Weekly Market Roundup

Abdur Rahman | May 17, 2024 at 09:27 PM GMT+05:00

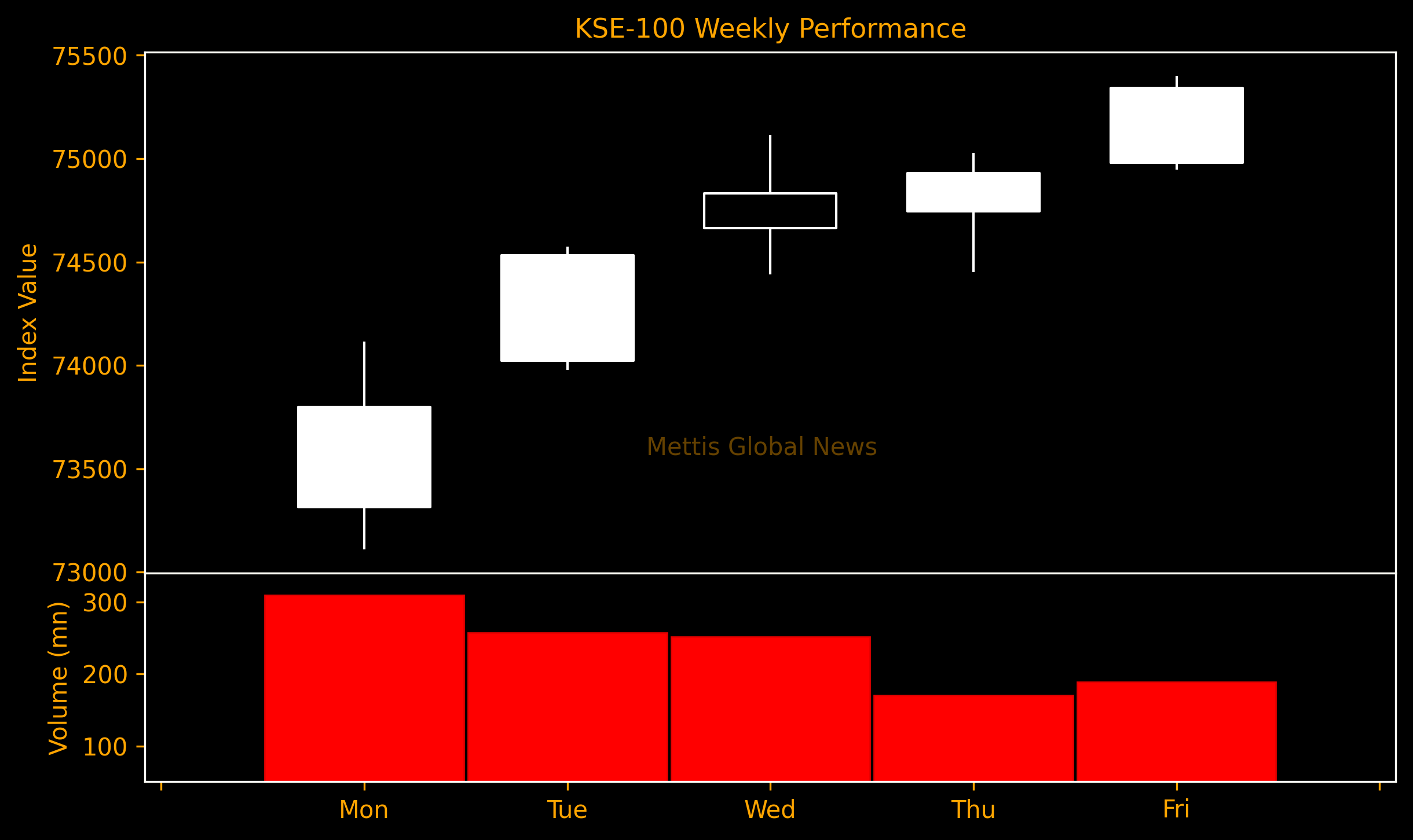

May 17, 2024 (MLN): Pakistan stock market's benchmark KSE-100 index continued to soar this week, jumping by another 2,257 points or 3.1% to close at a record high of 75,342.

On the currency front, the Pakistani Rupee recorded a marginal decline of 0.03% WoW.

