Weekly Market Roundup

_20260606124224963_473c6c.jpeg?width=950&height=450&format=Webp)

MG News | June 06, 2026 at 05:46 PM GMT+05:00

June 06, 2026 (MLN): Pakistan’s equity market witnessed a correction during the week ended June 5, 2026, with the benchmark KSE-100 Index closing at 170,478.94, compared to 173,962.82 recorded on May 29, 2026.

The benchmark KSE-100 Index closed the week 3,483.88 points

lower, posting a 2.00% WoW decline, as heightened uncertainty surrounding

developments in the Middle East kept investors on the sidelines.

Concerns over the lack of meaningful headway in U.S.-Iran

talks, coupled with renewed regional frictions, dampened market confidence and

encouraged profit-taking, resulting in a broadly negative trading trend

throughout the week._20260606124233864_a4be55.jpeg)

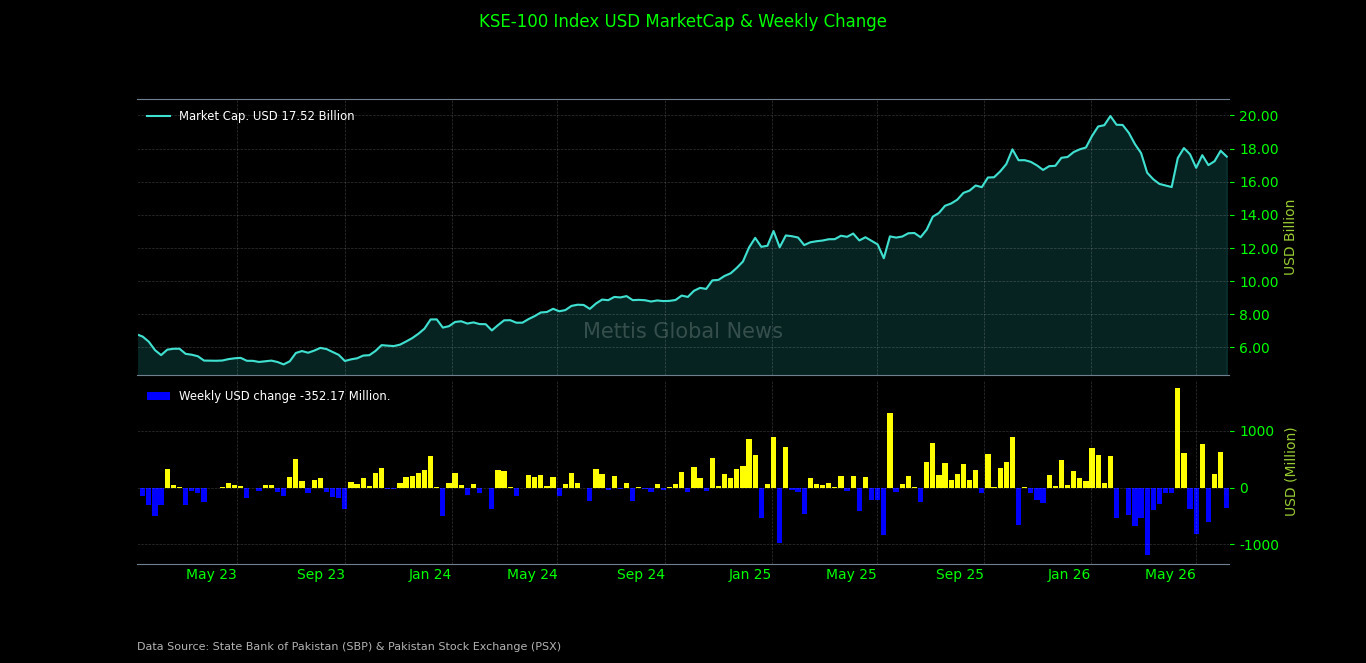

Market Capitalization

Total market capitalization decreased in line with the

benchmark index's performance. As of June 5, 2026, market capitalization stood

at Rs4.877 trillion, compared to Rs4.976tr on May 29, 2026, marked a decline of

Rs99.66bn or 2.00% WoW.

In USD terms, market capitalization fell to $17.52bn from

$17.87bn in the previous week, showing a decrease of approximately $352.17m

amid lower equity valuations.

