PSX in Jan: Chasing Stars, Stumbling at Finish

Nilam Bano | February 03, 2025 at 01:10 PM GMT+05:00

February 03, 2025 (MLN): Scaling new heights but stumbling at the finish line, the KSE-100 index posted an impressive 84% YoY return in January 2025. However, despite hitting an all-time high of 118,735 on January 06, 2025, the benchmark remained range-bound and closed the month at 114,255.72, marking a 0.76% decline from December 2024.

This dip was mainly driven by volatile sentiment due to uncertainty over the upcoming IMF review amid a revenue shortfall and slow progress on key benchmarks, lower-than-expected inflows and persistent domestic and geopolitical uncertainties.

Intraday swings were significant, with the index reached a low of 111,157.19 (-3,098.53 points) and a high of 118,735.1 (+4,479.38 points).

.jpeg)

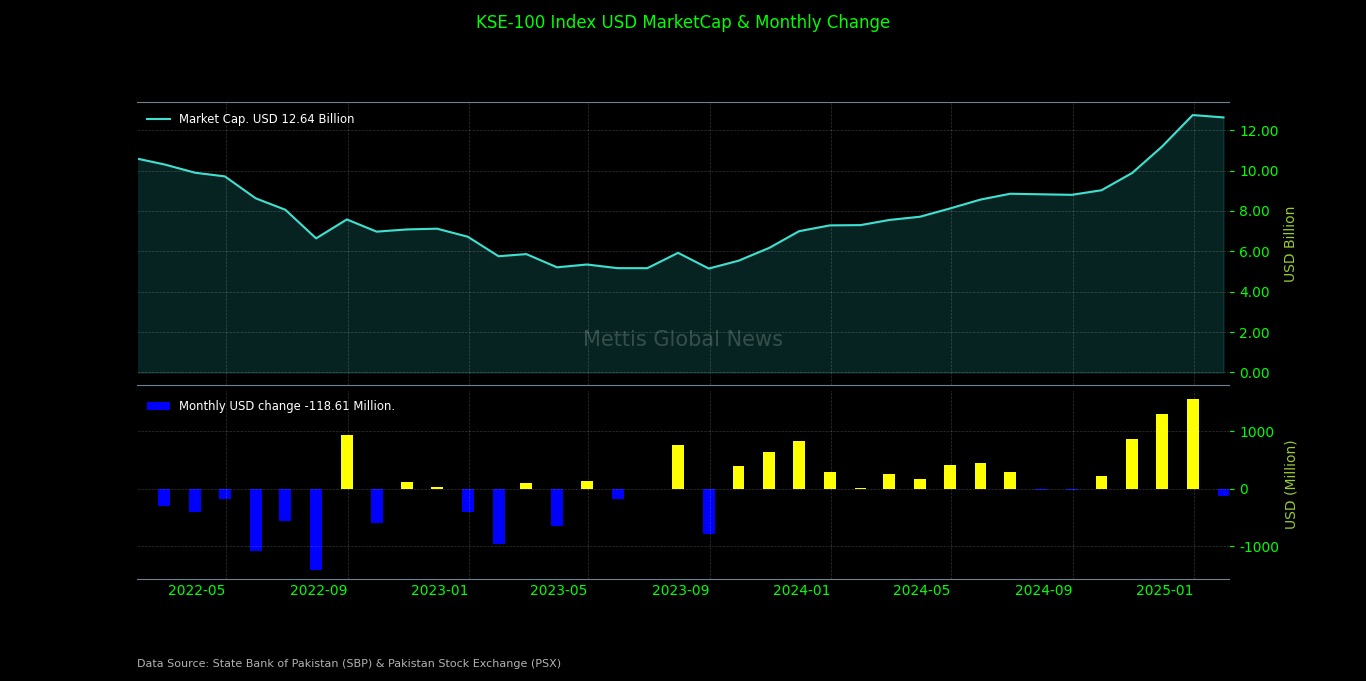

Market cap

The KSE-100 market capitalization stood at Rs3.52 trillion, down 0.78% from the previous month’s Rs3.55tr while compared to January 2024, the market cap has surged by 72.72%.

In USD terms, the market cap was recorded at $12.63 billion, compared to $12.75bn in the prior month, reflecting a decline of $118 million or -0.93%. While when compared to the previous year, the market capitalization witnessed a notable jump of 73%.

This month, the index return in USD terms turned negative to -0.89%, compared to last month’s positive return of +13.38%.

.jpeg)

The performance of economic indicators kept the hope intact as the current account recorded a surplus of $582m in December 2024, bringing the 1HFY25 total to $1.2bn.

Pakistan’s Gross Domestic Product (GDP) posted a growth of 0.92% in the first quarter of FY2024-25 despite a -1.03% contraction in the industrial sector.

