Weekly Market Roundup

_20260516095302187_fa0ba0.jpeg?width=950&height=450&format=Webp)

MG News | May 16, 2026 at 03:02 PM GMT+05:00

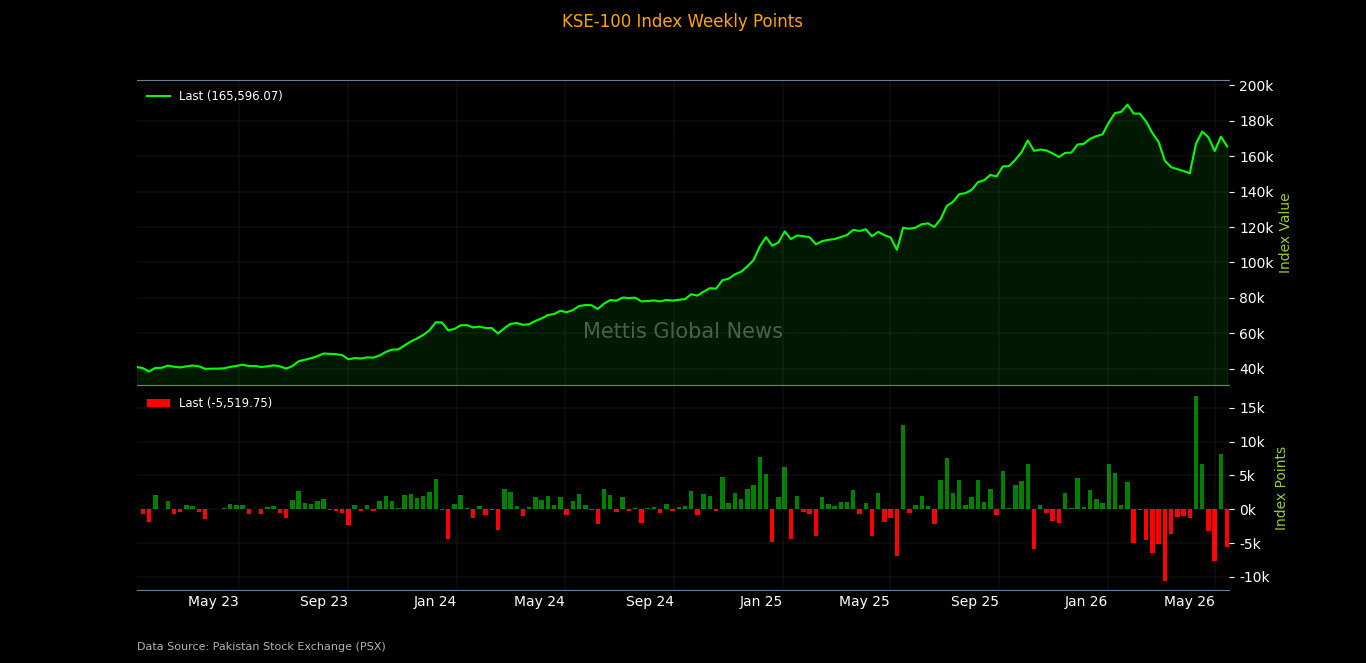

May 16, 2026 (MLN): Pakistan’s equity market

witnessed a sharp correction during the week ended May 15, 2026, with the

benchmark KSE-100 Index closing at 165,596.07, significantly lower than

171,115.82 recorded on May 08, 2026.

The index declined by 5,519.74 points, translating into a

3.23% week-on-week (WoW) loss, as investors stayed largely cautious and refrained from active participation due to rising oil prices and ongoing geopolitical uncertainties.

