Geopolitical shock wipes over 19,000 points off KSE-100 in March

_20260401103816024_f77f1a.jpeg?width=950&height=450&format=Webp)

MG News | April 01, 2026 at 03:57 PM GMT+05:00

April 01, 2026 (MLN): The Pakistan Stock Exchange’s benchmark KSE-100 Index recorded its worst monthly performance in six years in March 2026, plunging by 19,319 points, or 11.5%, to close at 148,743.

The index fell to an intra-month low of 144,119, down 23,943 points from February’s close, as a series of negative developments compounded and eroded investor confidence across multiple fronts.

_20260401103824355_13a253.jpeg)

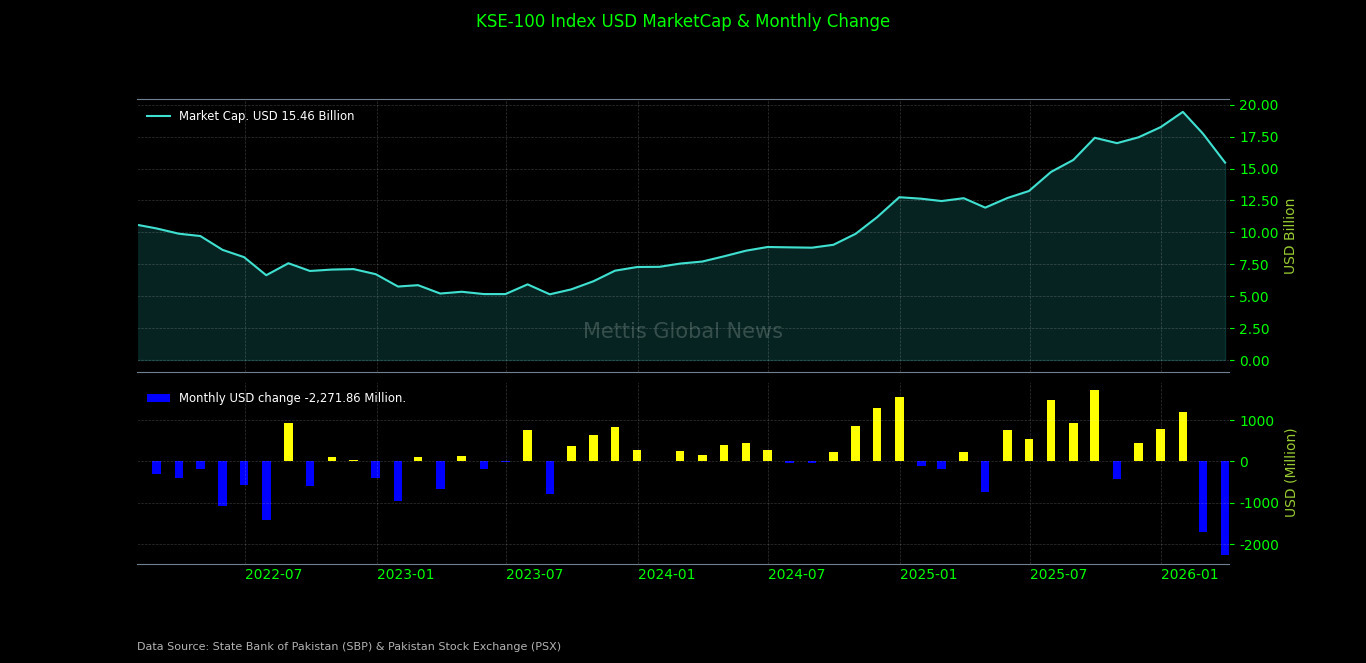

Market Capitalization:

_20260401103757303_078fc2.jpeg)

It came amid one of the most turbulent geopolitical environments the region has seen in decades, with an escalating war between the United States, Israel, and Iran.

This conflict has shaken global energy markets, disrupted international supply chains, and cast a long shadow over Pakistan's hard-won macroeconomic recovery.

At the start of the month, the United States and Israel launched coordinated military strikes against critical infrastructure in Iran, targeting military installations, civilian facilities, energy assets, and nuclear sites, and assassinating senior Iranian military and civilian leadership, including the Supreme Leader.

The strikes represented a dramatic escalation of tensions that had been simmering for months.