This growth was bolstered by positive contributions from agriculture (1.15%) and services (1.43%).

Inflation slowed to 4.1% in December compared to 4.9% in the last month and 29.7% YoY in December 2023. It is expected to decline further in January.

In a significant development, the United Arab Emirates (UAE) rollover two deposits, each worth $1 billion, placed with the SBP.

Initially set to mature in January 2025, these deposits will now be extended for an additional year.

During the month, the World Bank’s Board of Directors endorsed the first-ever 10-year Country Partnership Framework (CPF) for Pakistan.

The framework aims to promote inclusive and sustainable development by prioritizing human capital development.

Furthermore, the Pakistani Rupee (PKR) appreciated marginally by 0.14% MoM, closing at 278.95 per USD.

This stability is attributed mainly to robust remittances, current account surplus and foreign exchange reserves which played a crucial role in strengthening the rupee.

.jpeg)

In the last week of January, the Central Bank reduced the policy rate by 100bps to 12% on the back of a continued disinflationary trend.

The reduction was the sixth in a row, bringing the total decrease since June 2024 to 1,000bps as a slowdown in inflation gives policymakers room to continue monetary easing in a bid to spur growth.

Additionally, the SBP also revised the inflation forecast for FY25 to 5.5%-7.5%. Furthermore, the SBP adjusted its current account balance forecast for FY25 to a range of a 0.5% surplus to a 0.5% deficit of GDP.

The Central Directorate of National Savings (CDNS) once again reduced profit rates today across most of its savings schemes, with the Savings Account (SA) seeing the steepest cut of 200 basis points (bps), bringing it down from 13.50% to 11.50%, effective from January 31, 2025.

The foreign exchange reserves held by the Central Bank stood at $11.37 billion during the week ended on January 24, 2025.

Going forward, upcoming inflows from commercial banks and multilateral institutions will aid in bolstering foreign reserves, expected to stay above $13bn by June 2025.

On the upside, the Power Division issued a special directive to all electricity distribution companies, including Karachi Electric, regarding the execution of exclusive service-level agreements (SLAs) with industries that have captive power generation.

In addition, Saudi investors are taking interest in Reko Diq as Pakistan’s deal with Saudi Arabia for selling a stake in the copper and gold mining project controlled by Barrick Gold Corp. is being negotiated.

The Pakistani government hopes the deal will extend beyond exploration to include some of the downstream activities within the country.

