July's heatwave doused by strong macros

Nilam Bano | August 01, 2024 at 12:31 PM GMT+05:00

August 01, 2024 (MLN): July has been sweltering for the masses, but it brought a fresh breeze to Pakistan's economic landscape as the first month of FY25 was a parade of positive news. The economy hummed with optimism from almost all corners.

From robust data points issued by the Central Bank of Pakistan to favourable ratings from international agencies, the stars seemed to align.

The cherry on top was Pakistan securing a 37-month IMF Extended Fund Facility (EFF) program worth $7 billion.

The program aims to capitalize on the hard-won macroeconomic stability achieved over the past year by furthering efforts to strengthen public finances, reduce inflation, rebuild external buffers and remove economic distortions to spur private sector-led growth.

This lifeline, along with cooling inflation, gave the State Bank of Pakistan (SBP) the wiggle room to start considering a drop in interest rates, encouraging a bullish run in the equity market.

Foreign investors' interest rekindled in Pakistan's stock market on the IMF program, alongside rollovers from China and the UAE as Foreign Portfolio Investment (FIPI) saw a noticeable uptick in July.

In July alone, the FIPI saw a whopping upsurge of 13x MoM to $28.83m compared to $1.83m in June 2024. On a yearly basis, it witnessed an increase of 31.3% compared to $18.15m in July 2023.

.png)

Albeit unpopular bold decisions of authorities in the FY25 budget were crucial in securing the much-needed IMF program, restoring the confidence of friendly nations and investors alike.

As a result, investors stepped up to the plate to ride the waves of this new economic chapter.

Let’s have a look at the macros announced in July:

On cooling the State Bank of Pakistan (SBP) lowered its key policy rate by another 100 basis points to 19.5% on Monday, this week in line with the market expectations. The reduction was the second in a row, bringing the total decrease since June 2024 to 250bps.

This decision was attributed to the improved inflation in June 2024 along with SBP's FX reserves that have surged to over $9bn despite debt repayments, a narrower current account deficit, and IMF deal.

