Weekly Market Roundup

MG News | November 30, 2025 at 08:49 AM GMT+05:00

November 30, 2025 (MLN): The Pakistan Stock Exchange wrapped up the week with a strong rally, as the KSE-100 Index closed at 166,677.7 points, rising 2.82% from last week’s level of 162,102.92 points.

Despite two bearish sessions, the bulls dominated the week with three consecutive green closes, strengthening the upward trend driven by improved macro indicators and upbeat institutional flows.

_20251130025658297_ddcd45.jpeg)

The currency market also offered mild support. The PKR appreciated by 0.04% against the USD, closing at 280.5231, up from 280.6229 last week.

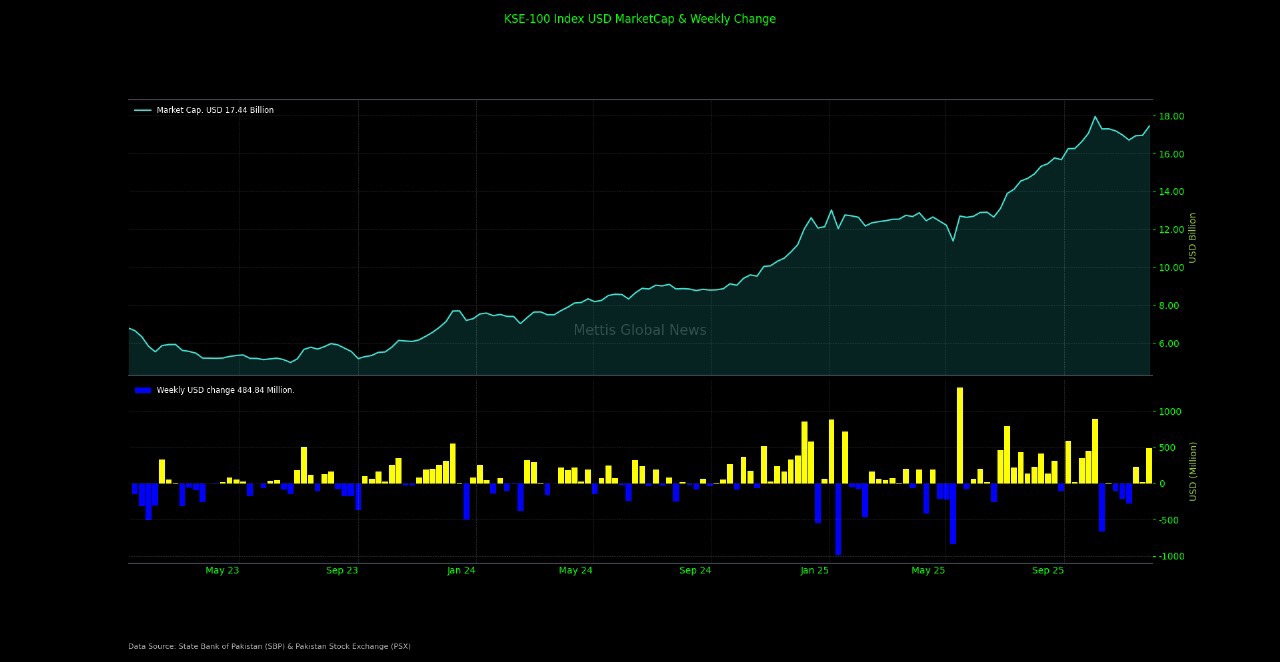

In line with the market’s positive tone, the total market capitalization surged to Rs4.89 trillion, marking a 2.82% increase from Rs4.75 trillion previously.

In USD terms, market cap advanced to $17.44 billion, reflecting a 2.86% weekly increase from $16.96 billion.

Meanwhile, the USD-based weekly return accelerated sharply to 2.85%, compared to just 0.13% last week, signaling renewed investor confidence.

_20251130025638695_fb7b33.jpeg)

The economic backdrop further strengthened market sentiment. OGRA’s decision to cut prescribed gas prices by 3% for SNGPL and 8% for SSGC signaled easing cost pressures for industries and households, while improving financial discipline within the energy chain.

The government’s abolition of the 0.25% Export Development Surcharge was another policy win for exporters aiming to reduce cost burdens and enhance global competitiveness.

Local mobile phone production remained robust, with 25.11 million devices assembled during Jan–Oct 2025, significantly outpacing commercial imports of just 1.7 million units, a reflection of sustained momentum in import substitution.

Meanwhile, CCP’s latest assessment highlighted that the Reko Diq copper-gold project could inject up to $74 billion into Pakistan’s economy over 37 years, strengthening expectations of long-term sectoral transformation.

