PSX rebounds in April after brutal slide

MG News | May 02, 2026 at 06:36 PM GMT+05:00

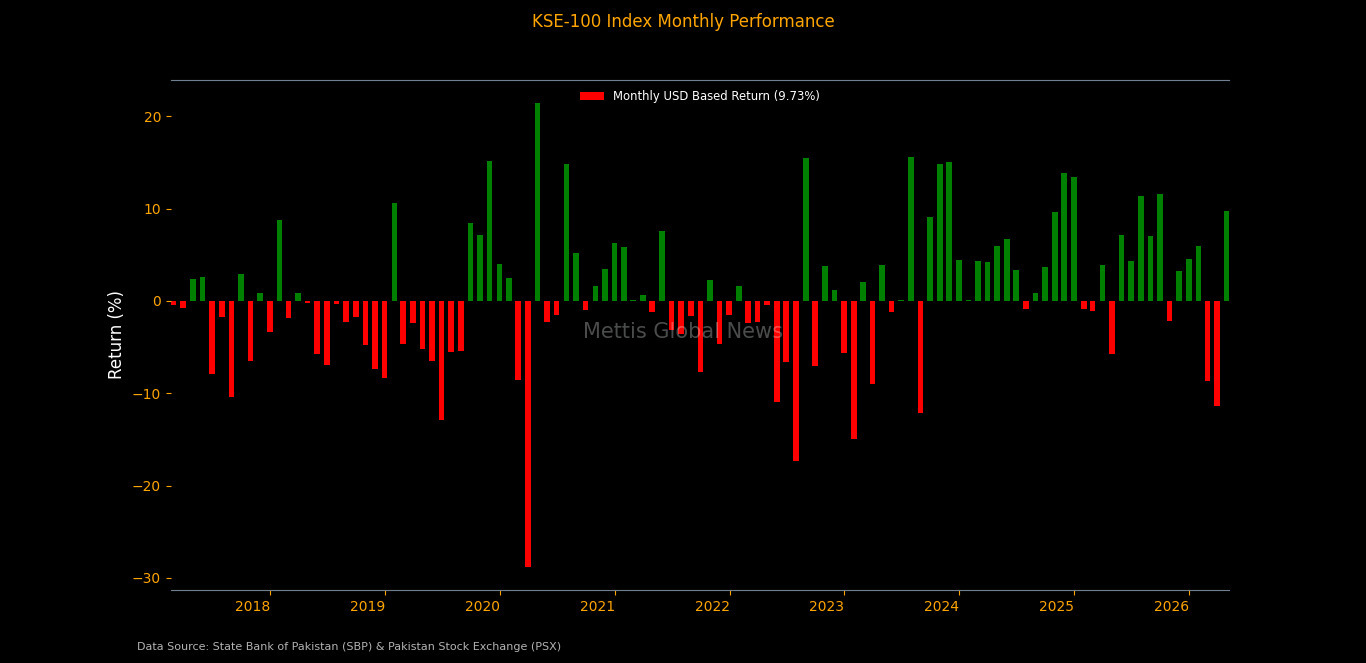

May 02, 2026 (MLN): After enduring back-to-back double-digit monthly losses, the sharpest in years, Pakistan's equity market staged its most decisive single-month rebound of FY26 in April, fuelled first by geopolitical hope and then by the resilient conviction of local investors who refused to let the market fall further.

The scoreboard heading into April 2026 made for grim reading. February had handed investors an –8.75% loss, and March delivered an even crueller blow of 11.50%, wiping out nearly a fifth of the index's value in just sixty trading days.

The KSE-100 had shed over 35,000 points from its January peak, market capitalisation in dollar terms had contracted from a heady USD 19.4 billion to a bruised USD 15.5 billion, and sentiment was running cold.

April changed that. The index closed at 162,994, a gain of 14,251 points and a 9.58% return in PKR terms (9.73% in USD).

The Pakistani Rupee remained broadly stable against the US Dollar in April, with the exchange rate moving marginally to 278.77 from 279.15, an appreciation of less than 0.14%.

This currency stability played a meaningful role in ensuring that the equity gain translated almost entirely into USD returns (+9.73%), making April one of Pakistan's strongest months for dollar-denominated investors in FY26.

The FX calm stands in contrast to the

acute currency pressures seen in the difficult years of 2022–2023, when

devaluations routinely eroded equity gains for offshore investors.

The market capitalisation recovered to USD 16.84 billion, clawing back USD 1.38 billion of lost ground.

Yet the monthly story was far from linear. It was a tale of two halves, a surge and a surrender, stitched together by events stretching from a ceasefire table in the Gulf to a State Bank boardroom in Karachi.

_20260430164143315_3b38f2.jpeg)

April opened with a bang. A 4.55% gain on the first trading day signalled that buyers had returned.