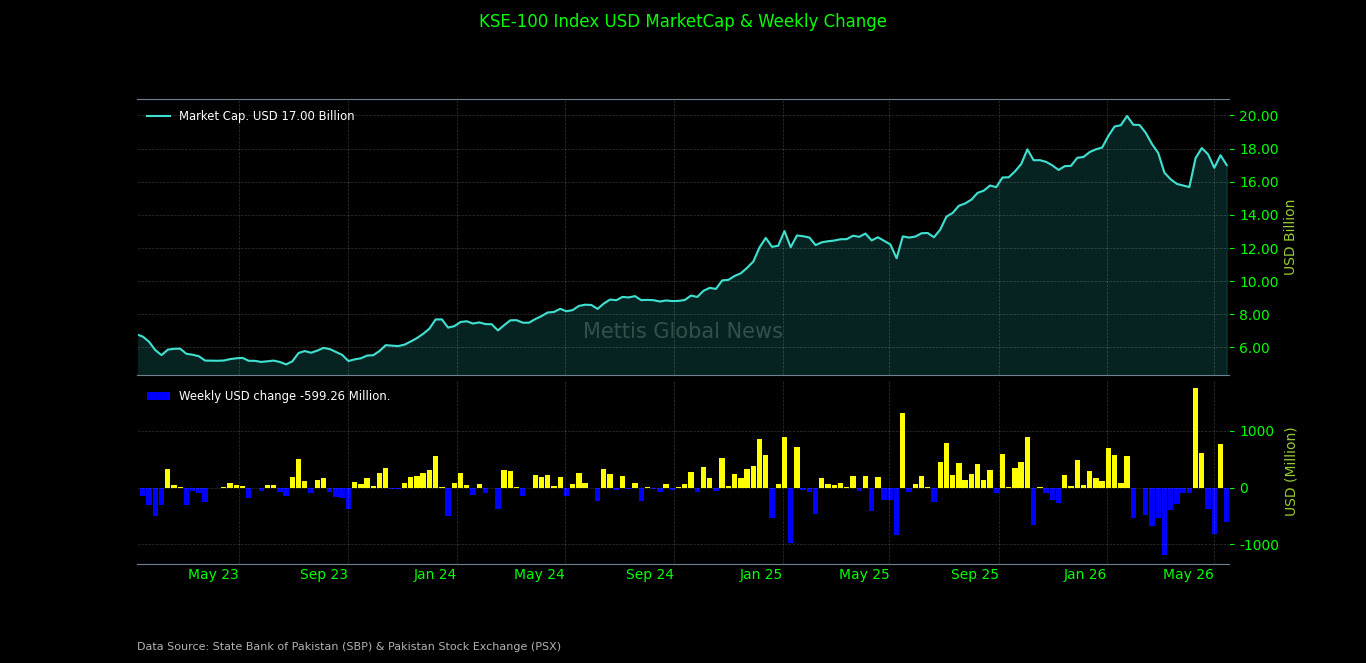

Market Capitalization

Total market capitalization declined in line with the

benchmark index performance. As of May 15, 2026, market capitalization stood at

Rs4.737 trillion, compared to Rs4.906tr on May 08, 2026, marking a decrease of

Rs168.60bn or 3.44% WoW.

In USD terms, market capitalization fell to $17.00bn from

$17.60bn in the previous week, reflecting erosion in overall market value amid

broad-based selling pressure.

Dollar-adjusted returns also turned negative, clocking in at

negative 3.19% WoW, compared to positive 5.01% in the prior week, indicating

weakening investor returns in both local and foreign currency terms._20260516095247911_3fb445.jpeg)

On the macroeconomic front, Pakistan’s National Savings

Schemes recorded net

inflows of Rs22.88bn in March 2026, up 10.6% from February, signaling

continued recovery in saver confidence amid improving returns.

Pakistan’s external debt and liabilities stood

at $137.56bn by the end of Q3FY26, declining 0.34% QoQ but rising 5.73%

YoY, according to State Bank of Pakistan data.

Pakistan’s central government debt

rose 9.28% YoY to Rs80.52tr in March 2026, driven by higher domestic and

external borrowing to finance the fiscal deficit.

Pakistan’s auto sales more than doubled in April 2026, surging

106.9% YoY to 22,015 units, driven by strong demand across passenger cars,

SUVs, and tractors amid improving consumer confidence and economic activity.

