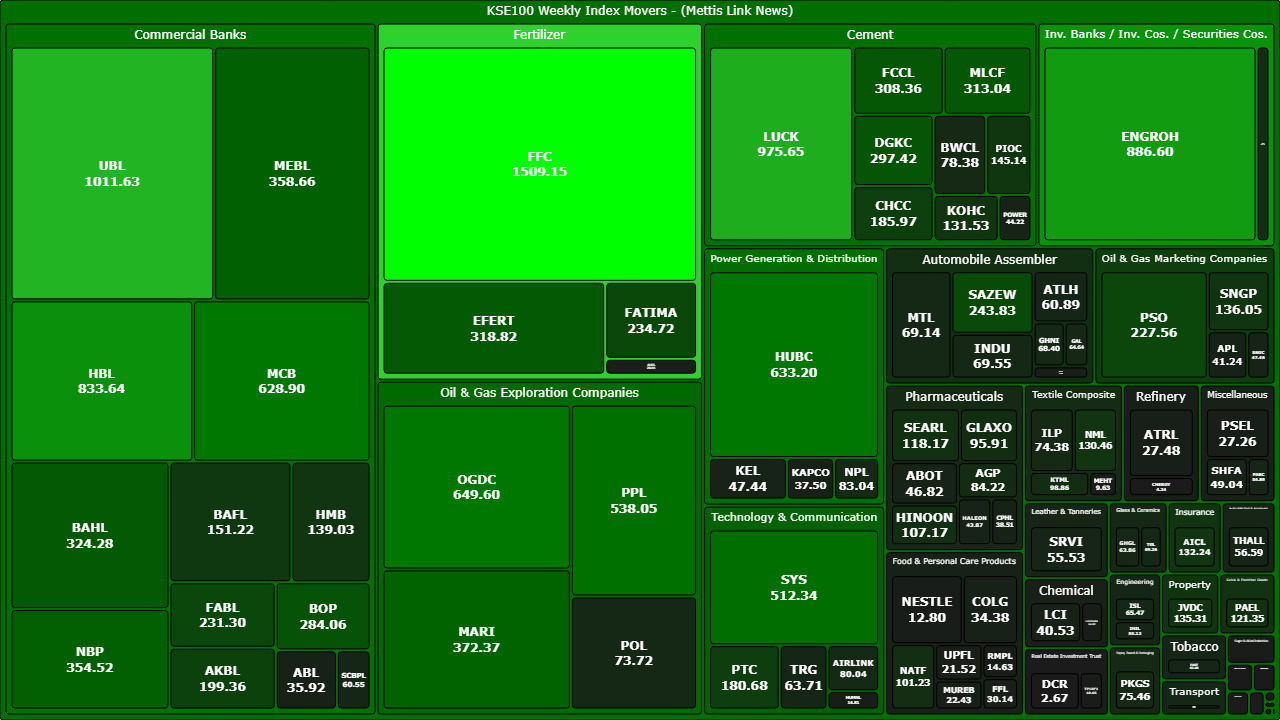

At the individual stock level, FFC led the gains,

contributing 1,509.15 points, followed by UBL (+1,011.63 points) and LUCK

(+975.65 points).

Other major contributors included ENGROH (+886.60 points),

HBL (+833.64 points), OGDC (+649.60 points), HUBC (+633.20 points), MCB

(+628.90 points), and PPL (+538.05 points).

Technology and energy stocks also remained strong, with SYS

(+512.34 points) and MARI (+372.37 points) adding to the upside.

Additional support came from MEBL, NBP, BAHL, EFERT, MLCF,

FCCL, DGKC, BOP, PSO, AKBL, BAFL, HMB, and SNGP among others, indicating

widespread participation from index-heavy stocks.

FIPI / LIPI

Foreign investment flows remained negative despite the

market rally. Under Foreign Institutional Portfolio Investment (FIPI), foreign

investors were net sellers with an outflow of Rs1.22bn ($4.40m).

The bulk of the selling came from foreign corporates, which

offloaded Rs1.92bn, while overseas Pakistanis provided partial support with net

buying of Rs703.31m. Foreign individuals remained marginal sellers.

On the domestic side, Local Portfolio Investment (LIPI)

absorbed the foreign outflows, resulting in a matching net inflow of Rs1.22bn

($4.40m).

Among local participants, mutual funds emerged as the

largest buyers with net purchases of Rs15.02bn, playing a key role in driving

the market rally.

On the other hand, banks & DFIs (-Rs8.04bn), insurance

companies (-Rs3.30bn), broker proprietary trading (-Rs1.25bn), and individuals

(-Rs912.15m) remained net sellers.

In the debt market, banks & DFIs showed strong

participation with net inflows, while mutual funds recorded outflows._20260411081009296_ddf3c9.jpeg)

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

_20260711124603464_8ff65f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,210.00 | 64,680.00 62,605.00 | -875.00 -1.37% |

| BRENT CRUDE | 78.44 | 79.80 77.28 | 2.43 3.20% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.76 | 75.08 72.61 | 2.35 3.29% |

| SUGAR #11 WORLD | 14.71 | 14.98 14.65 | -0.17 -1.14% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|