Weekly Market Roundup

Nilam Bano | February 02, 2025 at 09:16 AM GMT+05:00

February 02, 2025 (MLN): The equity market started the week on a negative note, spending three sessions in the red due to rollover week, weaker-than-expected corporate earnings, and uncertainty surrounding a cautious SBP policy rate adjustment.

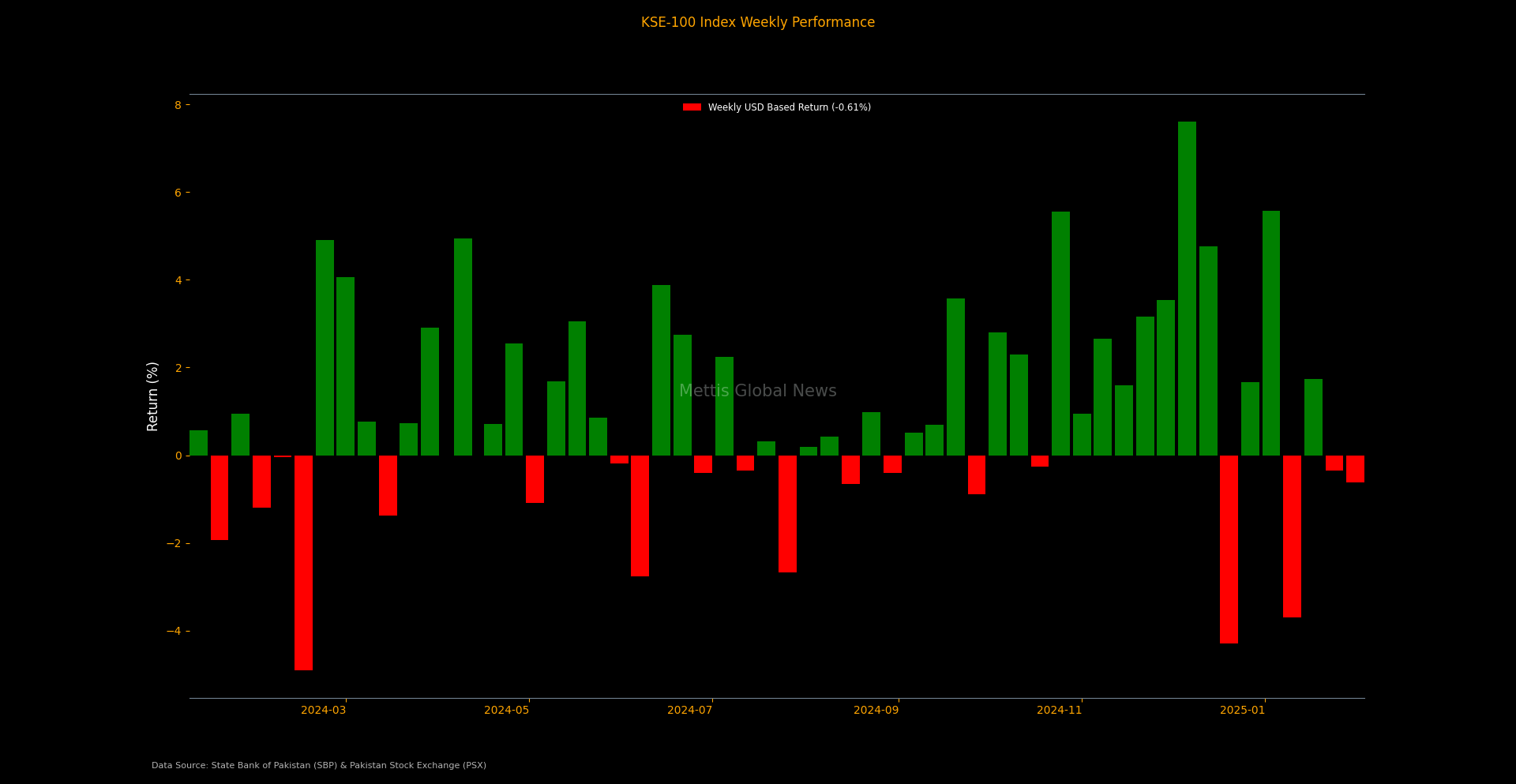

However, the market witnessed recovery in the last two sessions, leading the benchmark KSE-100 index to close at 114,255.72, down by 624.76 points or -0.54% compared to the previous week’s close of 114,880.48 points.

