Govt releases FY26 Economic Survey

MG News | June 11, 2026 at 02:47 PM GMT+05:00

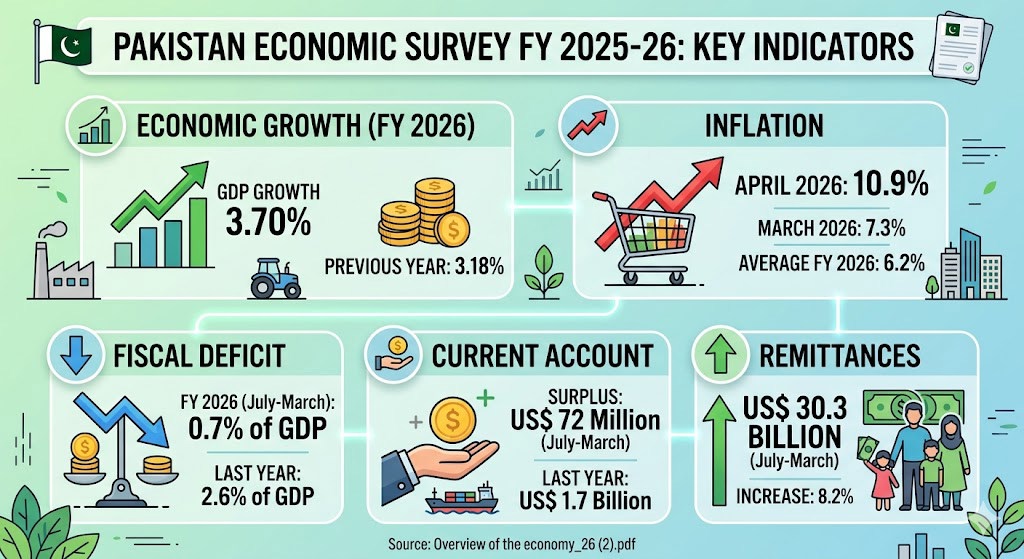

June 11, 2026 (MLN): Finance Minister Muhammad Aurangzeb presented the Economic Survey FY2025-26 during a scheduled press conference, outlines a narrative of macroeconomic stabilization, structural transition, and cautious optimism.

Against a highly volatile global backdrop marked by

geopolitical conflicts and trade barriers, Pakistan’s economy accelerated its

growth momentum, registering a GDP growth rate of 3.70% compared to

3.18% in the previous fiscal year.

This comprehensive review details the sectoral

transformations, fiscal corrections, digital milestones, and structural

vulnerabilities that defined the country's economic landscape in FY26.

1. The Global Backdrop: A Fractured Resilience

The international economic environment in late 2025 and

early 2026 was characterized by deep divisions, showing initial trade

resilience with a 5.1% global trade volume expansion in 2025 before the outlook

darkened rapidly due to the outbreak of conflict in the Middle East.

According to the IMF, global growth is projected to moderate

from 3.4% in 2025 to 3.1% in 2026, while global headline inflation is expected

to tick upward to 4.4% from 4.1%.

Among the major economies, the US remained a strong driver

with growth projected to rise to 2.3% in 2026 due to technology momentum and

expansionary policies, whereas China’s growth is expected to moderate to 4.4%

under the adverse effects of higher US effective tariffs, which hit an

estimated 13.5% by April 2026.

Ultimately, these escalating trade barriers and regional

conflicts triggered severe energy supply route disruptions, heightened shipping

and insurance costs, and added significant downside risks that slowed global

trade volume growth to a projected 2.8% for 2026.

2. Real Sector Performance: Sectoral Triggers of Growth

Pakistan’s GDP growth of 3.70% was anchored by positive

contributions across all three major sectors of the economy services, industry,

and agriculture pushing the total GDP valued at current market prices to Rs

126.9 trillion ($452.1 billion), which marks an 11.3% increase over the

previous year.

Agriculture: Defying the Flood Waters

Despite suffering from the devastating monsoon floods of

2025, the agriculture sector demonstrated remarkable resilience by posting a

growth of 2.89%, which is a significant recovery from the 1.53% growth

recorded in the prior year.

The crucial crop sub-sector shook off a previous contraction

of 1.01% to grow by 1.44% in FY26, as bumper harvests in sugarcane (up 6.2% to

89.45m tonnes), wheat (up 4.3% to 29.61m tonnes), and rice (up 2.8% to 9.99m

tonnes) effectively offset production declines in cotton and maize.

This performance was heavily supplemented by the livestock

sub-sector, which expanded by 3.75% with a renewed policy impetus from the

newly established National Meat Sector Transformation and Export Council.

To sustain this upward trajectory, financial institutions

also scaled up their expansion plans, targeting total agricultural credit

disbursements of Rs3.062tr, representing a 19% increase over the previous

year's allocation.