SBP’s foreign exchange data showed purchases of $257 million from the interbank market in August, up from $189 million in July.

Money supply rose 1.3% month-on-month to Rs44.9 trillion in October, compared to Rs44.84 trillion in September, while increasing 12.5% from October last year’s Rs39.93 trillion.

Inflation for November is projected between 5% and 6%, consistent with stable price trends but reflecting continued pressure from food and agriculture.

In monetary adjustments, SBP reduced the Special Cash Reserve Account remuneration rate by 14 bps to 2.86% for December.

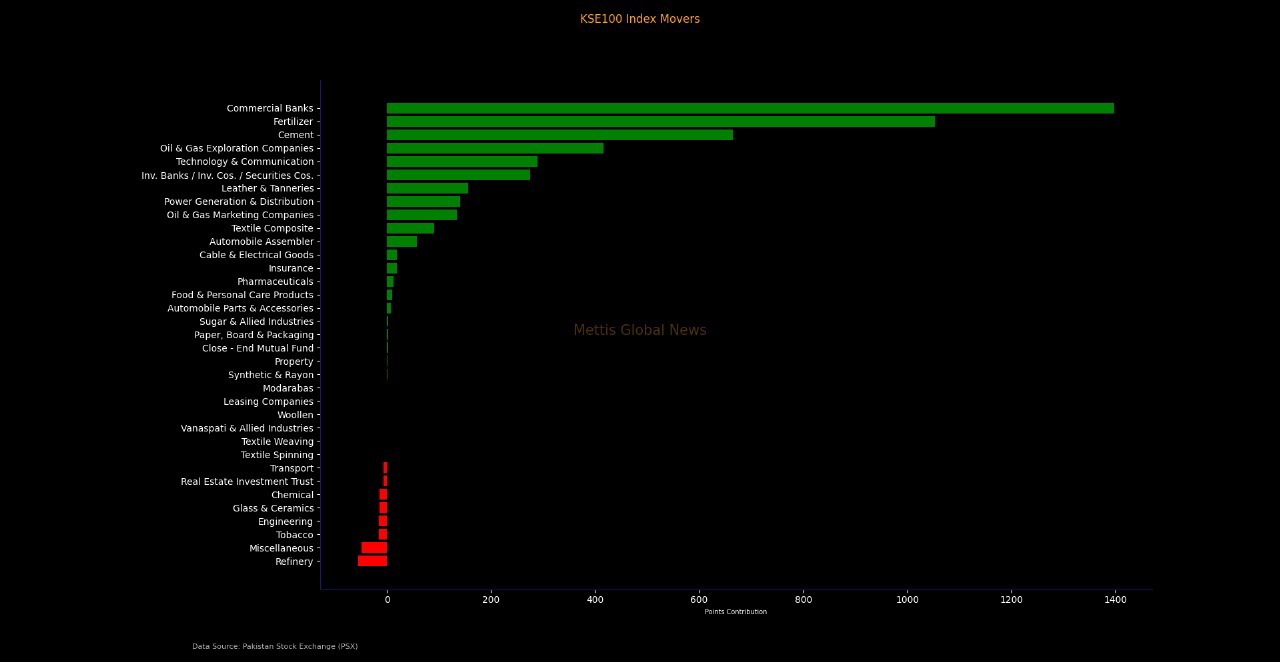

Index Movers:

Sector-wise, heavyweights were the primary engines of this rally. Commercial banks delivered a powerful performance, adding 1,397.62 points to the index, in line with the sector’s bullish momentum and improved financial system outlook.

Fertilizer stocks followed with a contribution of 1,052.56 points, buoyed by stable earnings and strong dividend profiles.

Cement added 664.45 points, reflecting renewed interest in cyclical and construction-related counters. Similarly, Oil & gas exploration companies added another 415.95 points.

Technology & communication contributed 289.30 points, maintaining strong volumes, while investment banks, power generation, automobile assemblers, and leather industries contributed moderate strength.

Meanwhile, refineries, miscellaneous sectors, tobacco, engineering, chemicals, and some textile segments ended the week in the red, dragging the index marginally lower, but not enough to offset strong gains from leading sectors.