Intraday swings were significant, with the index reached a low of 11,1157.18 (-3,098.54 points) and a high of 115,596.87 (+1,341.15 points).

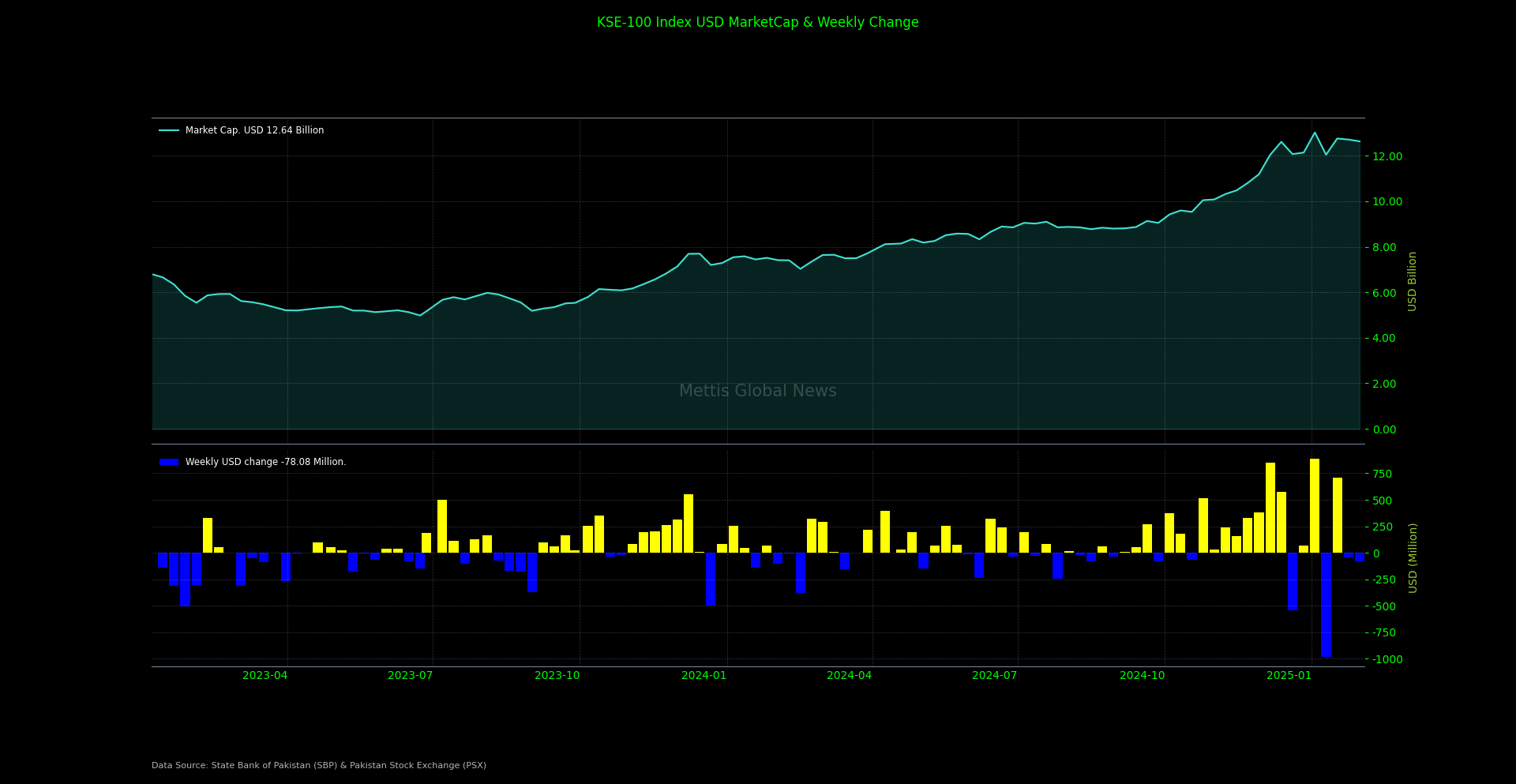

Market cap

The KSE-100 market capitalization stood at Rs3.52 trillion, down 0.54% from the previous week’s Rs3.54tr. In USD terms, the market cap was recorded at $12.63 billion, compared to $12.71bn in the prior week, reflecting a decline of $78 million or 0.61%.