Manufacturing and Mining: The Industrial Rebound

The industrial sector expanded by 3.51% overall,

driven primarily by a powerful turnaround in Large-Scale Manufacturing (LSM),

which recorded a robust growth rate of 6.11% due to favorable

macroeconomic conditions, a stable exchange rate, and relatively easing

monetary policy.

Out of 22 key manufacturing industries, 16 reported positive

trajectories, including textiles, food, wearing apparel, automobiles, and

petroleum products, culminating in a striking 11.1% year-on-year surge in the

Quantum Index of Manufacturing (QIM) in March 2026 alone.

Simultaneously, the Mining and Quarrying sector broke a

painful four-year streak of continuous contraction to post a marginal positive

growth of 0.4%.

Massive extractions were witnessed during the July-March

period for magnesite (164.8%), rock salt (109.9%), gypsum (67.0%), and iron ore

(41.5%), though critical domestic energy components like natural gas (-3.7%)

and crude oil (-0.6%) experienced slight declines.

Services: The Economic Engine

The services sector maintained its status as the absolute

powerhouse of Pakistan's economy, comprising the largest share at 58.42% of

the total GDP.

The sector expanded by 4.09% during the fiscal year

under review, a growth momentum that was heavily anchored by explosive

acceleration within the information and communication services sub-sector,

which expanded by 7.52%.

3. Macroeconomic Indicators: Income, Investment, and

Savings

The combination of enhanced economic activity and strict

fiscal management trickled down into improved national wealth, allowing

Pakistan's per capita income to rise from $1,751 to $1,901 while the

national exchange rate remained remarkably stable at an average of Rs 280.65

per US Dollar.

The investment-to-GDP ratio stood steady at 14.38%,

primarily driven by a 12.8% increase in private sector capital formation, which

reflected renewed business confidence and pushed total Gross Fixed Capital

Formation (GFCF) up 10.9% to reach Rs 16,071.2 billion.

Furthermore, national savings were recorded at 14.13% of

GDP, which successfully contained foreign savings reliance to just 0.24% of

GDP, signaling that the country managed to significantly limit its dependence

on volatile external debt financing for immediate capital requirements.

4. Fiscal and Monetary Discipline: Reining in the Deficit

The defining feature of the FY26 economic trajectory was a

sharp commitment to fiscal consolidation, widely supported by implementation

coordination via the National Fiscal Pact to improve revenue mobilization and

strengthen expenditure efficiency.

During the July-March FY26 period, the national fiscal

deficit narrowed drastically to just 0.7% of GDP (Rs 856.4 billion) from

the 2.6% of GDP recorded in the same period last year, while the primary

surplus rose to 3.2% of GDP (Rs 4,091.5 billion).

Total national revenue increased by 10.7% to Rs14.80tr boosted

by an 11.3% growth in tax revenues and a 10.1% rise in FBR net collections while

total public expenditures actually declined by 4.2% to Rs15.65tr, driven almost

entirely by a massive 23.2% drop in debt markup payments.

In the monetary domain, Broad Money (M2) expanded by 15.4%,

yet government borrowing for budgetary support fell dramatically from Rs1.32tr

down to Rs850.6bn, creating essential fiscal space that allowed private sector

credit to absorb Rs934.1bn for working capital and fixed investment loans.

5. Financial and Capital Markets: Investor Euphoria

Pakistan's capital markets outpaced several major global

stock indexes during the fiscal year, buoyed by strong corporate earnings, a

decline in the policy rate, and investor confidence stemming from successful

reviews and tranche disbursements under the IMF-EFF Programme.

The benchmark KSE-100 index posted a significant growth of 18.4%

during the July–March FY26 period, pushing total Pakistan Stock Exchange (PSX)

market capitalization up 8.5% to close at Rs16.534tr ($59.23bn) by March 31,

2026.

Islamic finance saw massive institutional expansion, with

Shariah-compliant assets growing to represent 64% of total market

capitalization ($10.6tr) across 308 listed securities.

The government capitalized on this momentum by successfully

generating Rs2.25tr through sovereign Sukuk issuances including a new 10-year

zero-coupon fixed-rate Sukuk which effectively expanded the share of

Shariah-compliant instruments within total government securities to 14.5%.

6. External Sector, Trade, and Public Debt Profile

While the structural architecture of the external sector

stabilized, the core trade balance remained under distinct geopolitical

pressure.

Supported by robust remittance channels, the current account

recorded a marginal surplus of $72m for July–March FY26, anchored

single-handedly by overseas workers' remittances which grew 8.2% to achieve an

inflow of $30.3bn.

Conversely, the merchandise trade deficit widened to $27.9bn

from $22.7bn last year, as an economic rebound caused imports to rise by 6.9%

while formal exports contracted by 8% due to weakened global demand and

regional shipping lane gridlocks.

