SBP leaves policy rate unchanged at 22%

MG News | October 30, 2023 at 04:30 PM GMT+05:00

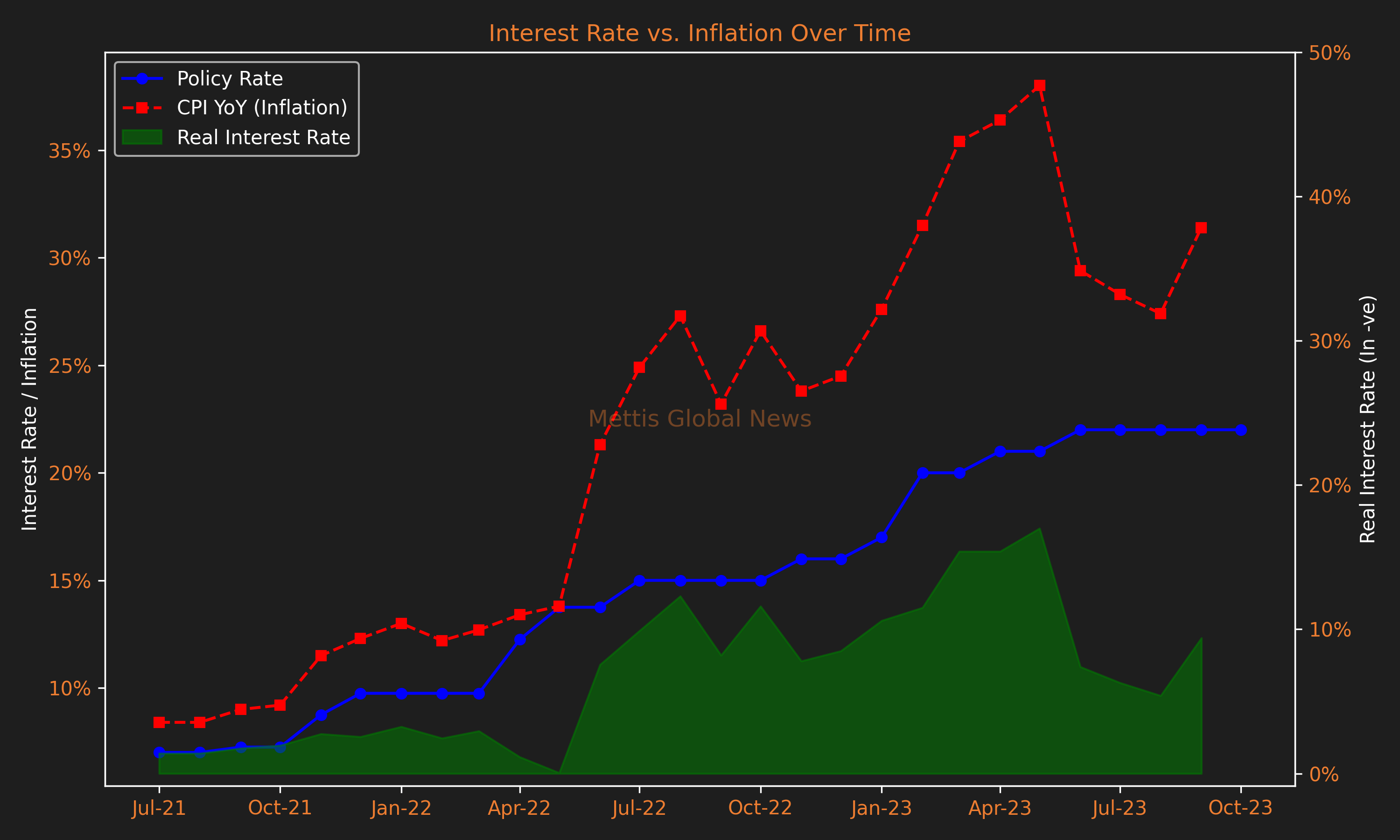

October 30, 2023 (MLN): The Monetary Policy Committee (MPC) of the State Bank of Pakistan (SBP) in its meeting held today, has decided to keep the policy rate unchanged at 22%.

The decision came in line with the market expectations wherein the majority of market participants were in consensus on the rate pause.

The Committee noted that headline inflation rose in September 2023 as expected.

However, it is projected to decline in October and then maintain a downward trajectory, especially in the second half of the fiscal year.

While the recent volatility in global oil prices as well as the increase in gas tariffs from November 2023 pose some risks to the FY24 outlook for inflation and the current account, the Committee also noted some offsetting factors.

These include the targeted fiscal consolidation in Q1; improvement in market availability of key commodities; and the alignment of interbank and open market exchange rates.

The MPC noted the following key developments since its September meeting.

First, the initial estimates for Kharif crops are encouraging and will have positive effects on other key sectors of the economy.

Second, the current account deficit narrowed considerably in August and September, which helped to stabilize the SBP’s FX reserves position amidst tepid external financing in these two months.

Third, fiscal consolidation remained on track, with both fiscal and primary balances improving during Q1-FY24.

