Weekly Market Roundup

_20260418090837864_892f21.jpeg?width=950&height=450&format=Webp)

MG News | April 18, 2026 at 02:13 PM GMT+05:00

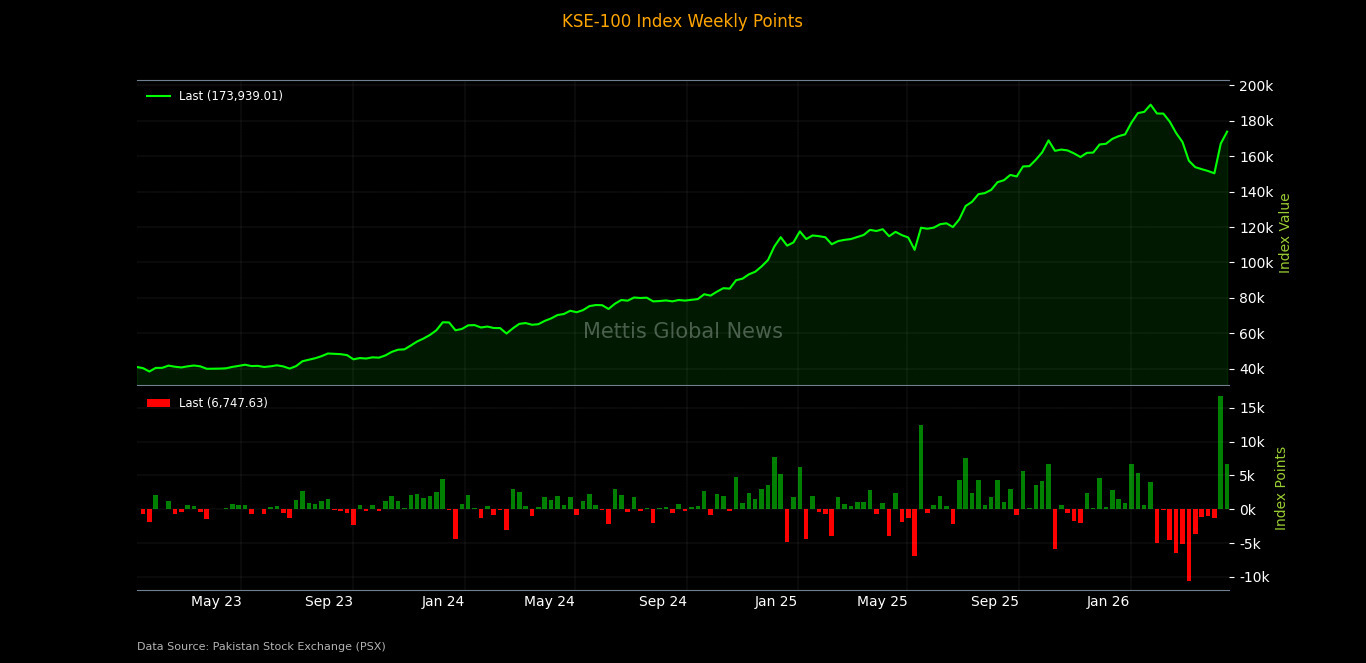

April 18, 2026 (MLN): Pakistan’s equity market

extended its recovery for a second consecutive week, as the benchmark KSE-100

Index closed at 173,939.01 on 17 April 2026, up from 167,191.38

recorded on 10 April 2026.

The index gained 6,747.63 points, translating into a 4.03%

week-on-week (WoW) increase.

Investor sentiment remained upbeat as participants chased

the upside on fresh optimism that a potential deal to end the Middle East

conflict could be within reach, with risk appetite further supported by hopes

of a broader diplomatic thaw.

Additionally, the State Bank of Pakistan’s confirmation of $2bn

inflows from Saudi Arabia and a decline in global oil prices further

strengthened market confidence and supported broad-based buying activity.

