Oil to see triple deficit in 2HCY22: Morgan Stanley

By MG News | January 11, 2022 at 05:30 PM GMT+05:00

January 11, 2022 (MLN): The oil market is likely to witness another year in disruption as it could see simultaneously low inventories, low spare capacity and low investment levels by 2HCY22 and the price to reach at $90 per bbl brent forecast for 3Q, a recently published report by Morgan Stanley noted.

During the last year, the oil prices rose around 50% last year, making 2021 one of the strongest years in the oil market in recent history. However, it is expected that the upward stick will continue which could create enough room for the oil market to witness triple-deficit.

With regards to low investment, the report noted that of all categories of spending, exploration remains particularly hard-hit. In 2021, the number of exploration wells completed dropped another 27%, and global discoveries fell to a 20+ year low.

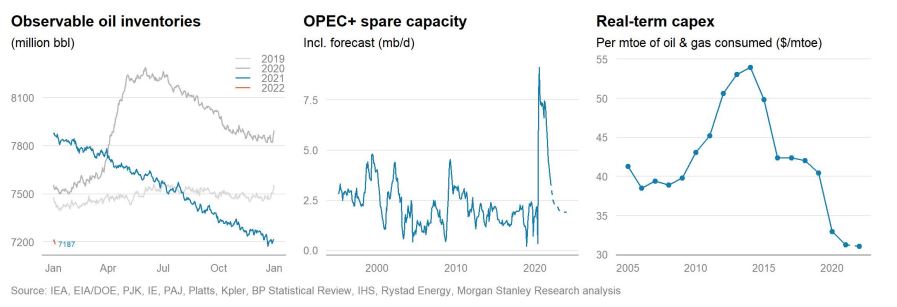

Field development fared better, but only marginally. Oil companies approved new investments for just 12.6bn barrel of future production - outside 2020, also 15+ year low.

“Development capex increased around 5% in nominal terms, but taking into account cost inflation, now running +11% y/y capex in real terms per unit of oil & gas consumed fell another 5% last year to a new 15+ year low,” it added.

In nominal terms, development capex is likely to increase around 8-9% in 2022, based on company guidance and estimates from consultants. However, if even inflation were to slow sharply from here, costs are still likely to be around 5% higher in 2022 on average, it added.

With combined oil & gas demand likely to increase by 3-4% as well, we estimate, real-term capex per unit of consumption is likely to stay broadly flat at the 2021 level, which is around 20% below the 2006-08 level, before the industry's capex boom of the early 2010s.

On the capacity front, the report said that spare capacity is likely to fall below 2 mb per day by second half in 2022. OPEC+ spare capacity has already fallen from 6.6 mb per day at the start of 2021, to almost 3.4 mb per day by November.

“It is expected OPEC+ (excl. Iran) production to increase by 250 kb per day per month in 1H and largely flat line in second half. That is far slower than the 400 kb per day monthly quota increase that OPEC+ has agreed on, but still would lead spare capacity to drop below 2 mb per day in second half, leaving a relatively small buffer,” it noted.

While inventories fell by 690mn bbl in 2021 with a rate of decline of 1.9 mbd, and are now at a 5+ year low. However, with a constructive demand forecast and relatively cautious expectations for OPEC+ supply, inventories to end 2022 lower still, the report highlighted.

Thus, Morgan Stanley forecasted the oil prices to reach $90 per bbl by third quarter of 2022.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 130,344.03 345.79M |

1.67% 2144.61 |

| ALLSHR | 81,023.99 1,021.87M |

1.55% 1236.37 |

| KSE30 | 39,908.26 141.62M |

2.05% 803.27 |

| KMI30 | 189,535.00 150.29M |

1.40% 2619.39 |

| KMIALLSHR | 54,783.66 508.76M |

1.07% 581.78 |

| BKTi | 34,940.73 55.86M |

4.37% 1464.05 |

| OGTi | 28,296.06 16.02M |

1.19% 333.47 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 109,320.00 | 110,105.00 109,265.00 |

-965.00 -0.88% |

| BRENT CRUDE | 68.50 | 69.00 68.48 |

-0.61 -0.88% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

0.75 0.78% |

| ROTTERDAM COAL MONTHLY | 109.20 | 110.00 108.25 |

1.70 1.58% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.87 | 67.50 66.83 |

-0.58 -0.86% |

| SUGAR #11 WORLD | 15.56 | 15.97 15.44 |

-0.14 -0.89% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|