Dollar-adjusted returns turned negative during the week,

registering -1.97% WoW compared to a positive 3.65% recorded in the previous

week, indicating weaker investor returns in both local and foreign currency

terms._20260606124204543_0d4cb2.jpeg)

On the macroeconomic front, Pakistan’s trade deficit

narrowed sharply to $2.58bn in May 2026, driven by a steep decline

in imports and higher exports, though the cumulative FY26 trade gap remained

significantly wider year-on-year.

Pakistan’s headline inflation

accelerated to 11.7% YoY in May 2026, driven by broad-based

price pressures across urban and rural areas, with core inflation indicators

also showing continued strengthening.

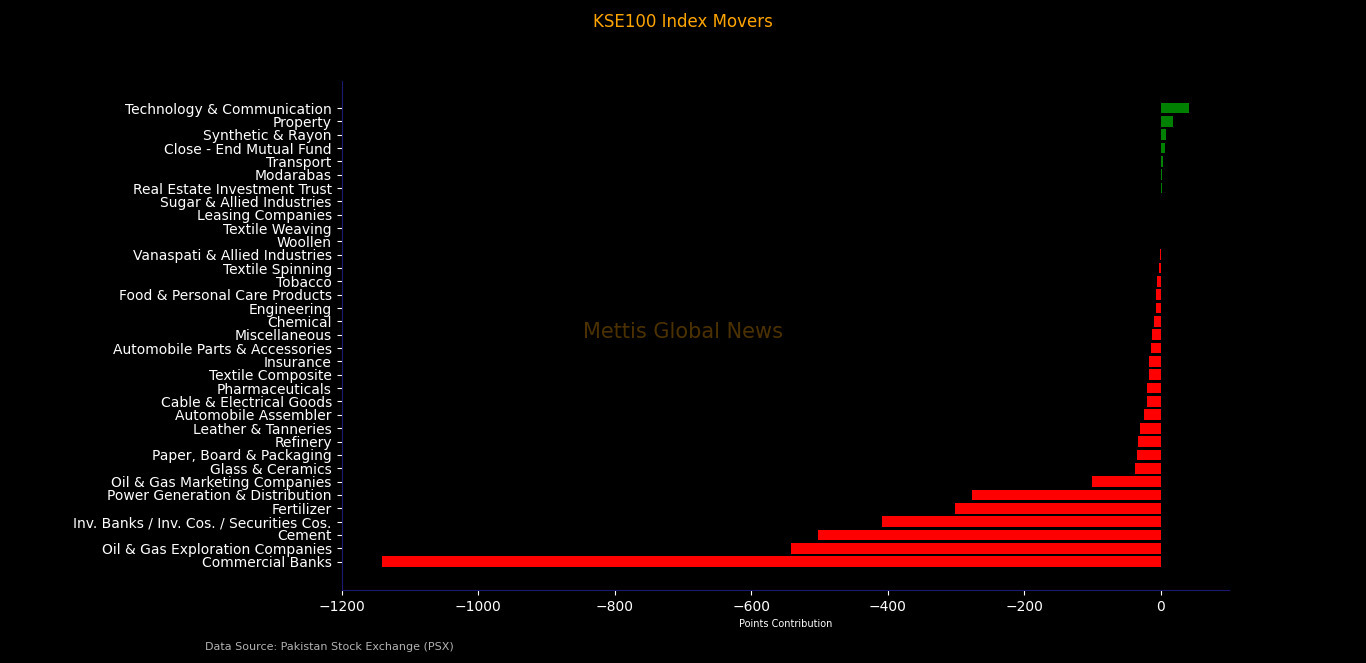

Index Movers

Sector-wise, the decline was broad-based and led by

index-heavy sectors.

Commercial banks emerged as the largest negative contributor

to the benchmark index, dragging it down by 1,141.42 points. Oil & Gas

Exploration Companies trimmed 541.97 points, while cement stocks erased 502.38

points during the week.