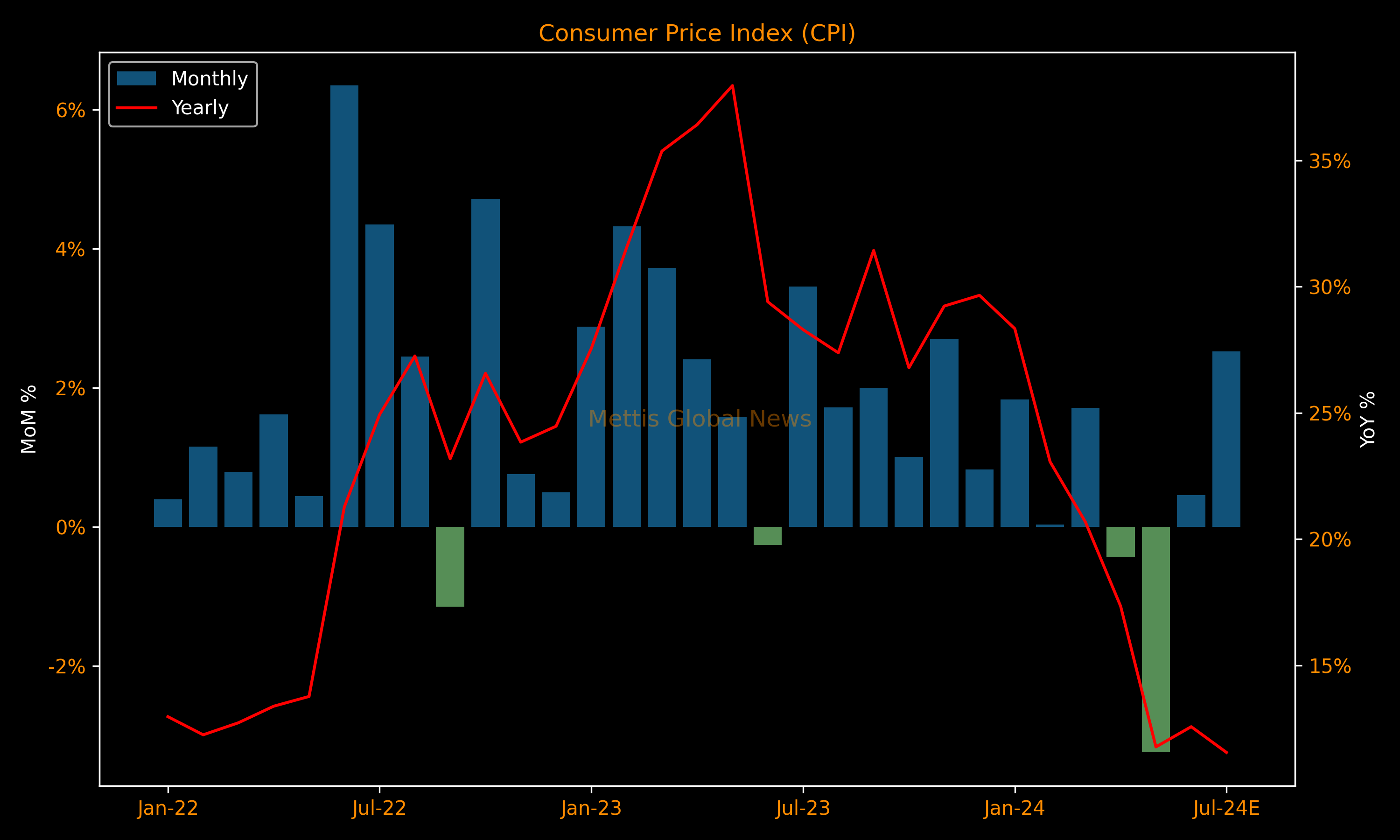

On the inflation side, CPI is expected to remain on the lower side in July despite a significant jump in monthly prices. According to our estimates, inflation is expected to fall to 11.6% in July 2024, compared to 12.6% YoY in the last month and 28.3% YoY in July 2023.