Pakistan’s workers’ remittances fell

7.6% MoM to $3.54bn in April 2026 amid Middle East tensions, though inflows

remained 11.4% higher YoY, keeping cumulative 10MFY26 remittances at $33.86bn.

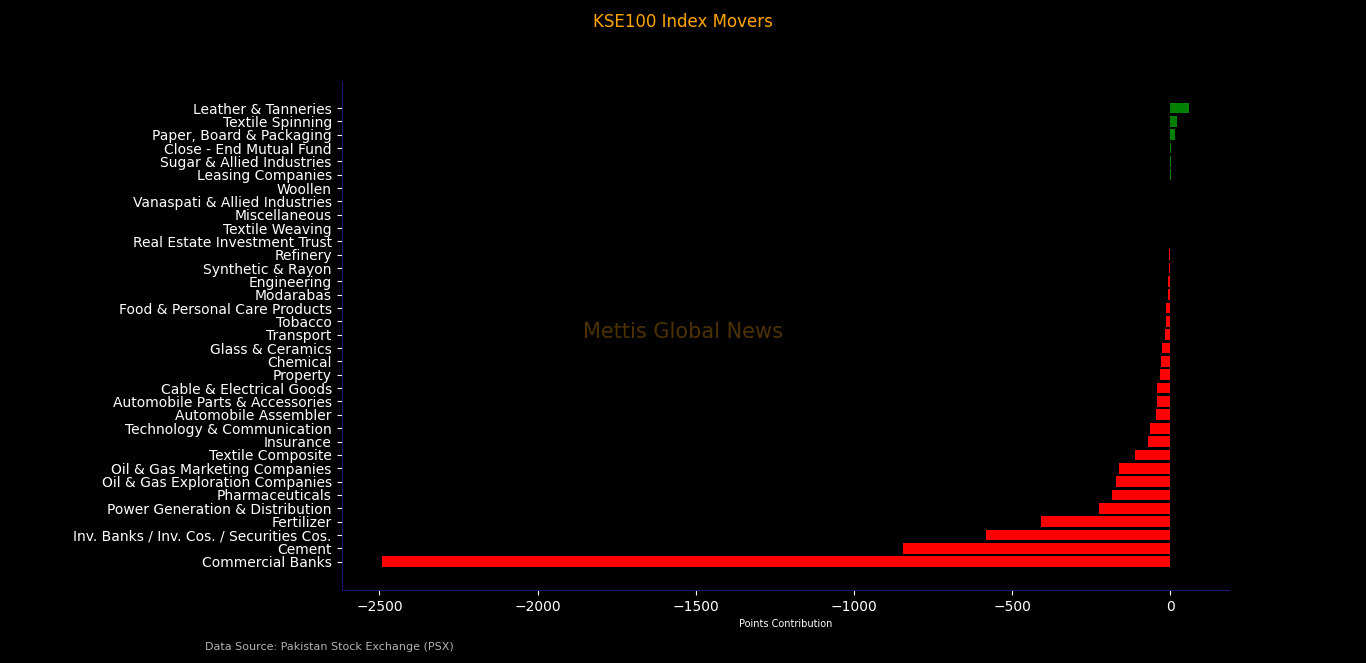

Index Movers

Sector-wise, the decline remained heavily concentrated in

index-heavy sectors.

Commercial banks emerged as the largest drag on the

benchmark index, wiping out 2,492.07 points amid heavy selling pressure in

major banking names and profit-taking across the sector.

Cement stocks trimmed 845.62 points from the index, while

investment banks/investment companies/securities companies erased 583.33 points

during the week.

Fertilizer dragged the benchmark by 409.62 points, followed

by power generation & distribution (-226.94 points), pharmaceuticals

(-184.87 points), oil & gas exploration companies (-172.65 points), and oil

& gas marketing companies (-162.38 points).

Additional negative contributions came from textile

composite (-110.26 points), insurance (-71.74 points), technology &

communication (-63.91 points), automobile assemblers (-44.22 points),

automobile parts & accessories (-43.27 points), cable & electrical

goods (-42.26 points), and property (-32.14 points), highlighting the

broad-based nature of the market decline.