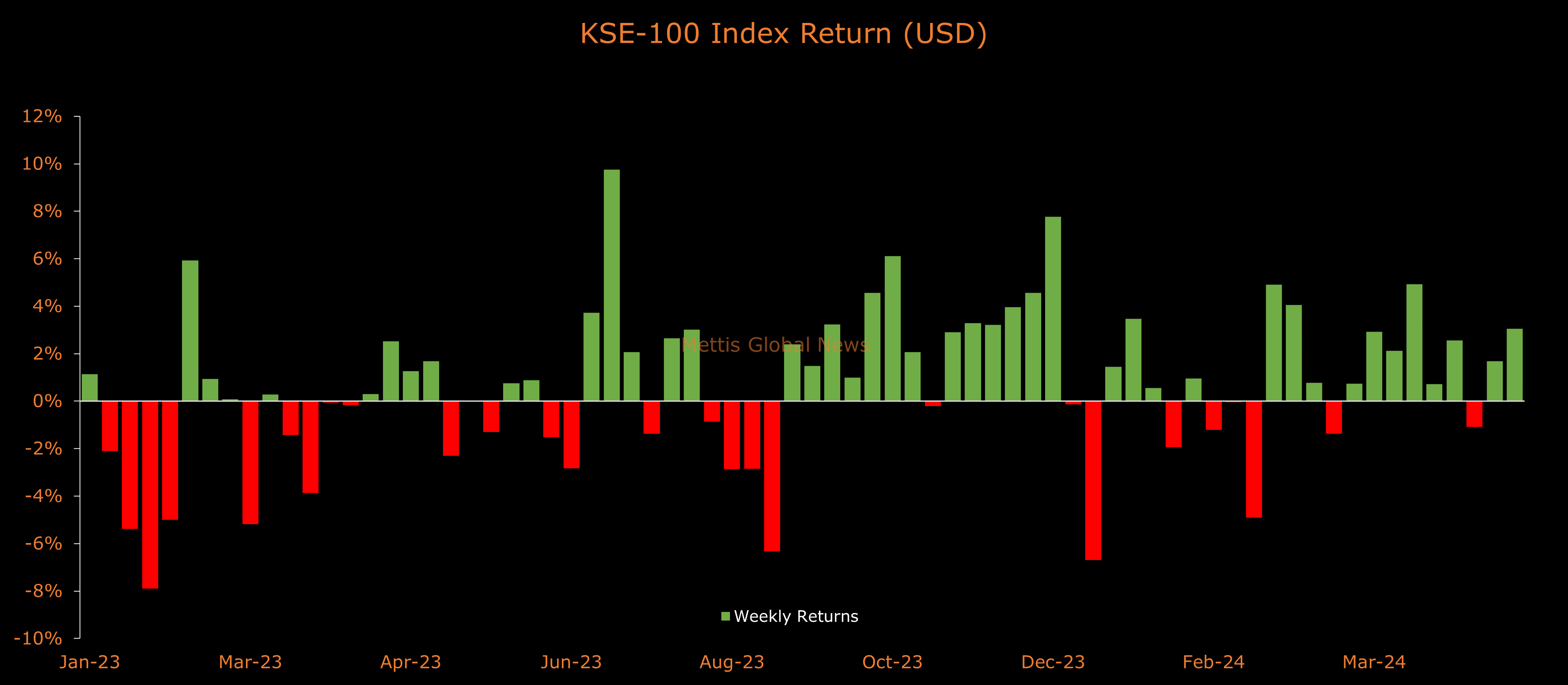

In USD terms, the KSE-100 index also gained 3.1% this week.

Throughout the week, KSE-100 traded in a range of 2,291 points, between a high of 75,401 (2,316) and a low of 73,110 (24) points.

PSX average traded volume was recorded at 554.51 million shares worth Rs21.93 billion, marking a decrease of 22.7% WoW in the number of shares and 10.4% WoW in traded value.

Meanwhile, the PSX market capitalization increased by $906.84m or 2.6% to $36.42bn over the week. In PKR terms, market capitalization stood at Rs10.13 trillion.

Pakistan stock market’s historic bull run—which started last year with International Monetary Fund (IMF) loan deal—has been further fueled amid strong foreign buying spree, renewed bets for interest rate cuts due to improvement in economic conditions, and official talks for a new IMF program.

Read: PSX continues historic bull run as foreign investors flock to Pakistan

On the economic front, the country posted another current account surplus of $491 million, largely due to a significant increase in workers' remittances.

Moreover, it attracted $359m FDI in April 2024, highest in over 4 years.

Economic growth is showing signs of recovery while inflation is trending downward.