This trade gap was partially salvaged by the services

account deficit narrowing to $2.1bn on the back of a 19.8% surge in IT

exports, helping push liquid foreign exchange reserves to $21.8bn

($16.4bn with the SBP).

Total public debt stood at Rs83.285tr ($92.2bn in

external debt), but prudent borrowing limits restricted debt growth to 3.4%

during the nine-month period compared to 6.7% previously, while active debt

portfolio risk management operations helped increase the average time to

maturity of domestic debt to 3.86 years.

7. Inflation and Energy: Vulnerability to Global Crises

Despite structural adjustments, the final quarter of the

fiscal year exposed Pakistan's persistent exposure to external volatility.

Average CPI inflation for the July-April period sat at 6.2%,

but regional conflicts and supply chain constraints in late spring caused an

abrupt spike, jumping from 7.3% in March 2026 to 10.9% in April 2026.

These same geopolitical tensions around the Strait of Hormuz

drove the national energy import bill up by 6.3% to $8.9bn due to

international oil price volatility.

In response to these vulnerabilities, Pakistan pressed

forward on its indigenous green energy transition, expanding total installed

generation capacity to 49,651 MW, where clean, environment-friendly sources hydel,

nuclear, and renewables successfully captured the majority share (50.8%)

over thermal alternatives.

8. Technology and Digital Infrastructure: The 5G Era

Begins

The Information Technology and telecommunication sector

served as a standout performer, accelerating Pakistan's shift toward a

knowledge-based digital economy.

On March 10, 2026, the Pakistan Telecommunication

Authority (PTA) successfully executed the long-awaited 5G spectrum auction,

generating $509.6m across multiple bands and elevating Pakistan to

"G5 Regulator Advanced Level" status by the International

Telecommunication Union.

This digital boom was mirrored in earnings as total ICT

export remittances jumped 19.7% to $3.38bn, while tech freelancer

exports surged 51% to $856.3m, fueled by programs like DigiSkills.pk

which conducted 5.14m trainings.

Infrastructure and regulatory frameworks were further

enhanced as total telecom subscriptions reached 207.2m, broadband penetration

rose to 64.2% (161m subscribers), and the federal government formally approved

the Artificial Intelligence Policy 2025 to accelerate AI adoption across

key sectors.

9. Social Horizons: Education, Health, and Employment

While fiscal adjustments often squeeze social sectors, the

survey highlighted localized improvements in human capital metrics.

The national literacy rate improved to 63% (73% for

males, 54% for females), while focused provincial expansion plans slashed the

national ratio of Out-of-School Children (OOSC) from 38% down to 28%,

with Balochistan recording the most dramatic turnaround by cutting its

out-of-school ratio from 69% to 45%.

Pakistan’s estimated population reached 252.09 million

with a 2.07% growth rate, showing moderate improvements in life expectancy to

67.8 years and immunization coverage to 73%, alongside major legislative

enactments like the ICT Child Marriage Restraint Act 2025 and the ICT

Domestic Violence Act 2026 to enhance human protection.

On the labor front, the employed workforce expanded to 77.2m

individuals, but due to a massive influx of youth entering the working-age

bracket, the formal unemployment rate ticked upward from 6.3% to 7.1%,

highlighting a pressing need to further accelerate job creation.

10. Climate Change: The Present Reality

The survey leaves no room for ambiguity regarding Pakistan's

profound environmental vulnerability, noting that despite contributing less

than 1% to global greenhouse emissions, the country remains at the absolute

epicenter of climate fallout.

The year 2025 entered the record books as Pakistan's second

warmest year in over six decades, experiencing a national mean temperature of

23.9°C with shifting monsoon dynamics that triggered catastrophic

multi-provincial floods.

These late 2025 floods alone claimed 1,039 lives, displaced

4 million citizens, and directly inflicted Rs822bn in damages, cementing

climate change as a critical present risk and a major downside driver

threatening to disrupt Pakistan's medium-term economic growth

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,846.68 370.24M | -0.81% -1463.60 |

| ALLSHR | 108,777.96 842.70M | -0.57% -624.36 |

| KSE30 | 53,571.08 118.45M | -0.81% -434.78 |

| KMI30 | 253,007.72 126.35M | -1.06% -2717.47 |

| KMIALLSHR | 69,727.55 549.62M | -0.70% -488.73 |

| BKTi | 52,178.22 35.92M | -0.12% -62.01 |

| OGTi | 35,518.90 13.54M | -0.77% -274.36 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,765.00 | 64,610.00 63,260.00 | -355.00 -0.55% |

| BRENT CRUDE | 89.12 | 90.03 86.60 | 1.40 1.60% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -4.00 -3.65% |

| ROTTERDAM COAL MONTHLY | 122.00 | 122.00 122.00 | 0.75 0.62% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.40 | 84.61 81.27 | 1.27 1.55% |

| SUGAR #11 WORLD | 16.74 | 16.75 16.33 | 0.27 1.64% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|