This week, the index return in USD terms remained negative at -0.61%, compared to last week’s return of -0.35%.

On the first day of the outgoing week, the Central Bank reduced the policy rate by 100bps to 12% on the back of a continued disinflationary trend.

The SBP also revised the inflation forecast for FY25 to 5.5%-7.5%. Furthermore, the SBP adjusted its current account balance forecast for FY25 to a range of a 0.5% surplus to a 0.5% deficit of GDP.

The Central Directorate of National Savings (CDNS) once again reduced profit rates today across most of its savings schemes, with the Savings Account (SA) seeing the steepest cut of 200 basis points (bps), bringing it down from 13.50% to 11.50%, effective from January 31, 2025.

The foreign exchange reserves held by the Central Bank decreased by $76.3m or 0.67% WoW to $11.37 billion during the week ended on January 24, 2025.

On the upside, the Power Division issued a special directive to all electricity distribution companies, including Karachi Electric, regarding the execution of exclusive service-level agreements (SLAs) with industries that have captive power generation.

The positive economic cues helped stabilize investor sentiment, pushing the KSE-100 index’s fiscal year-to-date returns to 45.65%.

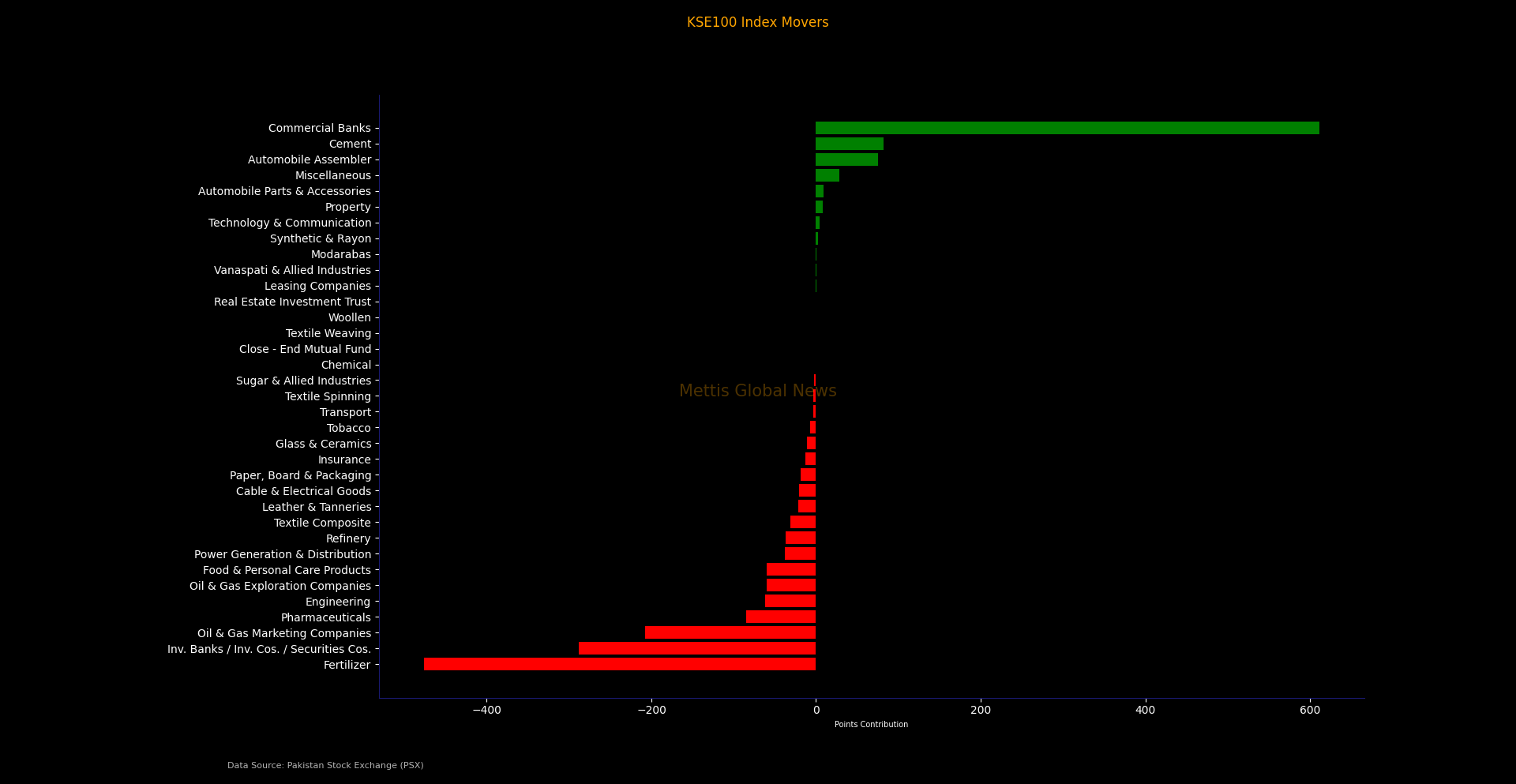

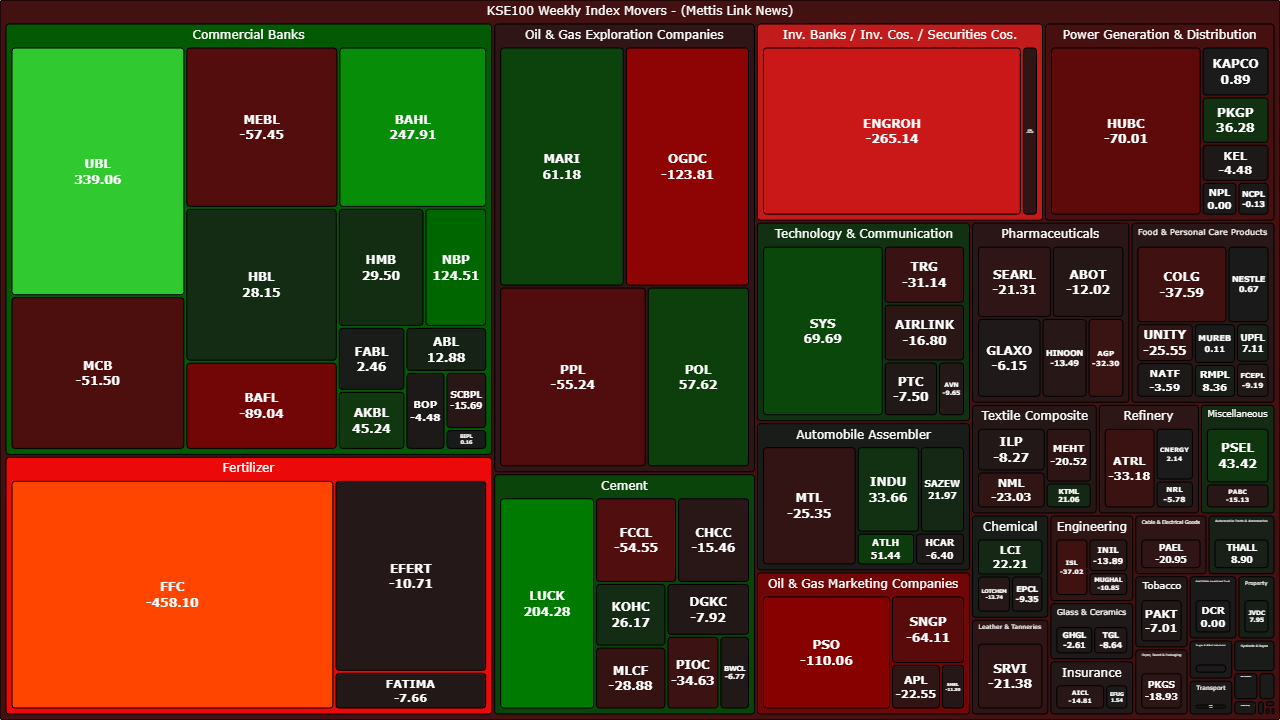

Top Index Movers

During the week, Fertilizer, Investment Banks, Oil & Gas Marketing Companies, and Pharmaceuticals dragged the index down by -476.46, -288.21, -208.02, and -85.26, respectively.

On the flip side, Commercial Banks, Cement, and Automobile Assembler contributed 611.72, 82.23, and 75.32, respectively to the index.