Investment banks, investment companies and securities

companies contributed negatively by 408.46 points, followed by fertilizer

(-301.88 points), power generation & distribution (-276.91 points), oil

& gas marketing companies (-101.03 points), glass & ceramics (-37.65

points),

Paper, board & packaging (-34.79 points), refinery

(-33.52 points), leather & tanneries (-30.19 points), automobile assemblers

(-24.20 points), cable & electrical goods (-20.24 points), pharmaceuticals

(-20.23 points), textile composite (-17.53 points), insurance (-16.44 points),

Automobile parts & accessories (-13.73 points),

miscellaneous (-13.21 points), chemical (-9.99 points), engineering (-7.00

points), food & personal care products (-6.74 points), tobacco (-5.22

points), textile spinning (-1.97 points), vanaspati & allied industries

(-0.05 points), and woollen (-0.02 points).

On the positive side, technology & communication added

41.81 points to the index, followed by property (+18.04 points), synthetic

& rayon (+7.69 points), close-end mutual funds (+5.94 points), transport

(+3.93 points), modarabas (+2.63 points),

Real estate investment trusts (+1.97 points), sugar &

allied industries (+0.44 points), leasing companies (+0.27 points), and textile

weaving (+0.20 points).

The downside was dominated by heavyweight banking,

fertilizer, cement, exploration, and power sector stocks.

Engro Holdings emerged as the largest negative contributor,

dragging the index by 479.23 points, followed by Lucky Cement (-336.93 points),

United Bank Limited (-280.66 points), HUBCO (-242.82 points),

Oil & Gas Development Company (-225.98 points), Bank AL

Habib (-213.30 points), Pakistan Petroleum Limited (-205.95 points), National

Bank of Pakistan (-178.82 points),

Mari Petroleum (-166.20 points), Engro Fertilizers (-162.79

points), Habib Bank Limited (-156.70 points), and Fauji Fertilizer Company

(-149.68 points).

Other major laggards included MCB Bank (-82.21 points),

Meezan Bank (-63.89 points), Sazgar Engineering Works (-62.24 points), Systems

Limited (-59.03 points), Bank Alfalah (-53.59 points),

Askari Bank (-49.09 points), Bank of Punjab (-38.65 points),

Fauji Cement (-34.81 points), Packages Limited (-34.79 points),

K-Electric (-32.82 points), Pakistan State Oil (-32.58

points), Attock Petroleum (-31.08 points), Service Industries (-30.19 points),

Habib Metropolitan Bank (-29.34 points), National Foods (-28.28 points),

Sui Northern Gas Pipelines (-26.78 points), Ghani Glass

(-24.34 points), Attock Refinery (-23.44 points), Bestway Cement (-21.61

points), and Pak Elektron (-20.24 points).

On the upside, Pakistan Stock Exchange was the largest positive contributor, adding 70.77 points to the benchmark index, followed by Pakistan Telecommunication Company (+69.48 points), Pakistan Oilfields (+56.15 points),

Ghani Chemical Industries (+31.58 points), TRG Pakistan

(+30.24 points), Honda Atlas Cars (+27.97 points), Colgate-Palmolive Pakistan

(+26.42 points), Javedan Corporation (+18.04 points),

Soneri Bank (+17.66 points), and Ghandhara Automobiles

(+13.50 points).

Other positive contributors included The Searle Company,

Nestlé Pakistan, Ibrahim Fibres, Hinopak Motors, Fatima Fertilizer, Hub Power

Company (KAPCO), Attock Cement,

Allied Bank, Pakistan International Bulk Terminal, Kohat

Cement, First Habib Modaraba, LCI, CPHL, Meezan Education Trust, Dolmen City

REIT, Pioneer Cement, Hum Network, JDW Sugar Mills, TPL REIT Fund I, Pakistan

General Leasing, and Air Link Communication.

Overall, the market remained under pressure throughout the

week as profit-taking in index-heavy sectors outweighed gains in a limited

number of technology, property, and transport-related stocks, resulting in a

broad-based decline in the benchmark index._20260606124146595_60b258.jpeg)