Iran's retaliation was swift and far-reaching. The country launched waves of missile and drone strikes against Israeli and US military and commercial assets across the region, while simultaneously targeting the energy infrastructure and airports of Gulf neighbours, among them the UAE, Saudi Arabia, Kuwait, Qatar, Bahrain, and Oman.

Most consequentially for global markets, Iran moved to close the Strait of Hormuz, the narrow waterway through which approximately 20% of the world's oil and liquefied natural gas (LNG) supply passes each day.

An Iranian strike on Qatar's LNG plant delivered an additional shock to global gas markets, compounding the Strait of Hormuz closure.

These are not merely headline numbers; they represent a fundamental supply disruption that sent economies from London to Tokyo scrambling to secure energy at any price.

For Pakistan, a net energy-importing country already navigating a fragile balance-of-payments position, the timing could hardly have been worse.

The surge in global crude prices translated almost immediately into a roughly 20% spike in domestic fuel prices during the month. The government moved first to raise MS (motor spirit) and HSD (high-speed diesel) prices by PKR 55 per litre effective March 7, citing higher ex-refinery costs.

Subsequently, despite continued surges in international oil prices and elevated regional risk premiums, the government chose to hold domestic prices steady on multiple occasions.

It absorbed the differential through petroleum development charges (PDCs), which swelled to approximately PKR 96/litre for MS and PKR 204/litre for HSD, implying a total subsidy burden of roughly PKR 125 billion in PDC claims alone.

Also, the Prime Minister announced a nationwide austerity drive aimed at conserving fuel consumption, coupled with cuts to the development budget, in an effort to balance the books.

Pakistan, alongside Egypt, Türkiye, and Saudi Arabia, has been actively leading mediation efforts to broker a ceasefire between the warring parties.

Pakistan's role as a lead mediator carries diplomatic prestige but also presents risks, particularly to the country's relations with both Western powers and Gulf partners whose infrastructure and economies are being damaged in the conflict.

The Ramadan seasonal factor added a structural headwind to market liquidity, with activity typically thinning during the holy month as trading desks operate at reduced capacity and investor attention shifts away from the market.