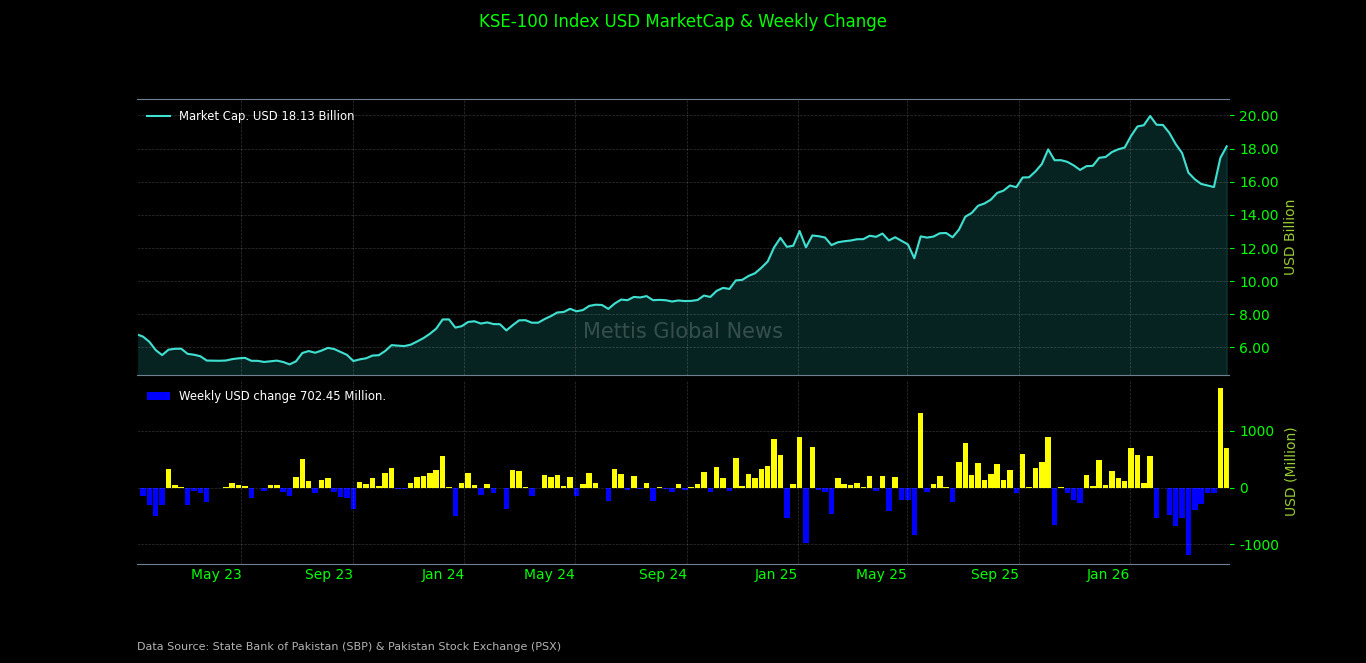

Market Capitalization

Total market capitalization continued its upward trajectory

in line with the index performance. On 17 April 2026, market cap rose to

Rs5.058 trillion, compared to Rs4.863tr on 10 April 2026, showing

a gain of Rs194.38bn or 4.00% WoW.

In USD terms, market capitalization increased to $18.13bn

from $17.43bn in the previous week, showing sustained improvement in

investor confidence alongside relative currency stability.

Dollar-adjusted returns remained positive, though moderated,

coming in at +4.07% WoW, compared to +11.20% in the previous week,

suggesting continued recovery in both local and foreign investor returns._20260418090820281_c9a4f2.jpeg)

On the macroeconomic front, auto financing in Pakistan climbed

to Rs345.34bn in March 2026, driving overall consumer credit to Rs1.06tr

amid strong YoY growth across segments.

Private sector lending also expanded, supported by gains in

agriculture and housing finance, reflecting broad-based credit momentum.

Pakistan’s FDI inflows

rose to $167.6m in March 2026, more than doubling YoY, though sharply lower

on a monthly basis amid volatile investment trends.

Despite stronger direct investment, heavy portfolio outflows

dragged overall foreign investment into negative territory, with cumulative

inflows also declining during 9MFY26.

Pakistan’s REER rose

to 105.17 in March 2026, signaling a stronger rupee but reduced export

competitiveness, while the currency posted marginal gains against the dollar.

Pakistan posted a $1.07bn

current account surplus in March 2026 one of the highest on record driven

by improved remittances and a narrowing monthly trade gap, despite a YoY

decline.

Pakistan’s auto sales surged

39.9% YoY in March 2026 to 15,531 units, signaling a strong recovery,

though MoM decline and a steep 9MFY26 contraction highlight lingering demand

pressures.