Other lagging sectors included chemical (-30.44 points),

glass & ceramics (-27.96 points), transport (-16.01 points), tobacco

(-14.12 points), food & personal care products (-12.58 points), modarabas

(-8.92 points), engineering (-8.26 points),

synthetic & rayon (-5.61 points), refinery (-4.87

points), real estate investment trust (-1.86 points), textile weaving (-1.40

points), miscellaneous (-0.40 points), and vanaspati & allied industries

(-0.27 points).

On the positive side, only a handful of sectors managed to

close in green territory, with leather & tanneries adding 58.97 points,

followed by textile spinning (+20.52 points), paper, board & packaging

(+14.03 points),

close-end mutual fund (+2.78 points), sugar & allied

industries (+1.39 points), leasing companies (+0.40 points), and woollen (+0.16

points), indicating limited strength in selective pockets of the market.

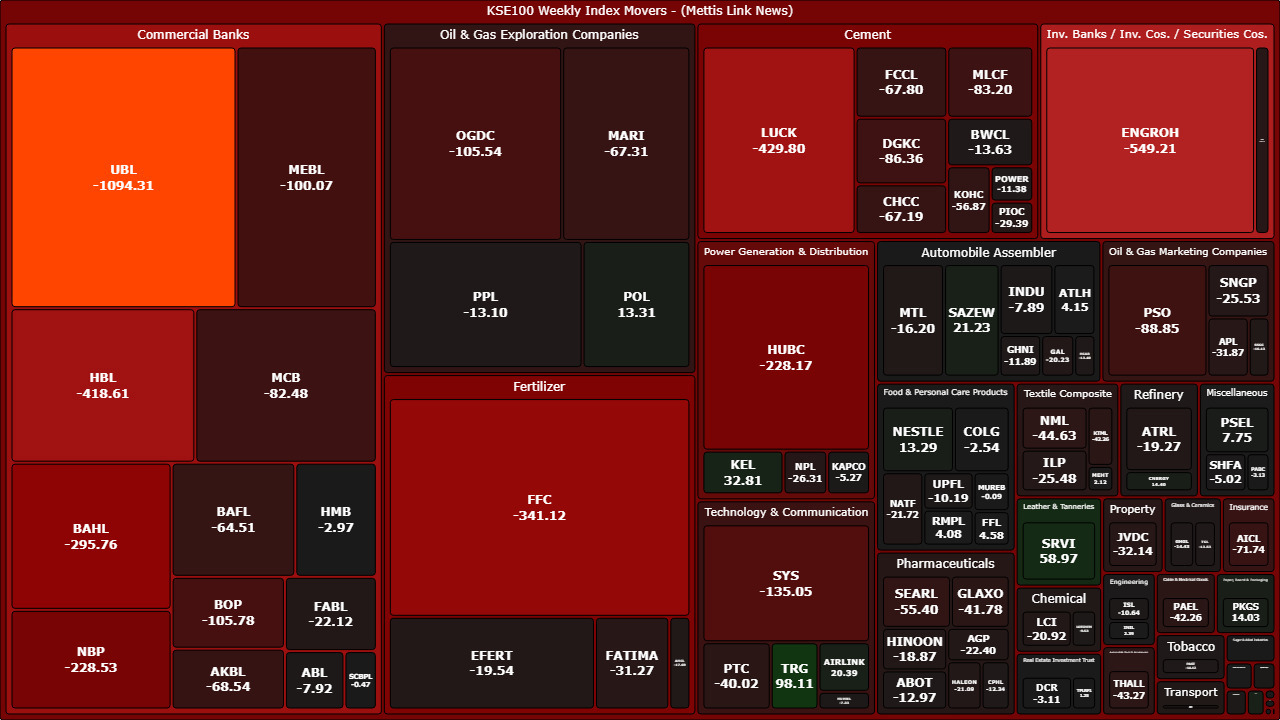

Scrip-wise, the downside was dominated by heavyweight

banking, cement, fertilizer, and investment company stocks.