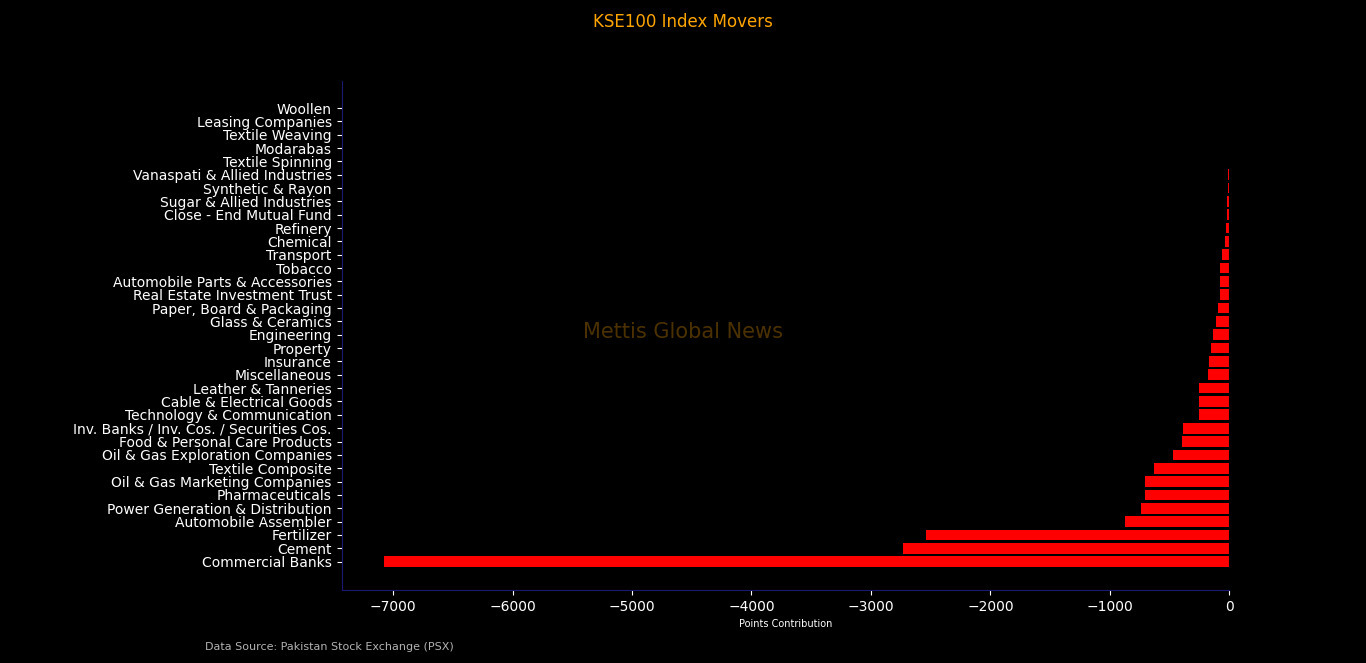

Index Contributors:

Every single sector on the KSE-100 finished the month in negative territory. Commercial Banks were the largest drag on the index, shedding 7,078 index points.

Cement followed with a loss of 2,732 points, weighed down by demand concerns and higher input costs.

The Fertilizer sector lost 2,543 points, a significant reversal for an otherwise resilient sector, on the back of energy price shocks affecting production economics.

The Automobile Assembler sector shed 874 points as consumer sentiment weakened and fears of stagflationary conditions mounted.

Power Generation and Distribution lost 741 points, while Pharmaceuticals and Oil & Gas Marketing Companies each fell by over 700 points.

Technology & Communication, which had been one of the index's strongest performers in prior months, fell 258 points, though SYS, the largest contributor to the sector, managed to buck the trend with a positive contribution of 204 points, the single largest index gainer for the month.

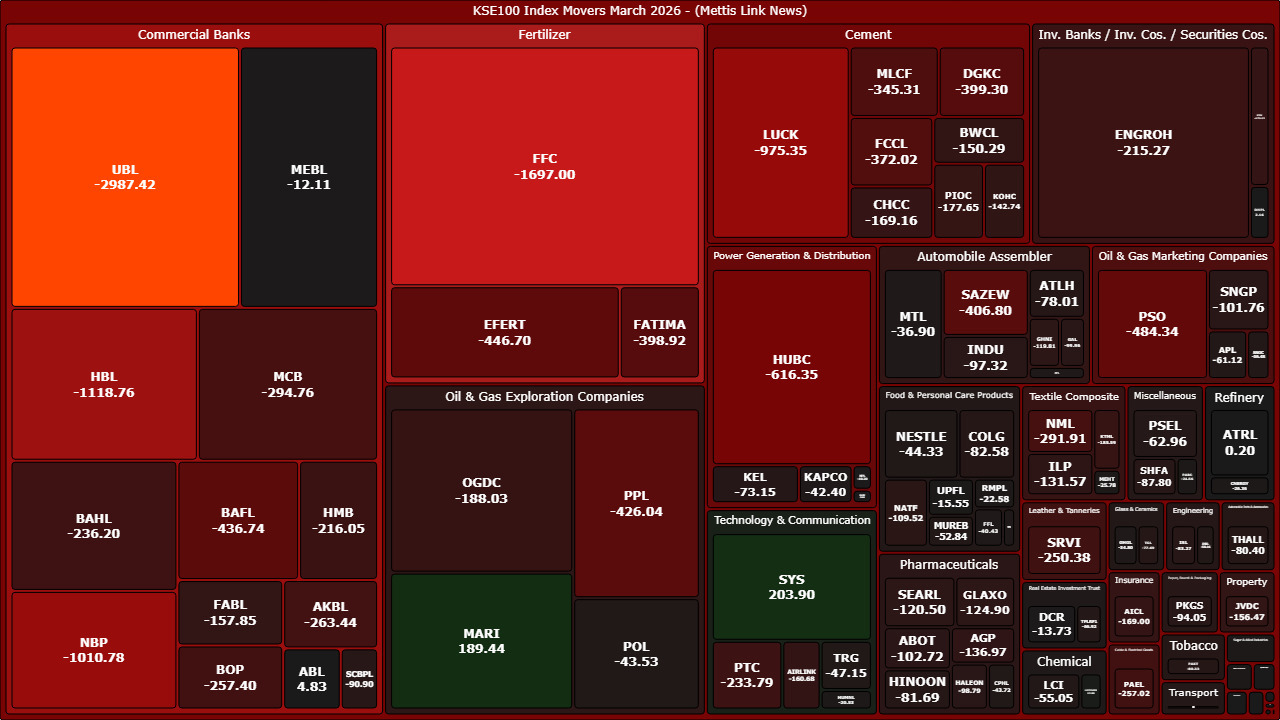

At the scrip level, the damage was heavily concentrated in the large-cap, high-weight components of the index. UBL alone accounted for a staggering 2,987 index points of decline, making it the single largest individual detractor for March.