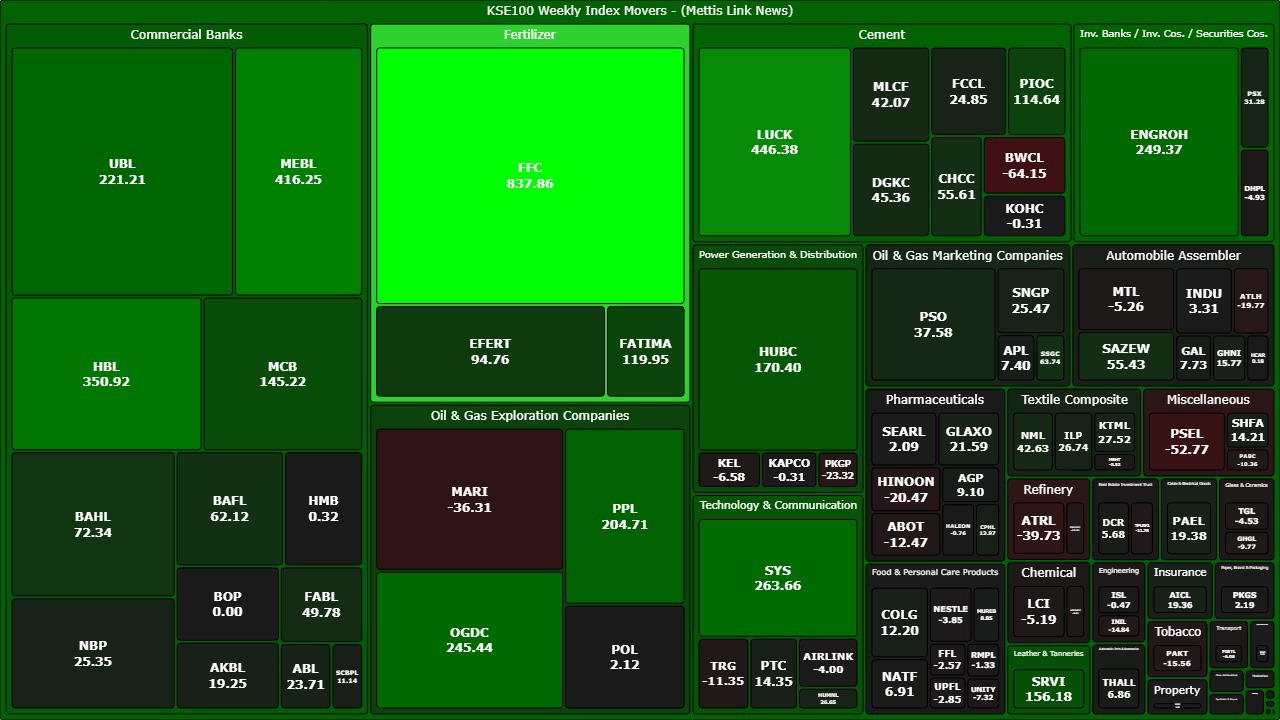

The scrip-level performance reflected a similar pattern, with FFC dominating the week with a sizeable contribution of 837.86 points.

LUCK followed with 446.38 points, MEBL with 416.25 points, and HBL with 350.92 points, showcasing strong interest in blue-chip, dividend-paying, and high-capacity stocks.

Technology giant SYS added 263.65 points, while energy and banking majors, including ENGROH, OGDC, UBL, PPL, HUBC, and MCB added significant support.

On the losing side, BWCL, PSEL, ATRL, MARI, ATLH, and CNERGY were among the biggest laggards, though their combined drag remained overshadowed by broad-based positive flows.

FIPI/LIPI:

Foreign investors continued their selling trend, recording a net outflow of $12.9 million during the week.

However, this foreign selling was entirely absorbed by local institutional investors, who collectively posted a net inflow of $12.9 million.

Banks, DFIs, mutual funds, and insurance companies were the primary buyers, while individuals and companies trimmed their positions.

_20251130030011587_8a1757.jpeg)

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 173,962.82 313.69M | 1.30% 2237.52 |

| ALLSHR | 104,178.62 550.40M | 0.93% 964.13 |

| KSE30 | 52,166.33 164.58M | 1.26% 649.19 |

| KMI30 | 250,496.48 141.11M | 1.59% 3930.77 |

| KMIALLSHR | 67,844.06 318.73M | 1.20% 801.29 |

| BKTi | 47,430.11 44.68M | 0.28% 130.40 |

| OGTi | 36,386.96 9.01M | 0.13% 45.59 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 74,230.00 | 74,370.00 72,595.00 | 610.00 0.83% |

| BRENT CRUDE | 90.43 | 92.95 89.93 | -2.27 -2.45% |

| RICHARDS BAY COAL MONTHLY | 110.00 | 0.00 0.00 | -8.25 -6.98% |

| ROTTERDAM COAL MONTHLY | 112.85 | 0.00 0.00 | -0.05 -0.04% |

| USD RBD PALM OLEIN | 1,157.50 | 1,157.50 1,157.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 86.58 | 89.02 86.35 | -2.32 -2.61% |

| SUGAR #11 WORLD | 14.09 | 14.35 13.90 | 0.16 1.15% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|