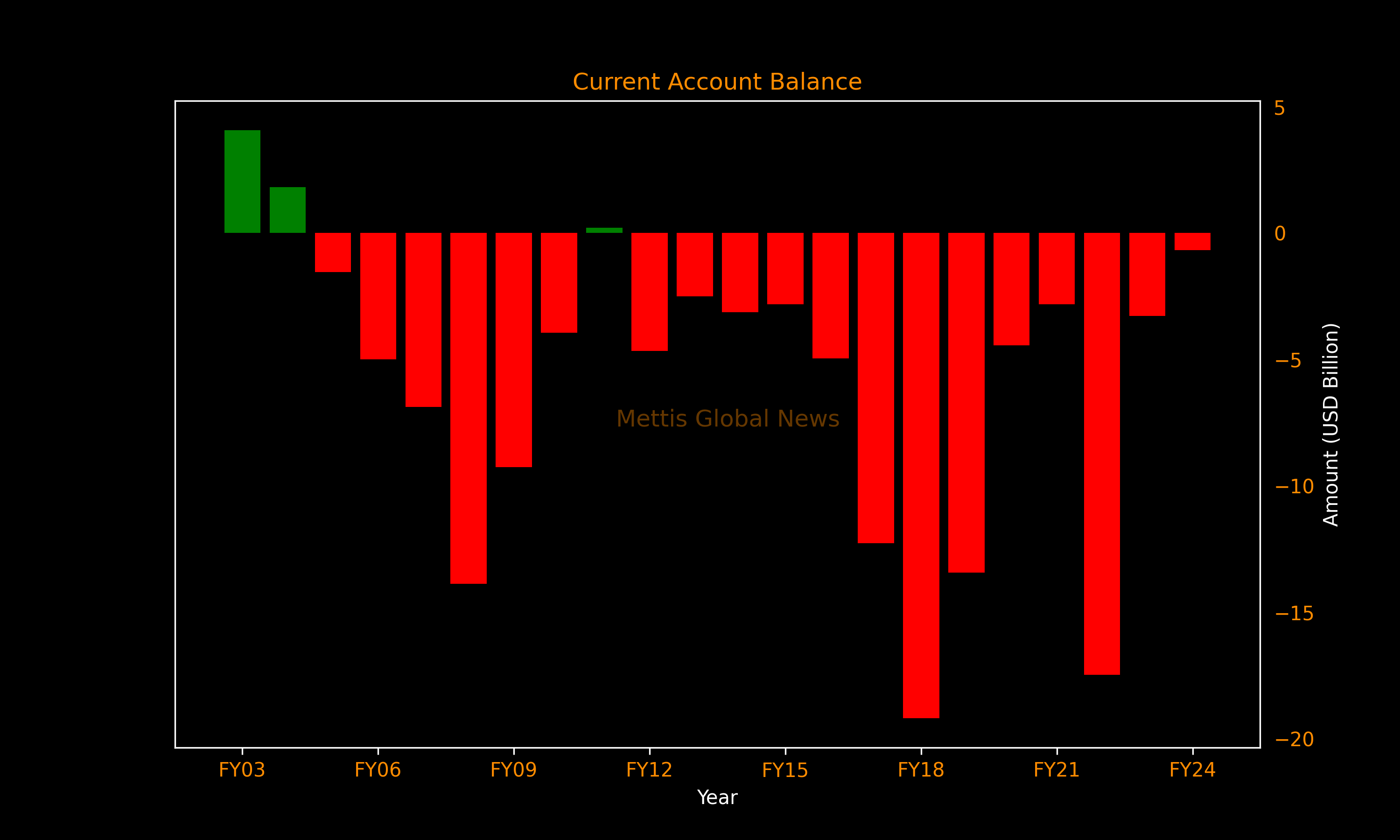

The current account deficit narrowed to $681 million, or 0.2% of GDP in FY24. This is a far cry from the $3.27 billion deficit the previous year and the average gap of $8.3bn over the past five years.

The last time the deficit was this low was in FY11.

This narrowing trade deficit was attributed to strong exports of food and high value-added (HVA) textiles, along with a significant drop in import payments.

Moreover, improved domestic agricultural output, moderate domestic demand, and favourable global commodity prices played a noteworthy role.

Rumours of import restrictions by the State Bank of Pakistan (SBP) were put aside by major importers and bank officials, who denied any significant controls.

The SBP Governor also confirmed this month that there are no restrictions on imports.

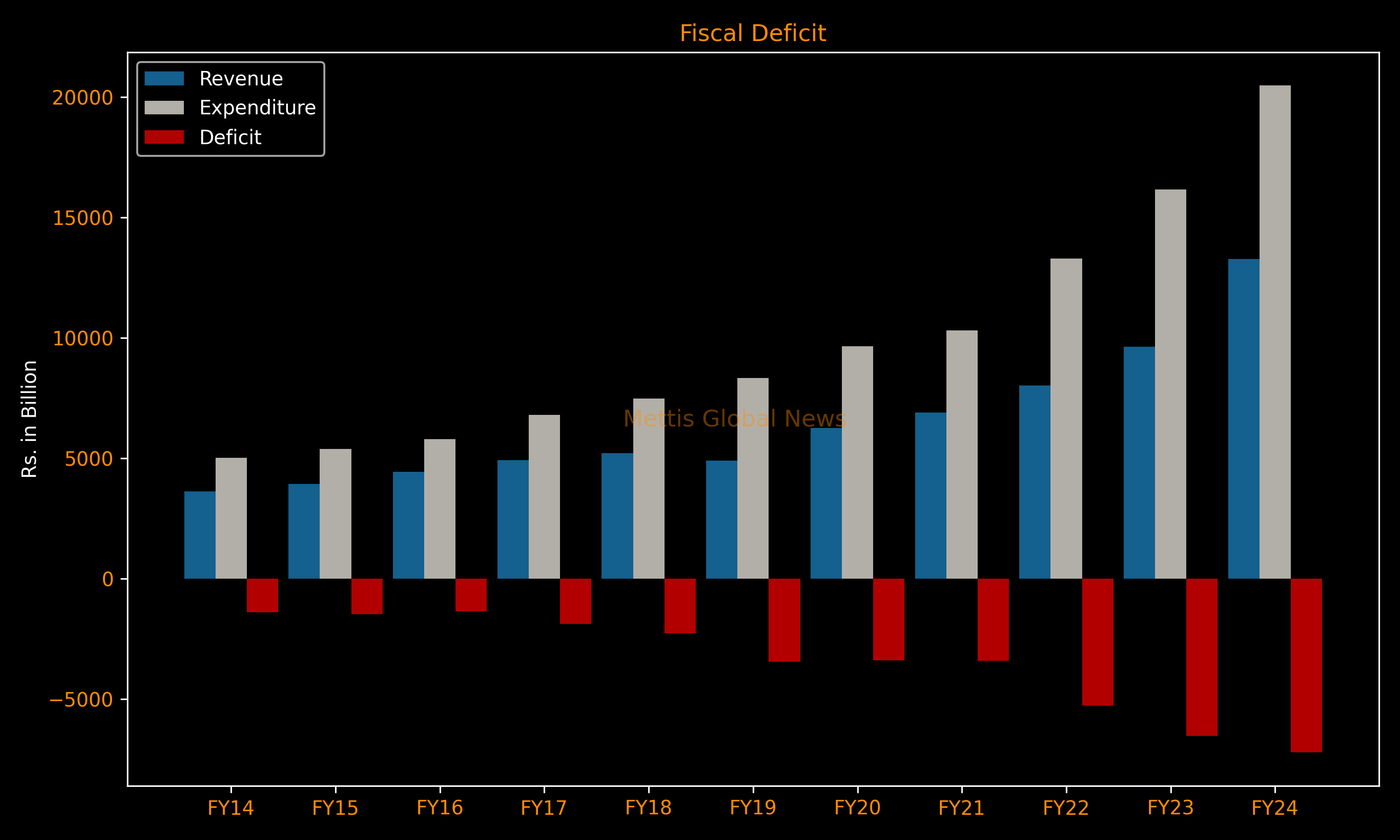

On the fiscal side, the government managed to keep its financial house for the first time in nearly two decades, reporting a primary surplus in FY24 worth Rs952.92bn, or 0.9% of GDP.