FFC contributed a loss of 1,697 points, HBL shed 1,119 points, NBP fell 1,011 points, and LUCK, the cement giant, lost 975 points. BAFL (−437 pts), PPL (−426 pts), EFERT (−447 pts), and PSO (−484 pts) were also among the significant laggards.

On the positive side, the gainers were few and far between. SYS, the technology conglomerate, added 204 index points, while MARI, the upstream oil and gas explorer, contributed 189 points, benefiting from the spike in global energy prices, boosting the valuation of its hydrocarbon reserves.

FIPI/LIPI:

The month's trading flows painted a picture of a market absorbing foreign selling with domestic buying support, a dynamic that helped prevent an even steeper decline.

Foreign investors (FIPI) were net sellers to the tune of $53.3 million for the month. The bulk of the outflow came from Foreign Corporations, which sold down a net $71.8 million in equities.

Overseas Pakistanis provided a partial offset, recording a net buy of $18.4 million.

On the local investor (LIPI) side, the picture was more nuanced. Individual investors were the largest net buyers, absorbing $48.2 million, followed by Banks and DFIs at $46.3 million.

Other Organisations added $19.0 million. However, Mutual Funds were notable net sellers at $55.7 million, suggesting institutional redemption pressure or strategic de-risking, while Broker Proprietary Trading desks were marginally net short at $3.1 million.

Overall, LIPI registered a net inflow of $53.3 million, effectively offsetting the FIPI outflow on a net basis.