Fourth, while core inflation remains sticky, inflation expectations of both consumers and businesses improved in the latest pulse surveys.

However, global oil prices remain quite volatile and the conflict in the Middle East makes its outlook even more uncertain.

In light of these developments, the MPC emphasized on continuing with the tight monetary policy stance.

The MPC reiterated its earlier view that the real policy rate is significantly positive on a 12-month forward-looking basis and is appropriate to bring inflation down to the medium-term target of 5-7% by end-FY25.

However, the MPC noted that this outlook is based on continued fiscal consolidation and timely realization of planned external inflows.

Real sector

Recent data on economic activity reinforces the MPC’s earlier expectation of moderate growth for this year.

In particular, the latest production estimates of major Kharif crops show a considerable increase compared to last year.

These improved crop output estimates are supported by higher fertilizer off-take and better availability of water.

Also, a moderate recovery in other key activity indicators like cement, POL, and auto sales is gaining traction.

Moreover, large-scale manufacturing (LSM) output has indicated a gradual improvement in the first two months of this year, with major contributions coming from domestic-oriented sectors.

External sector

The MPC noted a substantial improvement in the current account balance, as the deficit narrowed over 58% YoY to $947 million in Jul-Sep FY24, while almost leveling out in September 2023.

Both exports and workers’ remittances improved in September over the preceding two months.

The reforms related to exchange companies introduced in early September, coupled with administrative actions against illicit market activities, also helped improve FX market sentiments and liquidity.

The improved inflows in the interbank market helped stabilize the SBP’s FX reserves around $7.5 billion as of October 20, amidst tepid official inflows during August and September.

Nonetheless, the MPC noted that a successful and timely completion of the upcoming IMF-SBA review would help unlock other multilateral and bilateral financing.

Fiscal sector

In Q1-FY24, fiscal indicators improved compared to the first quarter of the last fiscal year. Specifically, the fiscal deficit improved to 0.9% of GDP from 1% and the primary balance posted a surplus of 0.4%, compared with 0.2% last year.

This improvement reflects both better revenue collection and restrained spending. FBR’s revenue recorded 24.9% growth over the same period last year.

Similarly, non-tax revenues almost doubled mainly due to a sharp rate-driven increase in PDL collection.

At the same time, total expenditures remained at last year’s level, supported by a considerable reduction in subsidies and grants. The MPC noted that continued fiscal prudence and meeting the targeted fiscal consolidation is imperative for keeping inflation on a downward trajectory

Money and credit

The broad money (M2) growth decelerated to 12.9 percent as of end-September from 14.2% at end-June 2023, primarily due to continued slowdown in private sector credit and more than seasonal retirement in commodity operations financing.

Similarly, the reserve money growth has slowed down since June, which is primarily explained by a significant deceleration in the growth of currency in circulation.

The MPC noted that since June, the Net Foreign Assets (NFA) of SBP and the banking system expanded owing mainly to significant FX inflows in July, while Net Domestic Assets (NDA) contracted, leading to an improvement in the composition of both M2 and reserve money.

It is also expected that the planned fiscal consolidation and realization of expected external inflows will create space for credit to the private sector and also improve the NFA of the banking system.

Inflation outlook

As anticipated, headline inflation surged to 31.4% YoY in September.

The MPC expects inflation to decline significantly in October, owing to downward adjustments in fuel prices, easing prices of some major food commodities, and a favorable base effect.

The Committee also reaffirmed its earlier assessment that inflation will decline substantially from the second half of FY24, barring any major adverse developments.

The recent uptick and volatile trend in global oil prices, as well as the second-round effects of a substantial increase in gas tariffs, pose some upside risk to the inflation outlook.

Core inflation is also persisting at elevated levels; remained around 21% during the last four months.

However, the Committee noted that fiscal policy is also contributing to the overall stabilization measures, which, coupled with better availability of food commodities, is likely to supplement the central bank’s efforts to bring down inflation.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 177,083.22 263.77M | -0.63% -1116.80 |

| ALLSHR | 106,985.24 708.60M | -0.56% -599.74 |

| KSE30 | 52,836.31 88.14M | -0.71% -377.39 |

| KMI30 | 249,402.60 98.38M | -0.75% -1875.51 |

| KMIALLSHR | 68,629.46 382.90M | -0.54% -369.14 |

| BKTi | 50,585.57 17.47M | -0.42% -215.71 |

| OGTi | 34,443.84 5.73M | -1.18% -411.99 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,665.00 | 64,805.00 64,140.00 | 180.00 0.28% |

| BRENT CRUDE | 78.36 | 79.84 78.11 | -1.00 -1.26% |

| RICHARDS BAY COAL MONTHLY | 107.75 | 0.00 0.00 | 0.95 0.89% |

| ROTTERDAM COAL MONTHLY | 118.00 | 120.40 118.00 | 0.25 0.21% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 74.51 | 76.06 74.24 | -1.26 -1.66% |

| SUGAR #11 WORLD | 15.06 | 15.33 15.01 | 0.05 0.33% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|