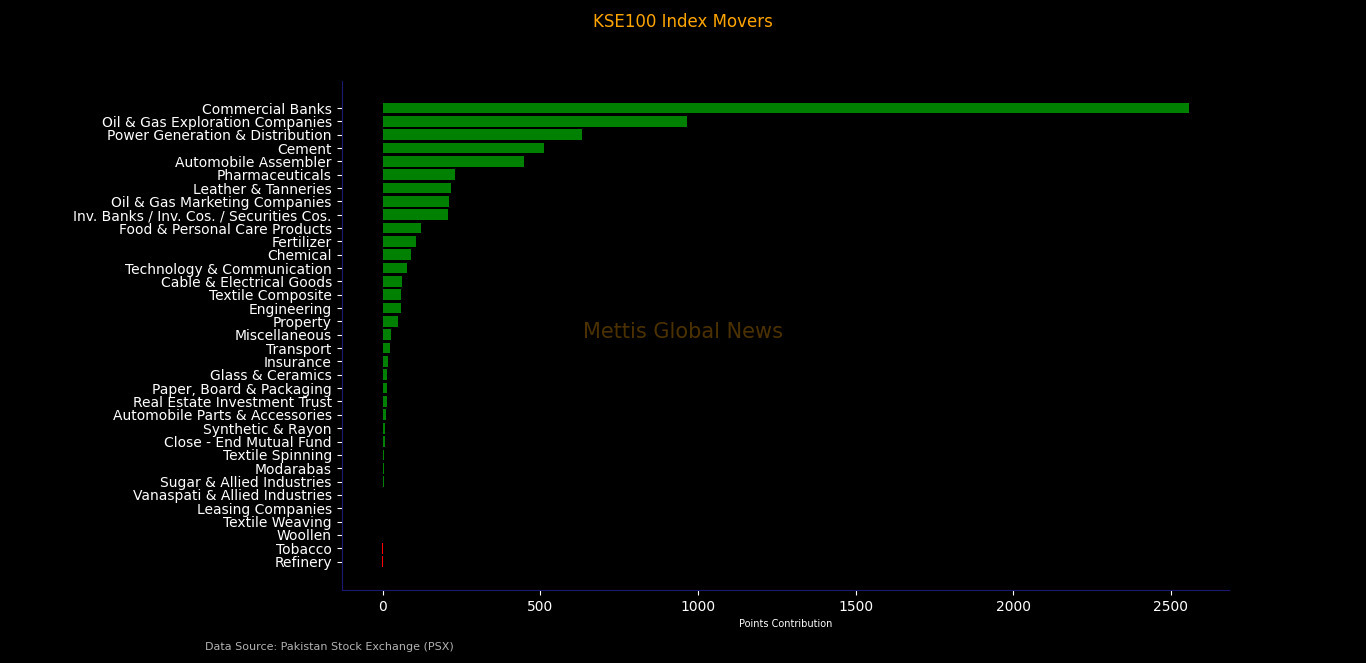

Index Movers

Sector-wise, commercial banks once again dominated

the upside, contributing 2,557.58 points to the index, driven by strong

institutional interest and attractive valuations.

Oil & gas exploration companies added 966.25 points,

supported by stable energy fundamentals, while power generation &

distribution contributed 631.04 points.

Cement (+512.89 points) and automobile assemblers (+448.69

points) also remained key contributors, reflecting improving expectations

around construction activity and auto demand recovery.

Other notable positive contributors included pharmaceuticals

(+230.90 points), oil & gas marketing companies (+210.91 points),

investment banks and securities companies (+207.27 points), fertilizer (+106.69

points).

Food & personal care products (+122.30 points),

and technology & communication (+76.87 points), highlighting

broad-based participation.

On the downside, refinery (-2.39 points), tobacco (-2.38

points), and woollen (-0.08 points) remained the only lagging

sectors.