The real firecracker came on April 8, when optimism surrounding a potential US–Iran ceasefire lit a fire under the market, delivering a staggering single-session gain of 9.32%, the largest daily move of the entire fiscal year.

In one session, the market recovered

nearly two-thirds of what it had taken the whole of February to erase.

But the euphoria had a short shelf life. By April 13, a –3.95% decline confirmed that momentum was fragile.

Weaker-than-expected corporate results as quarterly earnings trickled in dampened enthusiasm and renewed geopolitical uncertainty, as ceasefire optimism faded, kept investors cautious. The final two trading sessions of the month (–1.54% on April 29, –1.71% on April 30) underlined the unease.

Buyers dominated the month overall, but they were always one headline away from retreating.

_20260430164116075_1d6d2a.jpeg)

The Macro Backdrop

Equity markets rarely move in isolation, and April's rebound occurred against a macro landscape that was simultaneously improving on some fronts and deteriorating on others.

The most consequential domestic event of the month was the State Bank of Pakistan's decision to raise the policy rate by 100 basis points, pushing the effective rate to 11.5%.

The catalyst was inflation. CPI for April 2026 rose to 10.9%YoY, the highest reading since July 2024, compared to 7.3% in March 2026.

Policy rate hike's aftershocks were visible in the debt market. During the April PIB auction, the government rejected all bids across all tenors as market participants drove yields upward in anticipation of further tightening.

Meanwhile, T-Bill yields rose 40–80 basis points across tenors, with the 1-month bill seeing majority acceptance.

The external story was more encouraging. Pakistan recorded a current account surplus of $1.07 billion in March 2026, bringing the 9MFY26 cumulative balance to a razor-thin surplus of USD 8 million.

Overseas Pakistanis sent home $3.8 billion in March (–5% YoY but +17% MoM), lifting 9MFY26 total remittances to $30.3 billion (+8% YoY).

On the financing front, Pakistan received the final $1 billion tranche of Saudi Arabia's $3 billion support package, while simultaneously executing a strategically significant move, repaying $3.45 billion to the UAE against maturing deposits and exercising the greenshoe option on its Eurobond, bringing total issuance to $750 million.

In a landmark institutional development, the World Bank reclassified Pakistan from its South Asia grouping to the new MENAAP region (Middle East, North Africa, Afghanistan, and Pakistan), effective from fiscal 2026.

Separately, Fitch

affirmed Pakistan's sovereign rating at 'B-' with a Stable Outlook,

providing investors with continued credit floor visibility.

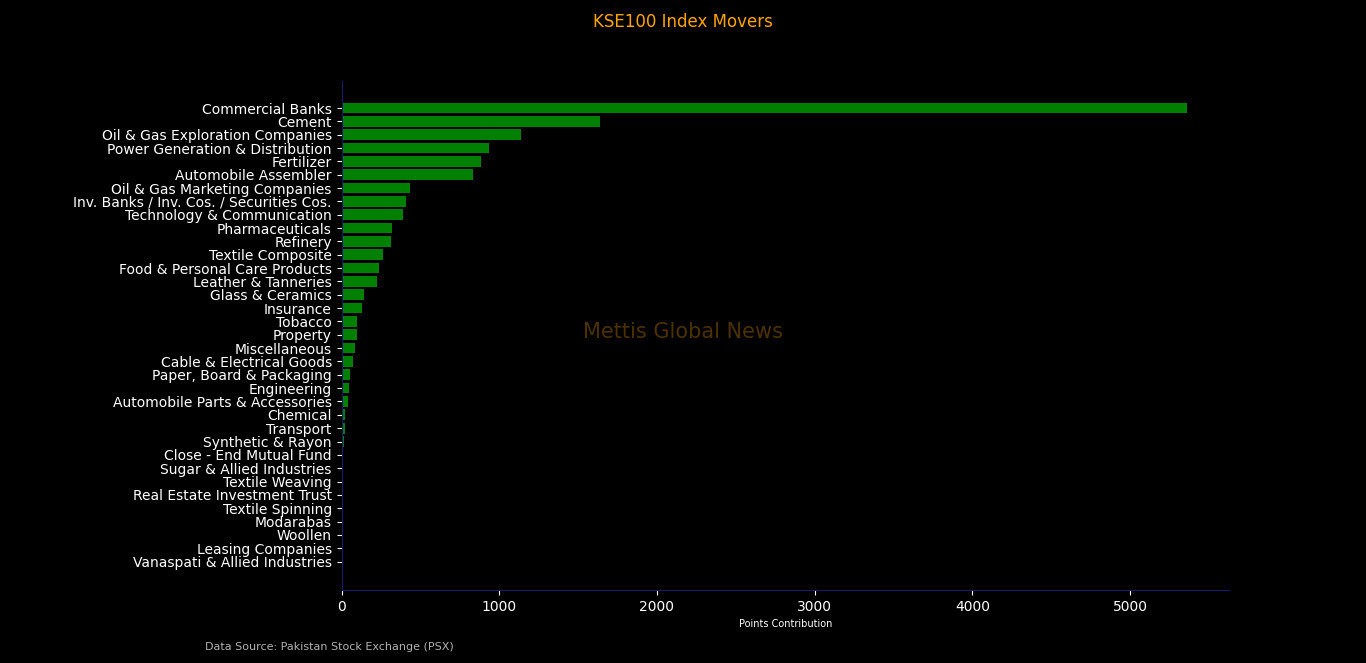

Index Contributors:

Commercial banks were the dominant force behind the KSE-100’s April rally, contributing +5,361.95 index points with the highest sectoral volume of 1.95 billion shares.

Cyclical sectors also provided strong support, with Cement adding +1,639.17 points (761 million shares) and Oil & Gas Exploration contributing +1,135.54 points (329 million shares).

Energy-linked sectors showed active participation, with Power Generation & Distribution contributing +934.89 points (1.54 billion shares), Refineries +314.98 points (1.18 billion shares), and Oil Marketing Companies +435.54 points (530 million shares).

On the consumption and industrial side, Fertilizer added +881.42 points (247 million shares), while Automobile Assemblers contributed +835.25 points (50 million shares), reflecting strong price re-rating despite lower trading volumes. Food & Personal Care (+236.67 points, 188 million shares) added defensive stability.

Growth and export-oriented sectors also contributed steadily, with Technology & Communication adding +389.06 points (509 million shares), Pharmaceuticals +318.92 points (174 million shares), Textile Composite +265.86 points (85 million shares), and Investment Banks/Securities +407.01 points (92 million shares).

Major Scrips

_20260430163912877_97fb38.jpeg)

During the month, overall foreign flows remained marginally net positive during April, with the aggregate FIPI recording a net inflow of $1.14 million. However, the composition of these flows painted a mixed picture.

Foreign Corporates emerged as the primary source of selling pressure, posting net outflows of $15.58 million, reflecting cautious sentiment among institutional foreign investors.

This was largely offset by a strong showing from Overseas Pakistanis, who contributed net inflows of $16.68 million.

Local participation during April was dominated by retail investors, with Individuals emerging as the most significant net buyers, injecting $59.54 million into the market, the largest contribution across all investor categories.

Mutual Funds and Companies also added to buying activity, with net purchases of $18.79 million and $16.45 million, respectively, while NBFCs recorded a minor net buy of $0.34 million.

On the sell side, Banks and DFIs were the most prominent net sellers, offloading $48.81 million, followed by Insurance Companies at $32.32 million and Other Organizations at $11.14 million.

Broker Proprietary Trading rounded out the sellers with net outflows of $3.98 million. On a net basis, the LIPI recorded a marginal net outflow of $1.14 million.

_20260430163912577_54b486.jpeg)

FY26 in Context

The FY26 narrative has three distinct chapters: a blazing start (Jul–Sep 2025, +31% over three months), a grinding winter consolidation (Oct 2025–Jan 2026), and a sharp correction followed by recovery (Feb–Apr 2026).

Despite the Feb–Mar

drawdown being the steepest two-month decline in recent memory, the KSE-100

still sits up 29.74% in PKR and 32.07% in USD for

the fiscal year to date, a return that comfortably outpaces most regional

peers and beats the FY25 performance of 60.15% on a trajectory-adjusted basis

when the remaining two months are considered.

Historically, April's performance places FY26 in respectable company. The market has now delivered positive FY returns in every year since FY19's 19.11% trough, with FY24's exceptional 89.24% and FY25's 60.15% setting an extraordinarily high base.

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,846.68 370.24M | -0.81% -1463.60 |

| ALLSHR | 108,777.96 842.70M | -0.57% -624.36 |

| KSE30 | 53,571.08 118.45M | -0.81% -434.78 |

| KMI30 | 253,007.72 126.35M | -1.06% -2717.47 |

| KMIALLSHR | 69,727.55 549.62M | -0.70% -488.73 |

| BKTi | 52,178.22 35.92M | -0.12% -62.01 |

| OGTi | 35,518.90 13.54M | -0.77% -274.36 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,775.00 | 64,610.00 63,260.00 | -345.00 -0.54% |

| BRENT CRUDE | 89.14 | 90.03 86.60 | 1.42 1.62% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -4.00 -3.65% |

| ROTTERDAM COAL MONTHLY | 122.00 | 122.00 122.00 | 0.75 0.62% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.40 | 84.61 81.27 | 1.27 1.55% |

| SUGAR #11 WORLD | 16.74 | 16.75 16.33 | 0.27 1.64% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|