This is the first such surplus since FY07. The fiscal deficit narrowed to 6.8% of GDP in FY24, down from 7.7% the previous year.

Pakistan saw a significant jump in FDI, increasing by 16.9% YoY to $1.9bn in FY24, compared to $1.63bn in the previous year.

In June 2024 alone, foreign inflows witnessed an uptick of 37.8% YoY to $168.75m, up from $122.42m in June 2023.

The country saw a decent surge in workers’ remittances by 10.68% to $30.25bn in FY24, compared to $27.33bn in FY23.

In June alone, remittances jumped by 44.4% year-on-year to $3.16bn, up from $2.19bn in June 2023.

Along with macros, the ratings from international agencies have also strengthen the confidence.

S&P Global Ratings affirmed Pakistan's long-term sovereign credit rating at 'CCC+' and short-term rating at 'C', maintaining a stable outlook.

This decision reflects a balance between the challenges posed by Pakistan's external liquidity and fiscal performance and the expected continued support from multilateral and bilateral partners over the next 12 months.

Meanwhile, Fitch Ratings upgraded Pakistan's Long-Term Foreign-Currency Issuer Default Rating (IDR) to 'CCC+' from 'CCC'.

It is important to note that Fitch typically does not assign outlooks to sovereigns rated 'CCC+' or below, but the upgrade reflects greater confidence in the availability of external funding, particularly in light of Pakistan's staff-level agreement (SLA) with the IMF.

What does the future hold for us?

During the reviewed month, a mixed bag of economic projections came forward.

The central bank expected GDP growth to range between 2.5% and 3.5%, foreign reserves to reach $13bn, and a current account deficit of 0-1.0% of GDP. The inflation target is set at 11.5-13.5%.

SBP Governor Jameel Ahmed, during the post-MPC Analyst Briefing, highlighted promising projections, including expected repayments of $26.2 billion, with $16.3bn set for rollover, leaving a net repayable amount of $10bn.

$1.1bn has already been repaid as of July 2024 with $9bn remaining over the next 11 months.

Meanwhile, S&P Global Ratings forecasted a significant drop in Pakistan's inflation over the next three years, although still above the central bank's target range of 5-7%.

The agency projected inflation to fall to 12.7% in FY24-25, down from last year's alarming 23.4%. The inflation rate is projected to ease further to 9% in both FY26 and FY27.

On the GDP front, S&P predicted Pakistan's economy will grow at a subdued rate of 3.5% in FY24-25, a slight improvement from 2.4% in the previous year.

This is in line with the government's target of 3.6% and the State Bank of Pakistan's (SBP) forecast of 2.5-3.5%.

Moreover, the Asian Development Bank's July 2024 Outlook (ADO) forecasted that Pakistan's public debt is likely to decline by 7 percentage points to 70% of GDP in FY24-25.

However, one should not forget that Pakistan's economy is often swayed by political tides, the road ahead might have its bumps but the macroeconomic outlook for the year remains promising.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,846.68 370.24M | -0.81% -1463.60 |

| ALLSHR | 108,777.96 842.70M | -0.57% -624.36 |

| KSE30 | 53,571.08 118.45M | -0.81% -434.78 |

| KMI30 | 253,007.72 126.35M | -1.06% -2717.47 |

| KMIALLSHR | 69,727.55 549.62M | -0.70% -488.73 |

| BKTi | 52,178.22 35.92M | -0.12% -62.01 |

| OGTi | 35,518.90 13.54M | -0.77% -274.36 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,740.00 | 64,610.00 63,260.00 | -380.00 -0.59% |

| BRENT CRUDE | 89.11 | 90.03 86.60 | 1.39 1.58% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -4.00 -3.65% |

| ROTTERDAM COAL MONTHLY | 122.00 | 122.00 122.00 | 0.75 0.62% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.39 | 84.61 81.27 | 1.26 1.53% |

| SUGAR #11 WORLD | 16.74 | 16.75 16.33 | 0.27 1.64% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|