Weekly Market Roundup

_20260711124603464_8ff65f.jpeg?width=950&height=450&format=Webp)

MG News | July 11, 2026 at 05:49 PM GMT+05:00

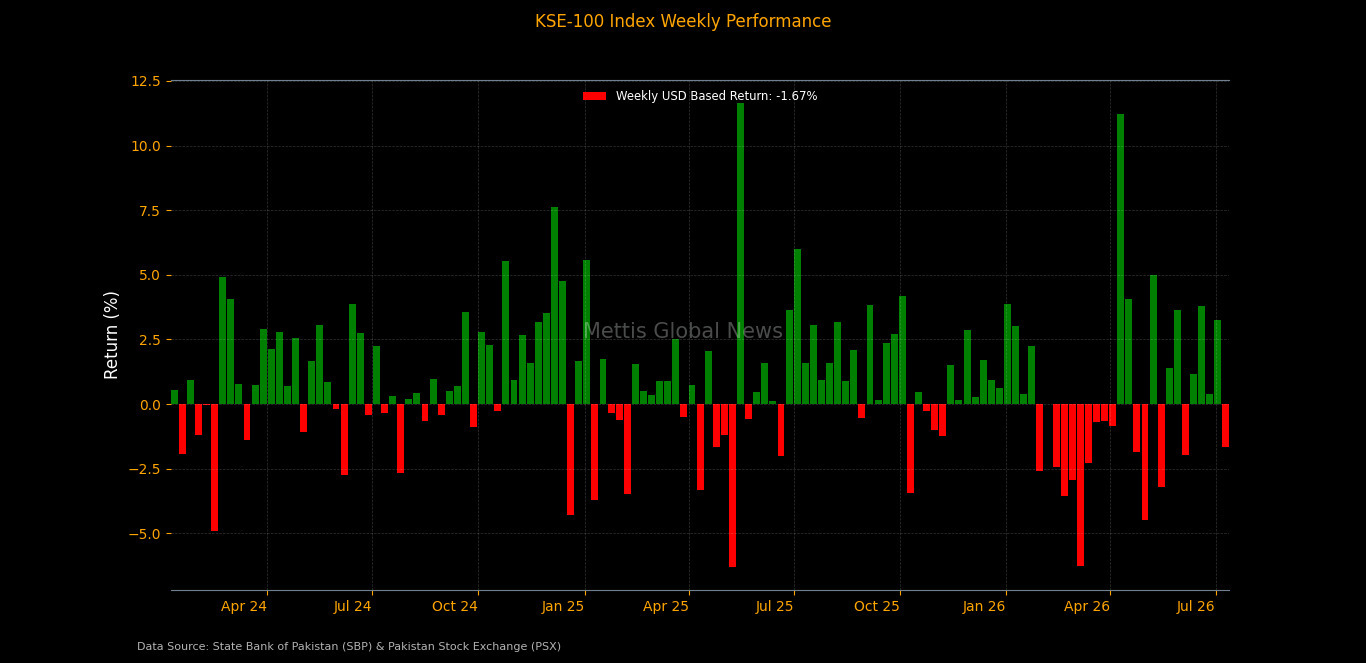

July 11, 2026 (MLN): The benchmark KSE-100 Index closed the week ended July 10, 2026 at 182,241.78 points, losing 3,130.43 points, or 1.69%, on a week-on-week basis from 185,372.21 points recorded on July 03, 2026.

Investor sentiment remained under pressure during the week

as escalating geopolitical tensions in the Middle East and fears of potential

disruptions to global oil supplies dampened risk appetite.

Concerns that higher energy prices could fuel inflation and

weigh on the global economic outlook prompted investors to adopt a cautious

stance, while selective value buying towards the end of the week helped the

benchmark index recover part of its losses.

Market Capitalization

The Pakistan Stock Exchange's market capitalization declined

by Rs89.70bn during the week, falling from Rs5.301tr on July

03 to Rs5.212tr on July 10.

In dollar terms, market capitalization decreased from $19.06bn

to $18.74bn, registering a decline of approximately $318.00m over

the week._20260711124554612_1a88d2.jpeg)

The market's USD-adjusted return stood at -1.67%,

compared with a positive 3.26% in the previous week, reflecting the

benchmark's decline after accounting for currency movements.