The weekly inflation fell for the fifth consecutive week. Accordingly, the CPI-based inflation for May is expected to fall to about 13-14% YoY, expanding real interest rates to 8-9%.

The government conducted two auctions during the week, picking up Rs639.5bn through MTBs at lower yields, and Rs458.5bn through PIB-PFL auction.

The central bank decreased the cut-off yields for the 12-month T-Bills by 49 basis points, further boosting rate cut hopes in June's meeting.

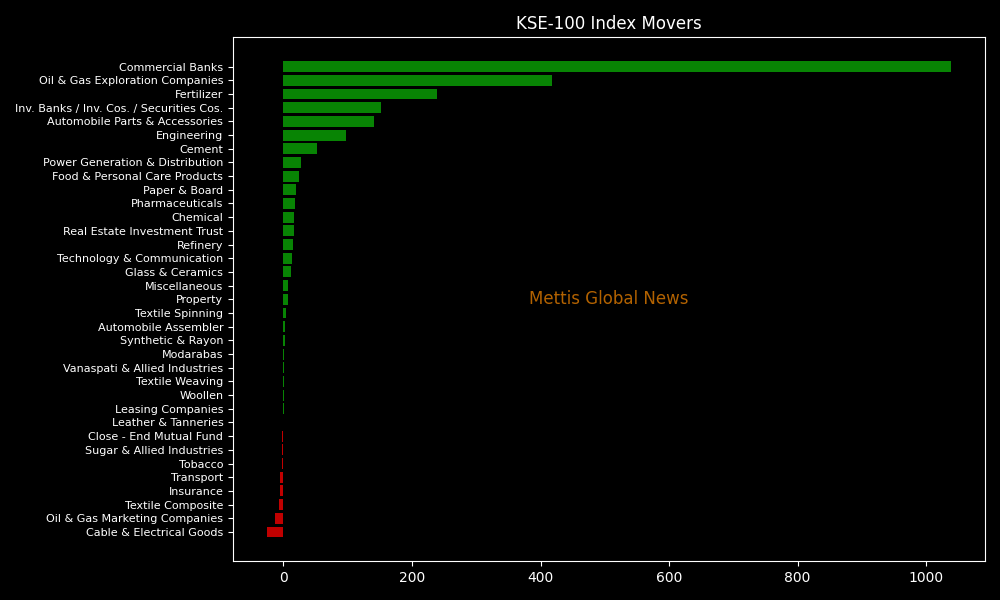

Top Index Movers

Sector-wise, top positive contributors were Commercial Banks (1,038pts), Oil & Gas Exploration Companies (417pts), Fertilizer (239pts), Inv. Banks / Inv. Cos. / Securities Cos. (152pts), and Automobile Parts & Accessories (141pts).

Contrary to that, negative contributions came from Cable & Electrical Goods (25pts), Oil & Gas Marketing Companies (13pts), Textile Composite, (8pts), Insurance (6pts), and Transport (5pts).

The best-performing stocks during the week were UBL (295pts), POL (202pts), MCB (174pts), EFERT (174pts), and MEBL (173pts).

Whereas, TRG, PAEL, KEL, PSO, and FCCL collectively took away 101 points from the index.