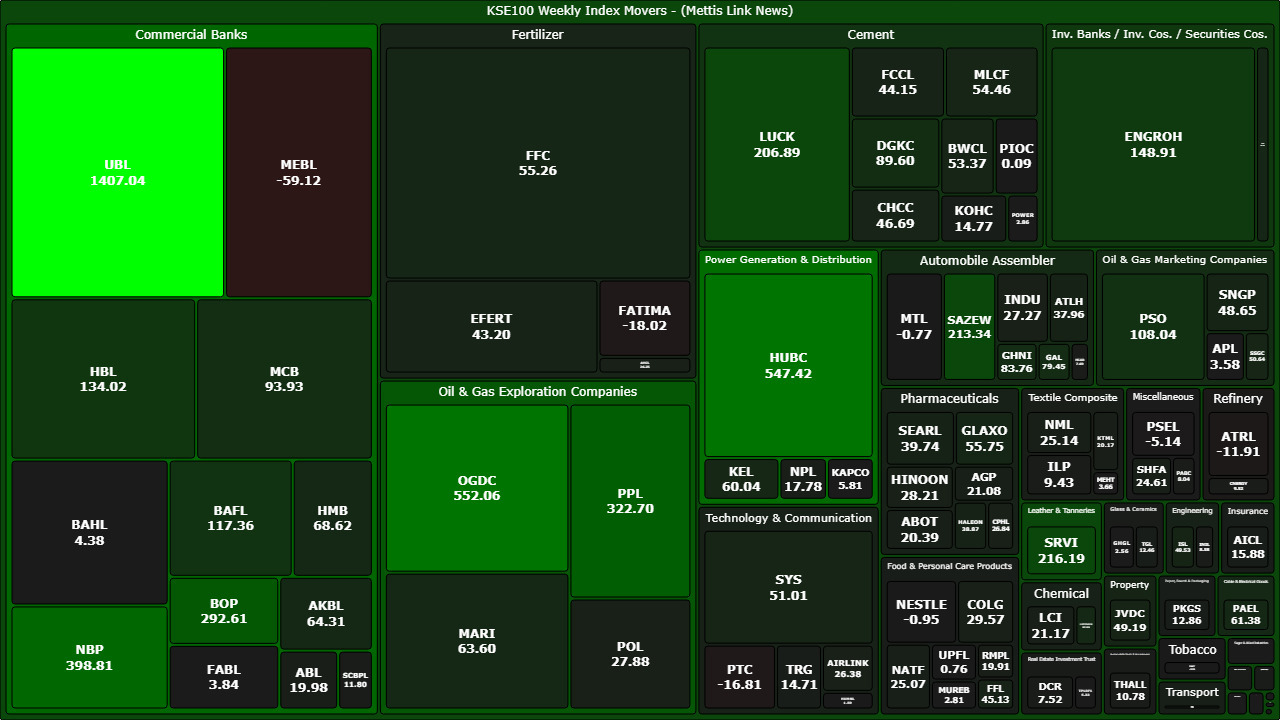

At the individual stock level, UBL led the

rally, contributing 1,407.04 points, followed by OGDC (+552.06

points) and HUBC (+547.42 points).

Other major contributors included NBP (+398.81 points),

PPL (+322.70 points), and BOP (+292.61 points), reinforcing the

dominance of banking and energy stocks.

Key support also came from SRVI, SAZEW, LUCK, ENGROH,

HBL, BAFL, PSO, MCB, and DGKC, alongside notable contributions from GHNI,

GAL, MARI, SYS, PAEL, KEL, and PSX, indicating strong participation across

cyclical and growth sectors.

Additional gains were witnessed in GLAXO, FFC, MLCF,

BWCL, SSGC, ISL, JVDC, SNGP, FCCL, EFERT, SEARL, HALEON, and ATLH, further

confirming the breadth of the rally.

On the losing side, MEBL (-59.12 points), FATIMA

(-18.02 points), PTC (-16.81 points), and ATRL (-11.91 points)

weighed marginally on the index.

FIPI / LIPI

Foreign investment flows turned positive this week.

Under Foreign Institutional Portfolio Investment (FIPI), foreign investors

recorded a net inflow of Rs780.08m ($2.80m).

Foreign corporates remained net sellers with an outflow of Rs1.12bn,

while overseas Pakistanis provided strong support with net buying of Rs1.87bn

($6.70m). Foreign individuals remained marginal buyers.

On the domestic side, Local Portfolio Investment (LIPI)

showed a net outflow of Rs780.08m ($2.80m), effectively mirroring

foreign inflows.

Among local participants, individuals (+Rs2.99bn), companies

(+Rs2.94bn), and mutual funds (+Rs2.58bn) emerged as key buyers,

supporting market momentum.

On the other hand, banks & DFIs (-Rs6.16bn) and insurance

companies (-Rs2.69bn) were the major sellers, along with some selling

pressure from other organizations.

In the debt market, banks & DFIs showed significant

participation with net inflows of Rs20.07bn, while insurance companies

and mutual funds recorded notable outflows._20260418090808689_a75f9c.jpeg)

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,065.00 | 64,680.00 62,605.00 | -1020.00 -1.59% |

| BRENT CRUDE | 78.59 | 79.80 77.28 | 2.58 3.39% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.89 | 75.08 72.61 | 2.48 3.47% |

| SUGAR #11 WORLD | 14.88 | 14.98 14.65 | 0.00 0.00% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|