On the macroeconomic front, The SBP's latest liquidity

report projects $24.74bn in

foreign currency outflows within a year, with the largest repayments

due in the three-month to one-year period, against official reserves of $27.86bn.

Pakistan received $3.47bn in workers'

remittances in June 2026, down 18.3% month-on-month but up 2%

year-on-year, taking FY26 inflows to a record $41.58bn.

SBP raised Rs2.07tr through the MTB

auction, with cut-off yields declining across all tenors by

31–40bps, signaling easing short-term borrowing costs.

Pakistan's central

government debt rose 7.76% YoY to Rs81.95tr in May 2026, driven by

higher domestic and external borrowing to finance the fiscal deficit.

National

Savings Schemes mobilized Rs18.4bn in net savings in May 2026, down from

Rs23.9bn in April, with cumulative FY26 inflows reaching Rs269bn.

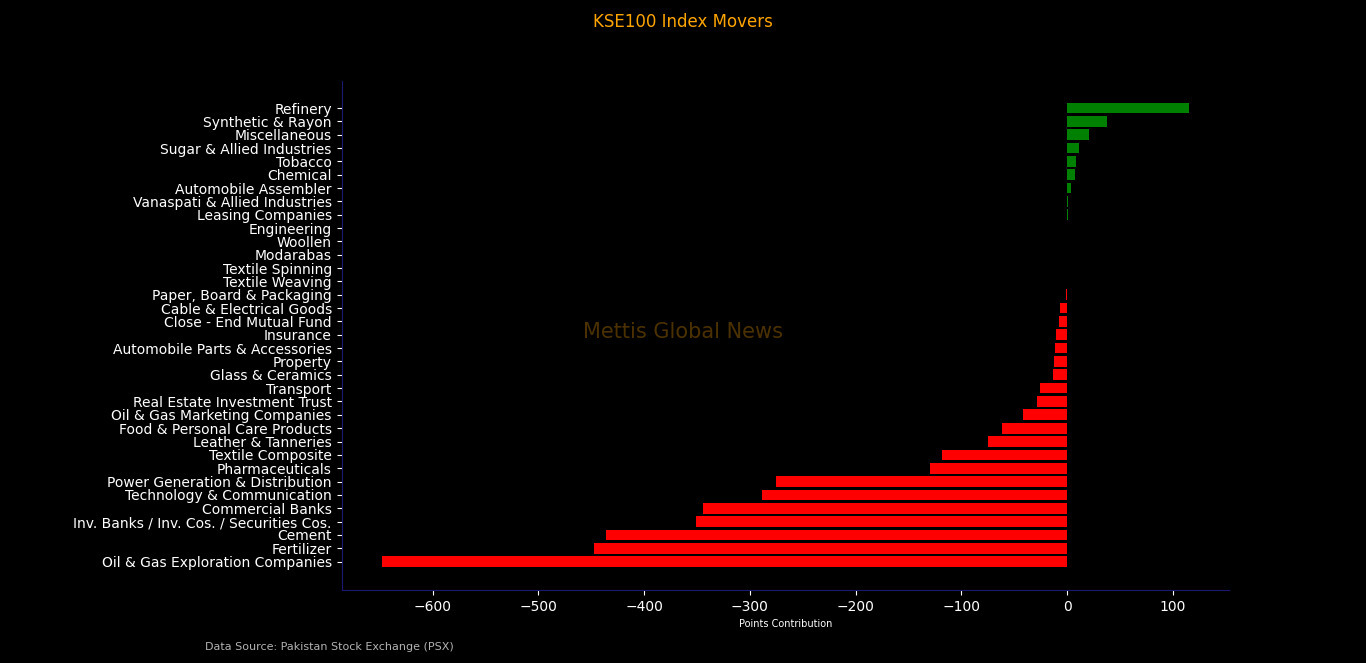

Index Movers

Sector-wise performance remained broadly negative during the

week, with Oil & Gas Exploration Companies exerting the largest drag

on the KSE-100 Index by 648.16 points, followed by Fertilizer (447.95

points),

Cement (436.01 points), Investment

Banks/Investment Companies/Securities Companies (351.24 points), Commercial

Banks (344.47 points), Technology & Communication (288.34 points),

Power Generation & Distribution (275.68 points), Pharmaceuticals

(129.87 points), Textile Composite (117.92 points), Leather &

Tanneries (75.22 points), Food & Personal Care Products (61.91

points),

Oil & Gas Marketing Companies (41.76 points), Real

Estate Investment Trust (28.55 points), and Transport (25.29 points).