Among individual stocks, FFC eroded -458.09 points from the index while ENGROH, OGDC, and PSO dented the index by -265.14, -123.80, and -110.05, respectively.

Conversely, UBL, BAHL, LUCK, and NBP added 339.06, 247.91, 204.27 and 124.50, respectively.

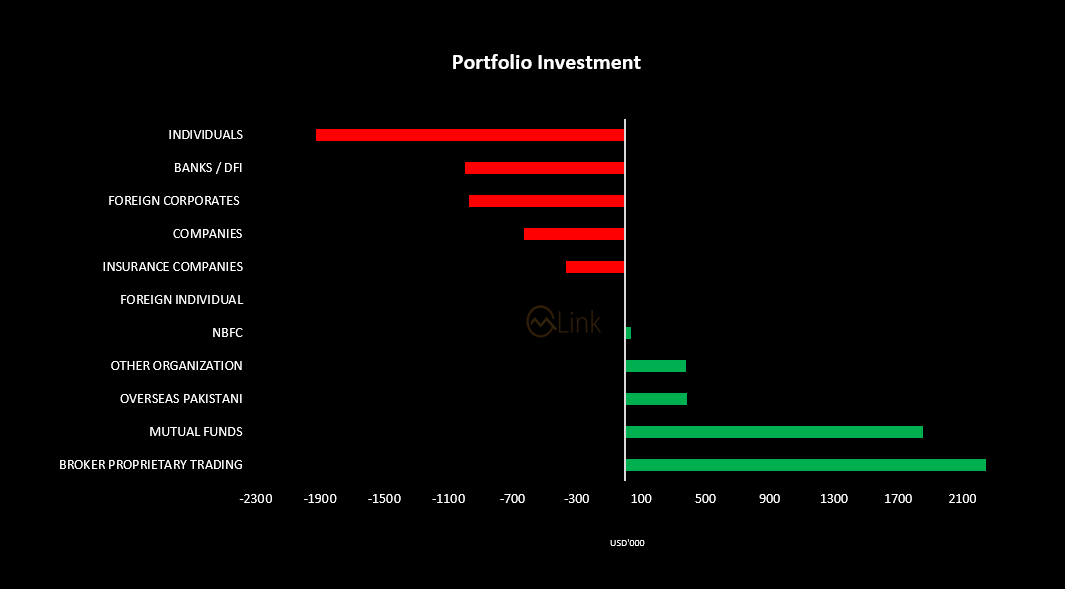

FIPI/LIPI

This week, foreign investors emerged as net sellers, offloading the equities worth $586.56 thousand.

Among them, foreign corporates led the selling activity worth $974.22 thousand while overseas Pakistanis purchased securities worth $386.72 thousand.

On the other hand, this week, local investors were net buyers, purchasing equities worth $586.56 thousand.

Among them, broker proprietary trading and mutual funds bought securities worth $2.24m and $1.85m, respectively.

However, individuals, banks/DFIs and companies sold securities worth $1.92m, $998.85 thousand and $632.23 thousand, respectively.

Copyright Mettis Link News

Related News

_20260303092753200_b3e945.webp?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 157,132.10 429.92M | 3.39% 5159.10 |

| ALLSHR | 93,566.86 763.32M | 2.62% 2388.00 |

| KSE30 | 48,302.97 218.66M | 4.27% 1976.50 |

| KMI30 | 220,798.52 207.58M | 4.07% 8628.34 |

| KMIALLSHR | 59,988.53 433.51M | 2.75% 1606.15 |

| BKTi | 46,193.08 61.76M | 4.26% 1887.06 |

| OGTi | 30,193.10 21.94M | 3.73% 1086.31 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 68,555.00 | 69,740.00 66,385.00 | -925.00 -1.33% |

| BRENT CRUDE | 80.14 | 85.12 78.38 | 2.40 3.09% |

| RICHARDS BAY COAL MONTHLY | 99.40 | 0.00 0.00 | -7.85 -7.32% |

| ROTTERDAM COAL MONTHLY | 124.15 | 139.50 124.15 | 5.35 4.50% |

| USD RBD PALM OLEIN | 1,083.50 | 1,083.50 1,083.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.20 | 77.98 70.41 | 1.97 2.77% |

| SUGAR #11 WORLD | 13.95 | 14.20 13.91 | 0.04 0.29% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|