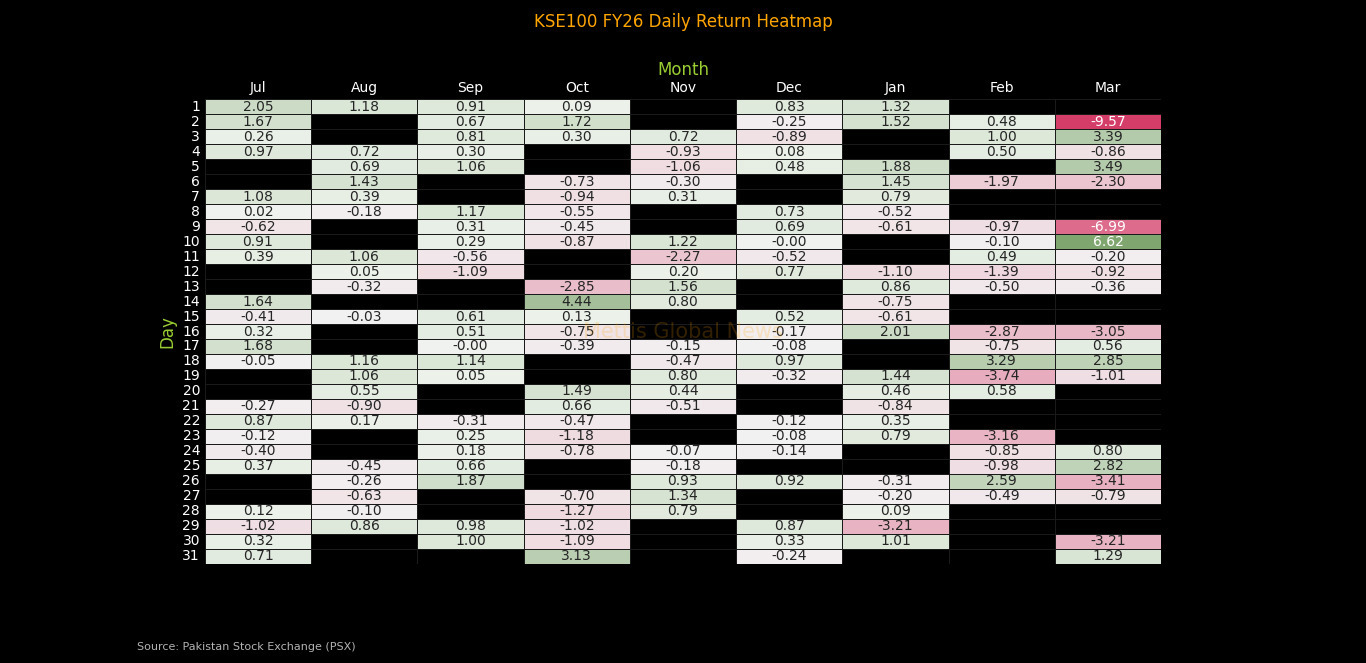

_20260401103718110_f86193.jpeg)

The KSE-100 FY26 Daily Return Heatmap shows that the early months of the fiscal year were marked by broadly positive daily returns and relatively modest volatility.

July and August posted predominantly green sessions, consistent with the broader bull run in progress. September showed some choppiness, a −1.09% on the 12th and −0.32% on the 13th, but no severe daily losses.

The largest single positive session in this stretch was July 1 (+2.05%) and August 6 (+1.43%).

October was the noisiest month of the first half, with sharp swings in both directions. October 14 delivered the single largest daily gain of the entire FY26 period, shown at +4.44%, while October 13 was the worst day of the month at −2.85%.

The tug-of-war between bulls and bears reflected broader global uncertainty, yet the month ultimately closed positively.

November introduced a string of negative sessions, with the −2.27% on the 11th being the most notable. December was relatively contained, oscillating around small gains and losses, consistent with year-end consolidation and thin holiday volumes.

January produced the strongest cluster of green days in the second half of FY26, with multiple sessions above +1%, confirming the index's run toward its all-time high of 184,174 points.

February's daily pattern signals the beginning of the deterioration. A −1.97% on the 6th, −2.87% on the 16th, −3.74% on the 19th, and −3.16% on the 23rd collectively point to mounting selling pressure, even as some days attempted recovery. The month ended with a net negative return of −8.75% (PKR) and −8.65% (USD).

March is visually the most alarming column in the entire heatmap. The opening day of the month delivered a brutal 9.57%, by far the single worst trading day of FY26, triggered by the initial shock of the US-Iran military escalation and Iran's closure of the Strait of Hormuz.

The 9th of March followed with another severe −6.99% session. A brief but sharp relief rally emerged on the 10th (+6.62%), as markets attempted to price in mediation hopes, but it proved short-lived. Subsequent sessions on the 16th (−3.05%), 26th (−3.41%), and 30th (−3.21%) continued the downward grind.

The month closed with a modest +1.29% on the 31st, insufficient to offset the accumulated damage.