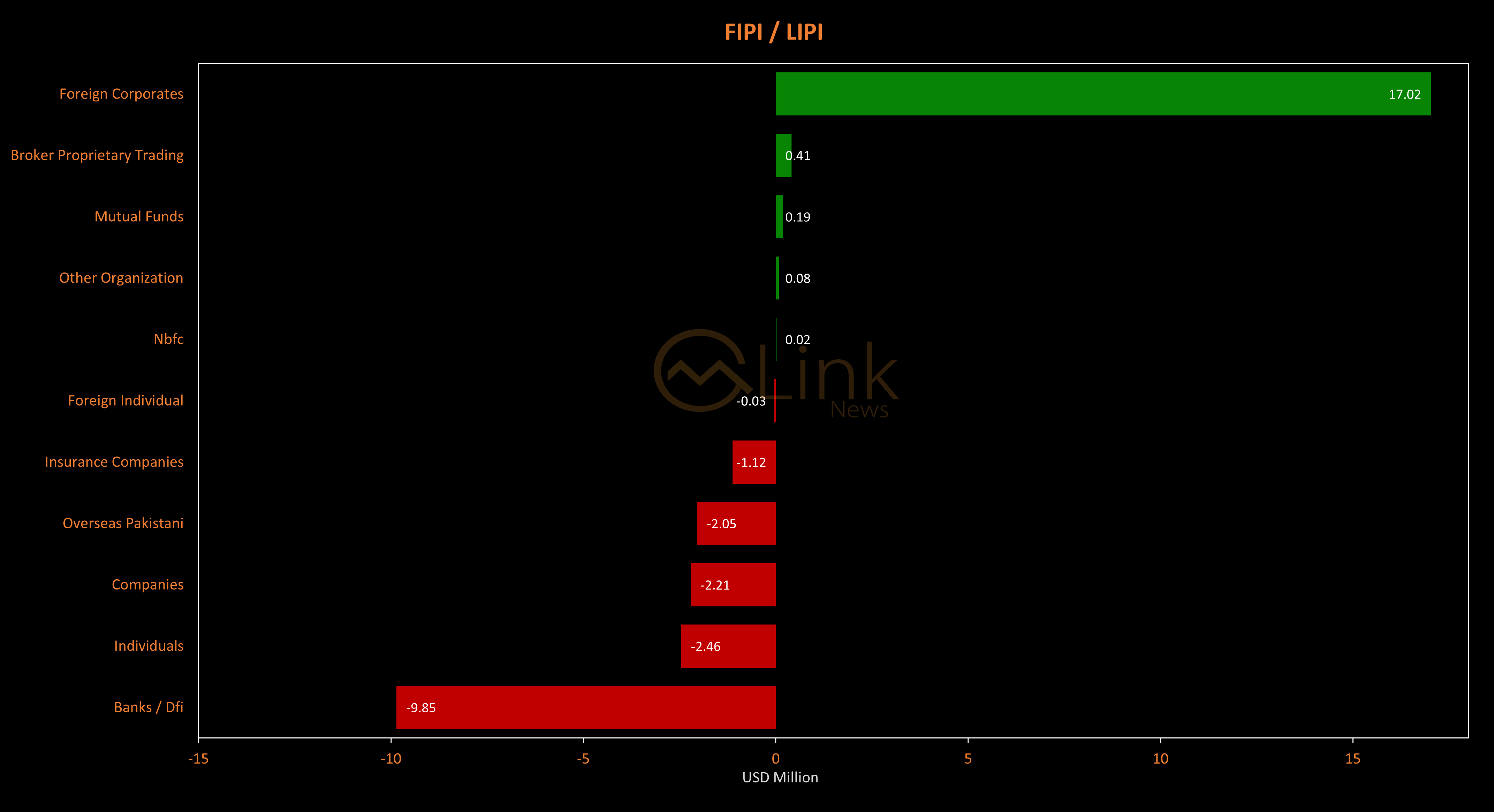

FIPI/LIPI

Foreign investors were net buyers during the week, acquiring a significant $14.94m worth of equities.

Flow-wise, Foreign corporations were the dominant buyers, with a net investment of $17m.

They allocated the majority of their capital, $7.79m, to Commercial Banks, while divesting from All other Sectors sector, amounting to $1.06m in sales.

On the other hand, the leading sellers were Banks / Dfi, with a net sale of $9.85m.

Their most substantial sales activity was in Commercial Banks, amounting to $6.18m, while they acquired $1.28m of equities in All other Sectors.

To note, the 100-index has gained 33,890 points or 81.76% during the fiscal year, whereas the ongoing calendar year has witnessed a cumulative increase of 12,891 points, equivalent to 20.64%.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 134,299.77 290.06M |

0.39% 517.42 |

| ALLSHR | 84,018.16 764.12M |

0.48% 402.35 |

| KSE30 | 40,814.29 132.59M |

0.33% 132.52 |

| KMI30 | 192,589.16 116.24M |

0.49% 948.28 |

| KMIALLSHR | 56,072.25 387.69M |

0.32% 180.74 |

| BKTi | 36,971.75 19.46M |

-0.05% -16.94 |

| OGTi | 28,240.28 6.19M |

0.21% 58.78 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 118,140.00 | 119,450.00 115,635.00 |

4270.00 3.75% |

| BRENT CRUDE | 70.63 | 70.71 68.55 |

1.99 2.90% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

1.10 1.14% |

| ROTTERDAM COAL MONTHLY | 108.75 | 108.75 108.75 |

0.40 0.37% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.75 | 68.77 66.50 |

2.18 3.27% |

| SUGAR #11 WORLD | 16.56 | 16.60 16.20 |

0.30 1.85% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|