Weekly Market Roundup

_20260320170657967_803b17.jpeg?width=950&height=450&format=Webp)

MG News | March 20, 2026 at 10:12 PM GMT+05:00

March 20, 2026 (MLN): Pakistan’s equity market

remained under pressure during the outgoing week, as the benchmark KSE-100

Index closed at 152,740.38, compared to 153,866.17 recorded on March 13, 2026.

The index shed 1,125.79 points over the week, translating

into a decline of 0.73% week-on-week (WoW).

Investor sentiment weakened as global oil and gas prices

surged, driven by fresh attacks on critical energy infrastructure in the Middle

East, pushing crude prices sharply higher to around $116 per barrel. The spike

in energy prices prompted cautious trading and broad-based selling across key

sectors.

Market Capitalization

Market capitalization also declined in line with the

benchmark index. The total listed market cap fell to Rs4.43 trillion on March 19,

2026, compared to Rs4.51tr recorded on March 13, 2026, marking a contraction of

Rs79.34bn or 1.76% WoW.

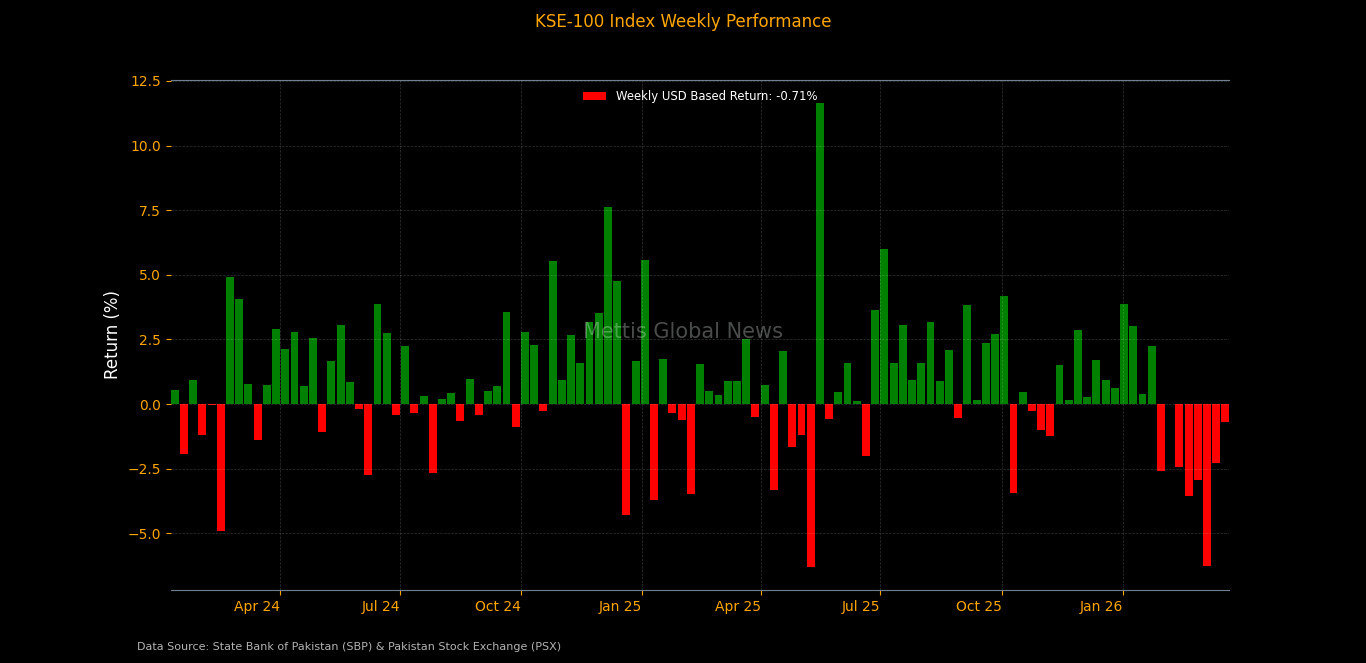

In dollar terms, total market capitalization declined by

$280.61m, reaching $15.87bn compared to $16.15bn in the previous week._20260320170648222_333881.jpeg)

Meanwhile, dollar-adjusted returns stood at negative 0.71%,

compared to negative 2.27% in the prior week, suggesting that the pace of

decline slowed relative to the previous week’s sharper drop.