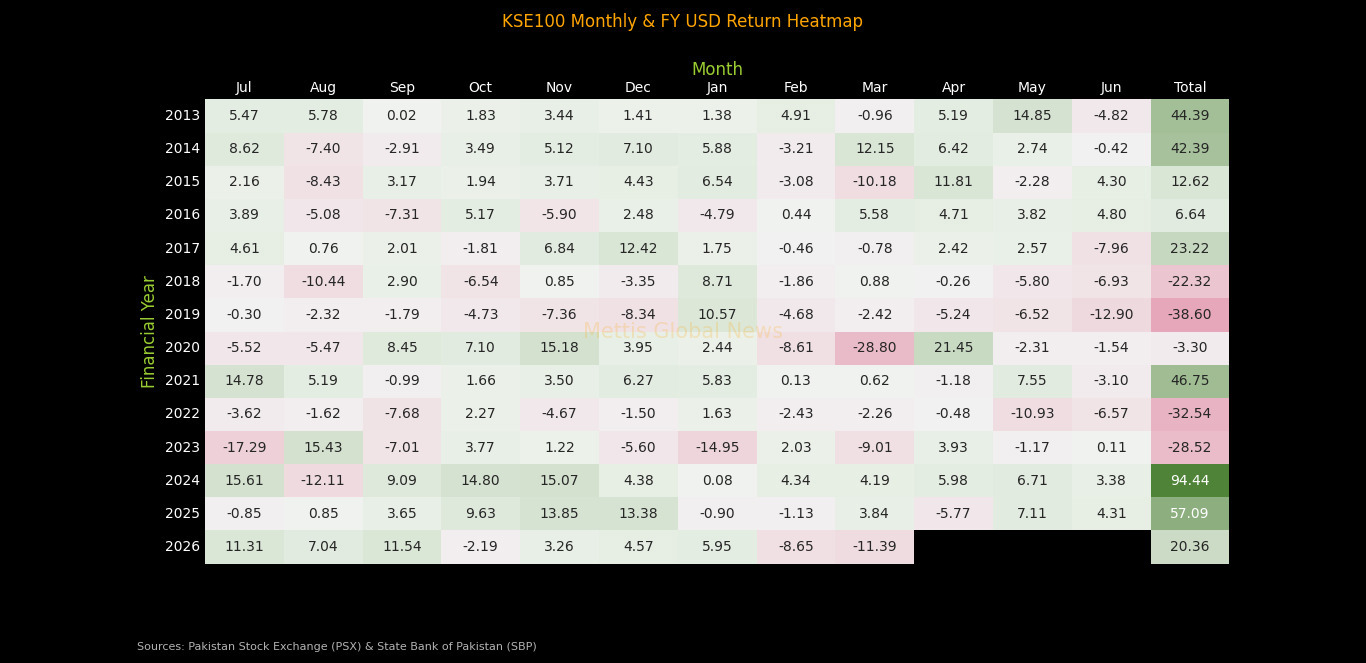

Considering KSE-100 Monthly & FY USD Return data, FY2013–FY2014 stand out as among the strongest in USD return terms, delivering full-year returns of +44.39% and +42.39% respectively. The rupee was relatively stable, and the index was in a structural uptrend driven by declining inflation and improving macro fundamentals. May 2014's +14.85% was the single best monthly USD return in the entire dataset.

In FY2015–FY2017 returns moderated but remained solidly positive at +12.62%, +6.64%, and +23.22%. FY2017 was rescued by a remarkable December 2016 (+12.42% USD), though that year also saw a −7.96% in June 2017 as the index began pricing in political uncertainty. The rupee remained managed during this period, keeping currency drag minimal.

FY2018–FY2019: These two years represent the worst sustained period of USD returns in recent history, delivering −22.32% and −38.60% respectively. The pain was dual-sourced: a collapsing index (political uncertainty, rising interest rates, IMF programme pressures) compounded by severe PKR devaluation — the rupee lost over 30% of its value against the dollar in FY2019.

August 2018's −10.44% and January 2019's −14.95% are among the most painful individual monthly readings in the dataset.

March 2020's −28.80% in FY2020 is the single worst month across all years in USD terms, marking the COVID-19 shock.

FY2020 as a full year delivered −3.30% in USD terms, masking enormous intra-year volatility. March 2020's −28.80% was followed by April 2020's +21.45% — the two largest monthly swings in the dataset — as global markets collapsed and then bounced on central bank stimulus.

At +46.75% in USD terms, FY2021 was the strongest full-year performance in the dataset, driven by aggressive SBP rate cuts, fiscal stimulus, and a recovering economy. July 2021's +14.78% was the best opening month of any financial year shown.

FY2022 gave back −32.54% and FY2023 lost −28.52% in USD terms, as the combination of the Ukraine war, global commodity shock, political instability, and PKR freefall devastated foreign investor returns. July 2023's −17.29% stands as the second-worst individual month in the dataset.

At +94.44%, FY2024 was by far the strongest full-year USD return in the history of the dataset — powered by PKR stabilisation after the IMF programme, aggressive rate cuts, and rebounding corporate earnings.

Every single month of FY2024 except August delivered a positive USD return, and months like October (+14.80%), November (+15.07%), and July (+15.61%) were all extraordinary.

FY2025 delivered +57.09% in USD terms, a strong year in absolute terms though naturally lower than the exceptional base of FY2024. October (+9.63%), November (+13.85%), and December (+13.38%) were the standout months.

FY2026 is nine months complete with a year-to-date USD return of +20.36%, which masks a tale of two halves. The July–January period delivered strong returns (including July's +11.31%, September's +11.54%), before February (−8.65%) and March (−11.39%) erased a substantial portion of the fiscal year's gains.

