MPS Preview: Deteriorating macros cueing a sharp hike

MG News | May 21, 2022 at 07:17 PM GMT+05:00

May 20, 2022 (MLN): The State Bank of Pakistan (SBP) is scheduled to convene on May 23, 2022, wherein it is likely to increase the policy rate by 100-150 bps in the upcoming monetary policy statement.

The prospects of tighter monetary policy arise primarily from the movement in both primary and secondary market yields for government securities.

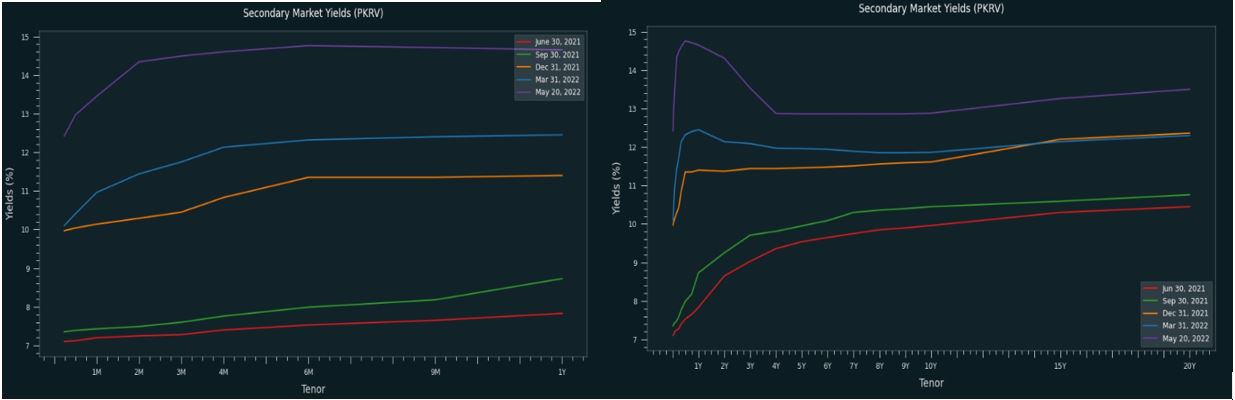

To infer the market expectations for monetary policy, the foremost thing to look at is the shape of the yield curve. On the PKRV front, it has been witnessed that since the last MPC meeting in April’22, yields have increased within the range of 203 bps to 332 bps as of May 19, 2022, for tenors 1M to 12M. For longer tenors 2Yrs to 20Yrs, the yields have soared within the range of 35 bps to 168 bps, hinting at the market’s expectations of another hike in the policy rate.

Further, as per the latest auction of T-bills on May 19, 2022, the cut-off yields for 3M, 6M and 12M have swelled by 170 bps, 145 bps, and 145 bps to currently stand at 14.5%, 14.7%, and 14.75% respectively, well above the prevailing policy rate of 12.25%. Moreover, in the recent T-bills auction, the majority of the participation was witnessed in 3M papers which indicates that investors are preferring to invest in the shortest tenor in anticipation of a rate hike.

On the KIBOR side, interbank rates since the last MPS have drastically increased within the range of 165 bps to 228 bps respectively for 1M, 3M, 6M, 9M and 1Y tenors as of May 19, 2022. At present, the real interest rate is at -1.15% whereas the gap between the interest rate and 6M KIBOR is at -2.59%, leaving ample room for further rate hikes.

The expectations of a sharp hike in policy rate further stem from a deteriorating outlook for inflation, rapidly slipping PKR, rising fiscal deficit amid huge petrol/diesel subsidy, dwindling FX reserves, and a crucial round of talks with the International Monetary Fund (IMF) which are currently underway, may push for further tightening.

Headline inflation which remained in double digits since Nov'21 is getting uncontrollable now, as it hit almost two years high of 13.4% in April’22, with pressure mainly coming from higher food and energy-related commodity prices such as oil, RLNG, and coal due to the Russia-Ukraine war.

As a result of continuous rise in energy-related commodity and food prices, the average food basket increased by 18% YoY, whereas energy prices were up by 38% YoY, combined with spillover effects, taking average inflation for 10MFY22 at 11% compared to 8.9% reported in FY21.

On the external front, the turbulence continues as the current account deficit increased massively to $13.8bn during 10MFY22 against $543mn during 10MFY21. This is primarily due to the huge import bills fueled by higher international commodity prices and strong aggregate demand owing to a recovery in GDP growth increasing the deficit. Meanwhile, to curb the massive deficit, the government on Thursday decided to impose a ban on the import of non-essential luxury items under the Comprehensive Economic Plan.

Similarly, on the fiscal side, the unbudgeted fuel subsidies and rising debt financing costs are squeezing the fiscal space of the government. In the 9MFY22, despite record tax collections, budget deficit stood at Rs2.56bn vs. Rs1.65bn seen in the same period last year. The said increase was mainly on account of Rs371bn increase in federal government subsidies, Rs244bn (66%) reduction in petroleum levy on retail fuels and Rs146bn increase in markup payments.

Further, since the last MPS in April, SBP’s FX reserves have plunged by $686mn or 7% to $10.2bn equivalent to 1.5 months of the import bill, mainly due to external debt repayments and settlement on a mining project. The dwindling FX reserves have put Pakistan’s currency under immense pressure, resulting in a sharp dip of Rs200 per dollar in the interbank market, depreciating by Rs11.82 since April 7, 2022.

Market participants expecting policy rate to increase to 13.25%

Based on the above scenarios, market consensus also seems to be pointing towards a sharp hike in policy rate as 9 out of 14 brokerage houses in a survey conducted by MG, expect SBP to increase the interest rate by 100 bps while 5 brokerage firms are expecting a hike in the range of 100-150 bps.

|

Policy Rate Projections for May'22 |

||

|---|---|---|

|

Brokerage House |

Expectations |

|

|

KASB Securities |

hike of 100-150 bps |

|

|

Abbasi and Company Pvt Ltd |

hike of 100-150 bps |

|

|

Insight Securities |

hike of 100-150 bps |

|

|

AKD Securities |

hike of 150 bps |

|

|

TSBL |

hike of 125 bps |

|

|

Optimus Capital |

hike of 100 bps |

|

|

Taurus Securities |

hike of 100 bps |

|

|

Arif Habib Limited |

hike of 100 bps |

|

|

WE Financial |

hike of 100 bps |

|

|

Sherman Securities |

hike of 100 bps |

|

|

JS Global |

hike of 100 bps |

|

|

Topline Securities |

hike of 100 bps |

|

|

Spectrum Securities |

hike of 100 bps |

|

|

Pearl Research |

hike of 100 bps |

|

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 178,262.34 385.16M | 4.23% 7241.13 |

| ALLSHR | 107,837.44 1,028.26M | 3.85% 4001.05 |

| KSE30 | 53,347.67 160.21M | 4.70% 2395.68 |

| KMI30 | 251,510.37 142.71M | 4.52% 10876.50 |

| KMIALLSHR | 69,173.86 484.44M | 3.91% 2601.11 |

| BKTi | 51,064.73 51.74M | 4.91% 2391.50 |

| OGTi | 35,248.42 10.48M | 4.59% 1546.17 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 65,550.00 | 66,075.00 63,875.00 | 1335.00 2.08% |

| BRENT CRUDE | 90.51 | 93.60 87.55 | -6.27 -6.48% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 120.00 | 120.00 120.00 | -0.25 -0.21% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.86 | 86.20 82.12 | -5.45 -6.10% |

| SUGAR #11 WORLD | 14.60 | 14.75 14.54 | -0.17 -1.15% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|