On the macroeconomic front, Automobile financing, as per State Bank of Pakistan data, rose to Rs336.61bn in February 2026, up 2.62% MoM and 35.28% YoY.

While total consumer financing

increased 19.46% YoY to Rs1.04tr with a 1.8% monthly gain; private sector

credit also grew 13.58% YoY to Rs10.61tr, driven mainly by gains in manufacturing,

alongside moderate increases in housing and personal loans.

Pakistan’s

LSM sector showed strong growth in January 2026, with output rising 10.54%

YoY and 12.08% MoM, taking cumulative FY26 growth to 5.75%.

Pakistan’s

Real Effective Exchange Rate (REER) fell 0.74% to 102.54 in February 2026,

while the Nominal Effective Exchange Rate (NEER) declined 0.50%, according to

the State Bank of Pakistan.

Despite the monthly drop, REER edged up 0.28% YoY, whereas

NEER fell 3.72% annually.

Pakistan’s FDI rose to $213.5m

in February 2026 from $132.7m last year, driven by higher inflows,

according to the State Bank of Pakistan. However, cumulative FDI in 8MFY26

declined to $1.19bn compared to $1.79bn last year.

Pakistan posted a current account surplus

of $427m in February, driven by steady remittances, though the 8MFY26

cumulative current account shows a $700 million deficit amid higher imports and

a widening trade gap.

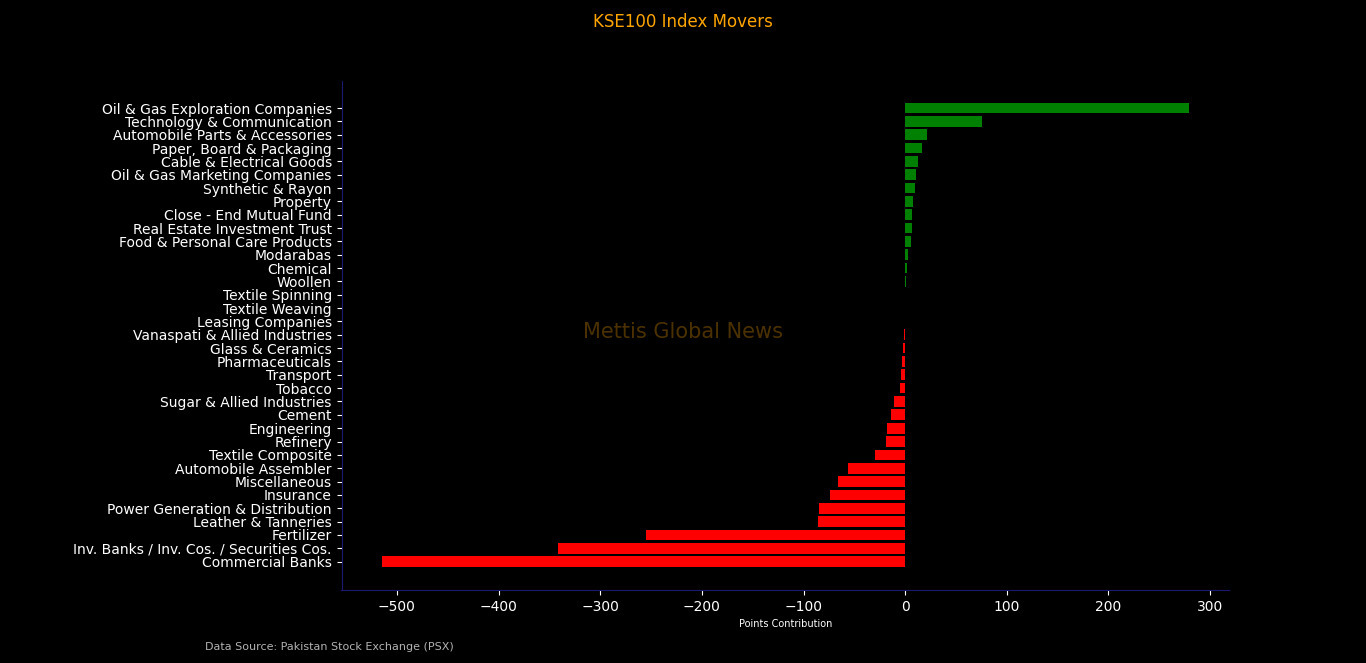

Index Movers

Sector-wise performance remained largely negative,

reflecting continued pressure across major segments of the market.