March 2026's −11.39% is the worst single month since March 2020's −28.80%, placing it clearly among the most painful months in the full thirteen-year history of the dataset.

Amid the market turbulence, Pakistan's broader macroeconomic fundamentals, while under pressure, have not yet deteriorated into crisis territory.

CPI for February 2026 came in at 7.0% YoY, up from 5.8% in January, marking the highest reading since October 2024. The uptick was driven primarily by base effects.

For March 2026, the Ministry of Finance estimated that CPI will be in the range of 7.5% - 8.5% YoY, reflecting both base effects and the first-round impact of the mid-month fuel price hike.

The State Bank of Pakistan kept its policy rate unchanged at 10.5% at its March 2026 Monetary Policy Committee meeting, adopting a cautious stance amid rising uncertainty from the Middle East conflict and volatile global commodity prices.

Pakistan registered a current account surplus of $427 million in February 2026, the highest monthly surplus since March 2025. The February surplus was driven largely by a 63% month-on-month contraction in the services deficit.

However, the cumulative 8MFY26 current account deficit stood at $700 million, compared to a surplus of USD 479 million in the same period last year, with imports running approximately 9% higher year-on-year and exports down roughly 5% YoY.

Workers' remittances for February 2026 were USD 3.3 billion, with cumulative 8MFY26 remittances reaching $26.5 billion, up 10% over the same period last year.

The PKR has remained broadly stable, hovering in the PKR 281–282/USD range during most of the month before closing around PKR 279.15/USD.

SBP's foreign exchange reserves stood at approximately $16.4 billion as of the latest available data.

On a relatively positive note, Pakistan and the IMF reached a staff-level agreement on the reviews under the Extended Fund Facility (EFF) and the Resilience and Sustainability Facility (RSF), which is expected to unlock approximately $1.21 billion in financing, subject to Board approval.

On the industrial front, the Large-Scale Manufacturing Index (LSMI) for January 2026 rose 12.1% month-on-month and 10.5% year-on-year, with top contributors including Furniture (+186% YoY), Automobiles (+67% YoY), Other Manufacturing (+59% YoY), and Other Transport Equipment (+36% YoY).

Cumulative 7MFY26 LSMI growth of 5.8% YoY remains positive for the full-year GDP outlook, though soaring energy costs in Q4 FY26 may dampen LSM momentum heading into the final stretch of the fiscal year.

In a development that received somewhat less attention amid the broader geopolitical noise, Barrick Gold announced that it was placing the Reko Diq copper and gold project, one of the largest undeveloped mineral deposits in the world and a flagship foreign direct investment for Pakistan, on hold for one year.

The trajectory of the KSE-100 over the coming weeks and months hinges almost exclusively on one variable: how long the conflict in the Middle East lasts, and whether the Strait of Hormuz can be reopened.

A swift ceasefire, even a fragile one, would likely produce a sharp relief rally. The index could recover a significant portion of March's losses.

Energy prices would ease, and inflationary pressure would abate. The current account would stabilise, and investor confidence would partially return.

A prolonged conflict, on the other hand, would trigger a series of negative effects for Pakistan's economy. Inflation could re-accelerate into double digits, and the monetary easing cycle might reverse with potential rate hikes.

Pressure on the current account and FX reserves would mount as remittances fall and the import bill climbs. Fiscal deficits could widen if fuel subsidies are maintained.

Equity valuations would likely continue to erode as foreign investors reduce exposure to frontier markets.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 180,226.46 316.95M | -1.11% -2015.32 |

| ALLSHR | 109,499.37 726.42M | -0.98% -1084.30 |

| KSE30 | 53,807.27 73.36M | -1.15% -624.44 |

| KMI30 | 253,849.09 92.18M | -1.19% -3065.12 |

| KMIALLSHR | 70,252.16 473.37M | -1.11% -789.14 |

| BKTi | 51,180.70 15.02M | -1.03% -532.06 |

| OGTi | 36,245.96 6.65M | -1.13% -413.63 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,185.00 | 64,680.00 62,605.00 | -900.00 -1.40% |

| BRENT CRUDE | 77.36 | 79.80 77.31 | 1.35 1.78% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 72.71 | 75.08 72.65 | 1.30 1.82% |

| SUGAR #11 WORLD | 14.68 | 14.98 14.65 | -0.20 -1.34% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|