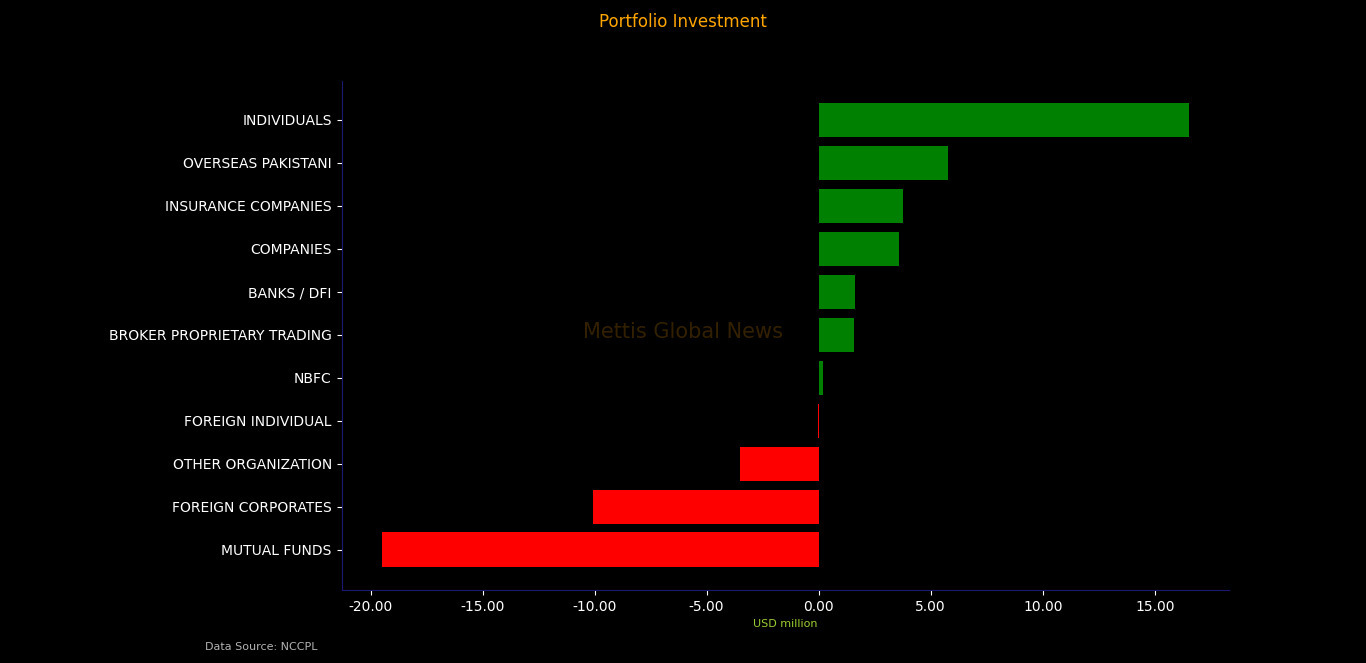

FIPI/LIPI

Foreign investors turned net sellers during the week, with

total net foreign selling in the equity segment standing at Rs1.19bn ($4.28m).

Within foreign flows, foreign individuals recorded net

selling of Rs3.07m ($11,057), while overseas Pakistanis emerged as net buyers

with inflows of Rs1.61bn ($5.79m).

On the local side, individuals emerged as the largest net

buyers with inflows of Rs4.60bn, followed by insurance companies at Rs1.05bn,

companies at Rs997.36m, NBFCs at Rs54.32m, and broker proprietary trading at

Rs437.09m.

Meanwhile, mutual funds remained the largest net sellers,

offloading equities worth Rs5.42bn, followed by other organizations with net

selling of Rs972.07m.

Copyright Mettis Link News

Related News

_20260430120221816_68194f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 175,771.46 113.29M | 2.78% 4750.26 |

| ALLSHR | 106,490.92 305.46M | 2.56% 2654.54 |

| KSE30 | 52,489.89 49.48M | 3.02% 1537.90 |

| KMI30 | 247,995.91 45.03M | 3.06% 7362.04 |

| KMIALLSHR | 68,325.17 143.99M | 2.63% 1752.42 |

| BKTi | 50,038.48 14.95M | 2.80% 1365.25 |

| OGTi | 34,815.58 3.90M | 3.30% 1113.33 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 65,405.00 | 65,570.00 63,875.00 | 1190.00 1.85% |

| BRENT CRUDE | 91.88 | 93.60 89.58 | -4.90 -5.06% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 0.00 0.00 | 0.85 0.71% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 84.54 | 86.20 83.10 | -4.77 -5.34% |

| SUGAR #11 WORLD | 14.76 | 0.00 0.00 | -0.01 -0.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|