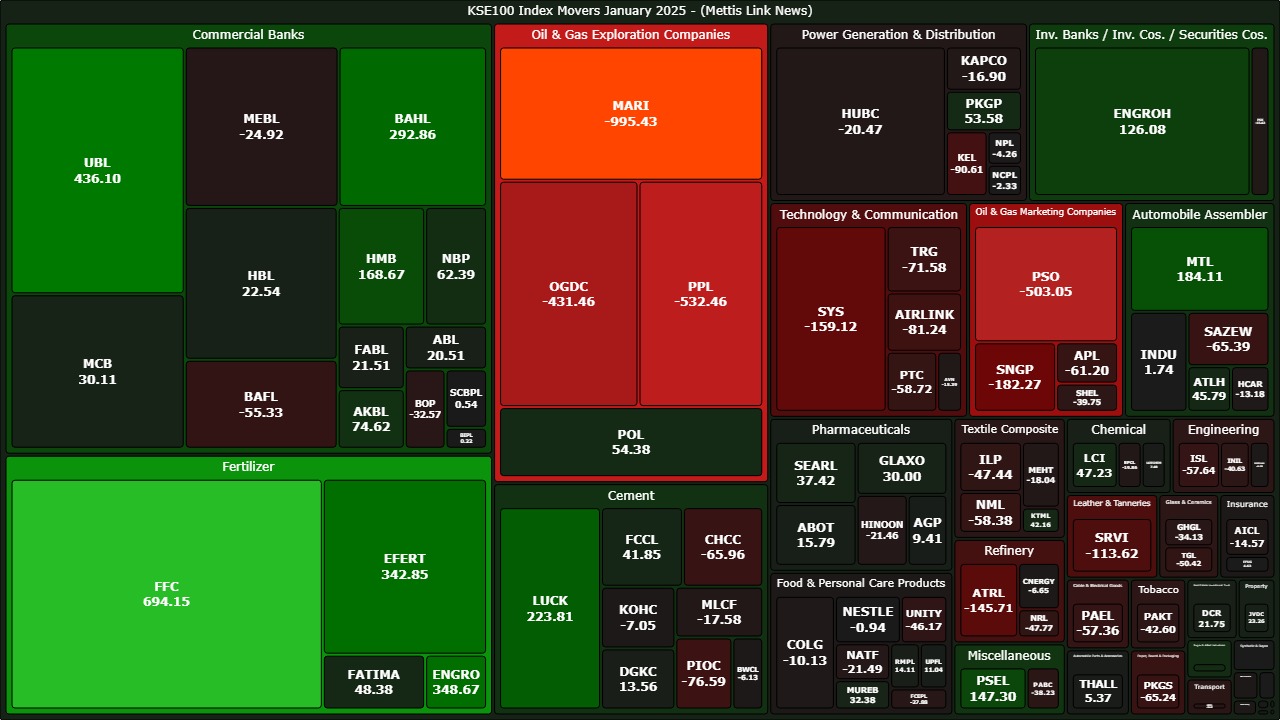

Top Index Movers

During the month, Oil & Gas Exploration Companies, Oil & Gas Marketing Companies, Technology & Communication, and Refinery dragged the index down by -1,904.96, -786.26, -386.05, and -200.12, respectively.

On the flip side, Fertilizer, Commercial Banks, and Automobile Assembler contributed 1434.05, 1017.25, and 153.07, respectively to the index.

.jpeg)

Among individual stocks, MARI eroded -995.43 points from the index while PPL, PSO, OGDC, and SNGP dented the index by -532.45, -503.04, -431.45 and -182.26, respectively.

Conversely, FFC, UBL, ENGRO, and EFERT added 694.15, 436.09, 348.67, and 342.85, respectively.

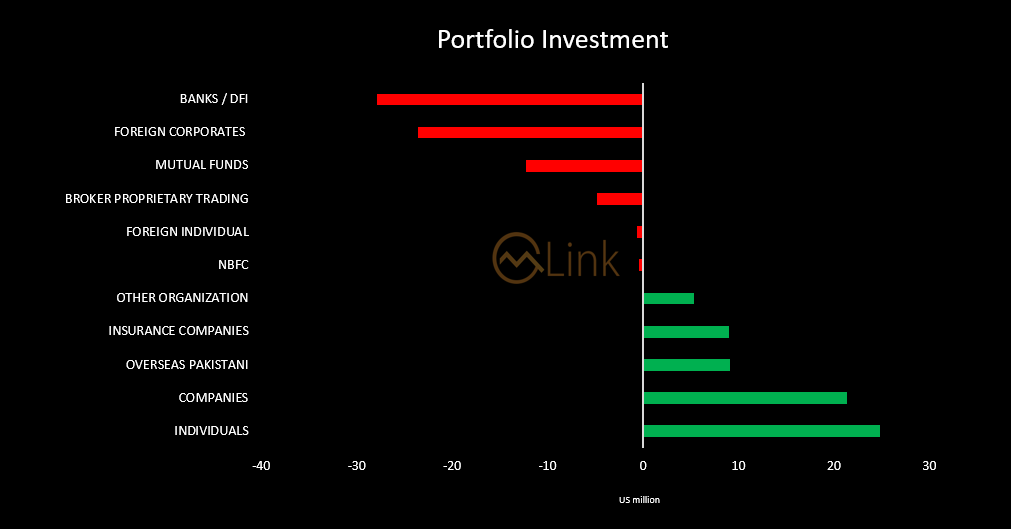

FIPI/LIPI

This month, foreign investors emerged as net sellers, offloading the equities worth $15.16m.

Among them, foreign corporations led this activity by selling securities worth $23.6m while overseas Pakistanis purchased securities worth $9.13m.

On the other hand, local investors were net buyers, purchasing equities worth $15.16m.

Among them, individuals and companies bought securities worth $24.84m and $21.33m, respectively.

However, banks/DFIs and mutual funds sold securities worth $27.93m, and $12.23m, respectively.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 155,783.90 29.55M | 6.35% 9303.75 |

| ALLSHR | 93,357.66 43.65M | 5.61% 4956.51 |

| KSE30 | 48,026.10 14.50M | 6.73% 3029.59 |

| KMI30 | 224,812.64 14.05M | 7.03% 14773.23 |

| KMIALLSHR | 60,624.62 26.71M | 5.77% 3308.90 |

| BKTi | 45,037.10 5.56M | 6.31% 2672.60 |

| OGTi | 33,251.07 1.68M | 5.62% 1770.59 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 69,940.00 | 70,765.00 68,485.00 | 735.00 1.06% |

| BRENT CRUDE | 94.42 | 95.04 88.05 | -4.54 -4.59% |

| RICHARDS BAY COAL MONTHLY | 99.40 | 0.00 0.00 | -13.60 -12.04% |

| ROTTERDAM COAL MONTHLY | 132.00 | 134.20 132.00 | 5.05 3.98% |

| USD RBD PALM OLEIN | 1,083.50 | 1,083.50 1,083.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.60 | 91.48 84.43 | -4.17 -4.40% |

| SUGAR #11 WORLD | 14.62 | 14.64 14.25 | 0.52 3.69% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|