Commercial banks emerged as the largest drag on the

benchmark, wiping out 514.86 index points, followed by investment banks and

securities companies (-341.42 points) and fertilizer (-254.92 points).

Power generation and distribution (-84.97 points), insurance

(-73.92 points), miscellaneous (-66.15 points), and automobile assemblers

(-56.47 points) also contributed to the downside.

Other notable laggards included textile composite,

refineries, engineering, cement, and pharmaceuticals, highlighting the

broad-based nature of the decline.

On the positive side, oil and gas exploration companies

provided the largest support to the index, adding 279.32 points.

Technology and communication contributed 75.52 points,

followed by automobile parts (21.08 points), paper and packaging (16.13

points), and cable and electrical goods (12.69 points).

Additional support came from oil marketing companies,

synthetic and rayon, property, REITs, and food and personal care sectors,

though gains remained limited compared to the broader losses.

At the company level, select stocks managed to lend support

to the index.

Among the gainers, MCB added 196.95 points, followed by UBL

(162.87 points) and SYS (122.19 points).

Other notable positive contributors included PPL (100.17

points), OGDC (79.24 points), POL (70.78 points), ABOT (61.27 points), and MLCF

(48.74 points).

Additional support came from KOHC, AKBL, PSO, MARI, and

THALL.

Despite these gains, the benchmark remained under pressure

due to heavy losses in several large-cap stocks.

NBP emerged as the largest drag on the index, wiping out

470.92 points, followed by ENGROH (-301.97 points) and HBL (-289.57 points).

Other major negative contributors included FFC (-203.80

points), HUBC (-91.99 points), SRVI (-85.62 points), AICL (-73.92 points), and

LUCK (-59.13 points).

Further pressure came from EFERT, BAHL, HMB, DGKC, and BAFL,

reflecting continued selling in index-heavy sectors, particularly banking and

fertilizer._20260320170620808_60a09d.jpeg)

FIPI / LIPI

Foreign investment flows continued to weigh on the market

during the week.

Under Foreign Portfolio Investment (FIPI), foreign investors

remained net sellers with an outflow of $9.94m.

The majority of the selling came from foreign corporates,

which offloaded $10.82m worth of equities.

Meanwhile, overseas Pakistanis provided buying support of

$0.88m, while foreign individuals remained largely neutral.

On the other hand, local investors absorbed the entire

foreign outflow, resulting in a matching net inflow of $9.94m under Local

Portfolio Investment (LIPI).

Among local participants, banks and DFIs emerged as the

largest buyers with net purchases of $9.47m, followed by individuals ($3.65m)

and companies ($1.95m).

Insurance companies and other organizations also recorded

modest inflows.

Meanwhile, mutual funds recorded the largest selling with an

outflow of $4.67m, followed by broker proprietary trading desks ($1.20m), while

NBFCs remained marginal buyers._20260320170628985_cb7892.jpeg)

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

_20260711124603464_8ff65f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 180,440.08 313.04M | -0.99% -1801.69 |

| ALLSHR | 109,591.89 713.12M | -0.90% -991.78 |

| KSE30 | 53,872.38 71.56M | -1.03% -559.33 |

| KMI30 | 254,139.42 90.17M | -1.08% -2774.79 |

| KMIALLSHR | 70,319.19 465.39M | -1.02% -722.11 |

| BKTi | 51,238.64 14.76M | -0.92% -474.12 |

| OGTi | 36,269.50 6.16M | -1.06% -390.08 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,205.00 | 64,680.00 62,605.00 | -880.00 -1.37% |

| BRENT CRUDE | 77.44 | 79.80 77.38 | 1.43 1.88% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 72.73 | 75.08 72.67 | 1.32 1.85% |

| SUGAR #11 WORLD | 14.68 | 14.98 14.65 | -0.20 -1.34% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|