United Bank Limited emerged as the largest negative

contributor, dragging the index by 1,094.31 points, followed by Engro Holdings

(-549.21 points), Habib Bank Limited (-418.61 points), Fauji Fertilizer Company

(-341.12 points), and Bank AL Habib (-295.76 points).

Other major laggards included National Bank of Pakistan

(-228.53 points), HUBCO (-228.17 points), Systems Limited (-135.05 points),

Bank of Punjab (-105.78 points),

Oil & Gas Development Company (-105.54 points), Meezan

Bank (-100.07 points), Pakistan State Oil (-88.85 points), DG Khan Cement

(-86.36 points), Maple Leaf Cement (-83.20 points), and MCB Bank (-82.48

points).

Additional pressure came from Adamjee Insurance, Askari

Bank, Fauji Cement, Mari Petroleum, Cherat Cement, Bank Alfalah, Kohat Cement,

The Searle Company, Nishat Mills, Thal Limited, Pak Elektron, GlaxoSmithKline

Pakistan,

Pakistan Telecommunication Company, Pakistan Stock Exchange,

and Lucky Cement, reflecting broad weakness across banking, cement, fertilizer,

technology, pharmaceutical, and energy sectors.

On the upside, gains remained limited and concentrated in a

handful of stocks.

TRG Pakistan led the gainers, contributing 98.11 points to

the index, followed by Service Industries (+58.97 points), K-Electric (+32.81

points), Sazgar Engineering Works (+21.23 points), and Gadoon Textile Mills

(+20.52 points).

Other positive contributors included Air Link Communication,

Cnergyico PK, Packages Limited, Pakistan Oilfields Limited, Nestlé Pakistan,

Pakistan Services Limited, FrieslandCampina Engro Pakistan, Atlas Honda, and

Rafhan Maize Products, reflecting selective buying interest in a few defensive

and growth-oriented names despite the broader market weakness.

FIPI/LIPI

Foreign investors remained marginal net buyers during the

week, with total net foreign buying in the equity segment standing at Rs9.42

million ($33,768).

Within foreign flows, overseas Pakistanis recorded net

buying of Rs1.55bn ($5.54m), which was largely offset by net selling from

foreign corporates amounting to Rs1.51bn ($5.42m). Foreign individuals also

remained net sellers during the week.

On the local side, individuals emerged as the largest net

buyers with inflows of Rs3.96bn, followed by broker proprietary trading at

Rs298.66m and NBFCs at Rs57.46m.

Meanwhile, mutual funds remained the largest net sellers,

offloading equities worth Rs2.48bn, followed by companies with net selling of

Rs1.41bn. Insurance companies, banks/DFIs, and other organizations also

remained net sellers during the week._20260516095243973_6b559b.jpeg)

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,306.41 279.49M | 0.91% 1613.49 |

| ALLSHR | 108,429.41 523.83M | 0.84% 902.02 |

| KSE30 | 53,456.60 100.55M | 0.82% 433.72 |

| KMI30 | 256,308.59 94.07M | 0.60% 1519.33 |

| KMIALLSHR | 70,487.96 354.79M | 0.79% 550.82 |

| BKTi | 48,585.18 22.55M | 1.29% 618.54 |

| OGTi | 37,017.30 4.03M | 0.50% 183.64 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 62,610.00 | 63,045.00 62,390.00 | 245.00 0.39% |

| BRENT CRUDE | 75.62 | 77.00 75.59 | -1.46 -1.89% |

| RICHARDS BAY COAL MONTHLY | 115.00 | 0.00 0.00 | 0.50 0.44% |

| ROTTERDAM COAL MONTHLY | 125.90 | 125.90 125.90 | -0.15 -0.12% |

| USD RBD PALM OLEIN | 1,157.50 | 1,157.50 1,157.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 71.82 | 73.18 71.80 | -1.39 -1.90% |

| SUGAR #11 WORLD | 13.86 | 13.96 13.83 | -0.09 -0.65% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|