On the positive side, Refinery contributed 115.39

points to the index, followed by Synthetic & Rayon (38.20 points),

Miscellaneous (20.64 points), Sugar & Allied Industries (11.02

points), Tobacco (8.32 points), Chemical (7.61 points) and Automobile

Assembler (3.97 points).

Among individual stocks, FFC emerged as the largest

contributor to the index, adding 410.15 points, followed by ENGROH

(378.98 points), PPL (284.66 points), OGDC (254.92 points),

HUBC (223.16 points), UBL (205.65 points), SYS

(182.39 points), LUCK (177.35 points), BAFL (149.40 points)

and MCB (141.26 points).

Other notable positive contributors included MARI (93.54

points), FCCL (83.45 points), AKBL (83.16 points), SRVI

(75.22 points), SAZEW (63.35 points), PTC (62.65 points), SNGP

(56.51 points), MLCF (48.30 points), NML (41.83 points) and ABOT

(38.97 points).

Among the major laggards were HBL (161.47 points), GHNI

(90.64 points), CNERGY (65.79 points), ATRL (49.60 points), IBFL

(38.20 points), SHFA (34.37 points), NBP (31.57 points), BAHL

(30.61 points), PSO (30.12 points) and PSX (27.75 points)._20260711124529874_92b68e.jpeg)

FIPI/LIPI

Foreign investors turned net buyers during the week,

recording net equity purchases of Rs2.37bn ($8.53m).

The buying was primarily driven by Foreign Corporates,

which accumulated equities worth Rs2.29bn ($8.24m). Overseas

Pakistanis also remained net buyers with Rs80.58m ($289,841) worth

of equity purchases, while Foreign Individuals posted modest net buying

of Rs382,794 ($1,377).

On the local side, Individuals emerged as the largest

buyers, with net equity purchases of Rs4.03bn ($14.51m).

Banks/DFIs also remained strong buyers with Rs2.77bn

($9.97m) worth of net purchases, followed by Insurance Companies

with Rs535.76m ($1.93m), Broker Proprietary Trading with Rs115.67m

($416,085) and NBFCs with Rs112.85m ($405,944).

The largest sellers were Companies, which offloaded

equities worth Rs5.80bn ($20.87m).

Mutual Funds recorded net selling of Rs3.15bn

($11.35m), followed by Other Organizations with Rs987.03m

($3.55m)._20260711124538709_68acc8.jpeg)

Copyright Mettis Link News

Related News

.png?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 176,094.12 210.43M | 0.31% 546.13 |

| ALLSHR | 106,530.89 879.03M | 0.30% 313.70 |

| KSE30 | 52,480.22 54.21M | 0.01% 4.71 |

| KMI30 | 247,198.06 71.10M | 0.26% 628.83 |

| KMIALLSHR | 68,178.54 320.54M | 0.35% 237.08 |

| BKTi | 50,319.17 20.32M | -0.21% -103.75 |

| OGTi | 34,316.47 3.14M | 0.13% 43.33 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,220.00 | 63,220.00 63,080.00 | 90.00 0.14% |

| BRENT CRUDE | 91.04 | 91.36 84.62 | 4.16 4.79% |

| RICHARDS BAY COAL MONTHLY | 107.75 | 0.00 0.00 | -0.25 -0.23% |

| ROTTERDAM COAL MONTHLY | 121.60 | 121.65 121.60 | 0.95 0.79% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 86.80 | 86.87 81.06 | 3.21 3.84% |

| SUGAR #11 WORLD | 14.65 | 14.78 14.38 | 0.22 1.52% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|