PSX FY24 Review: A Year for the History Books

Abdur Rahman | June 28, 2024 at 05:41 PM GMT+05:00

June 28, 2024 (MLN): The Pakistan stock market recorded its best yearly return in over two decades, driven by optimism over improved economic conditions, enticing valuations, and the central bank's shift to monetary easing.

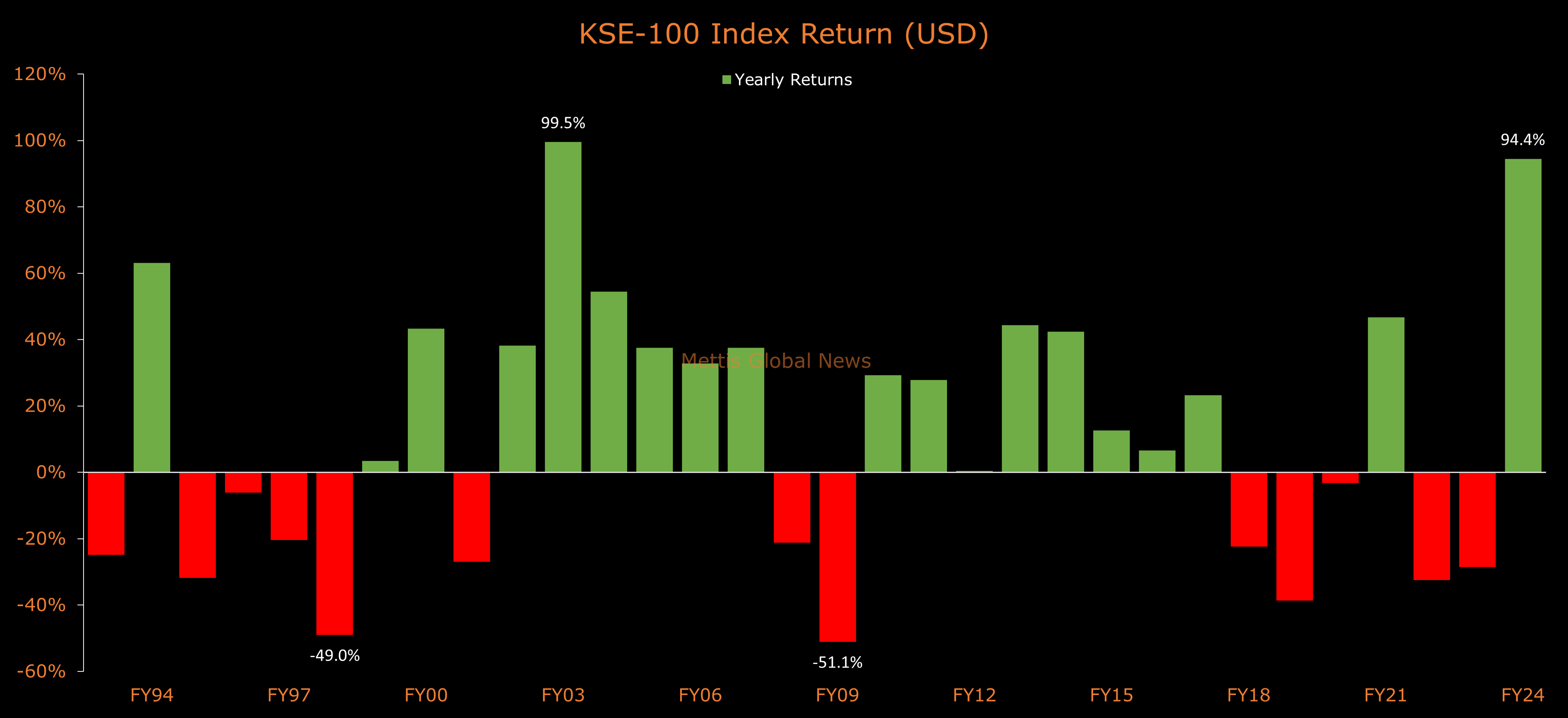

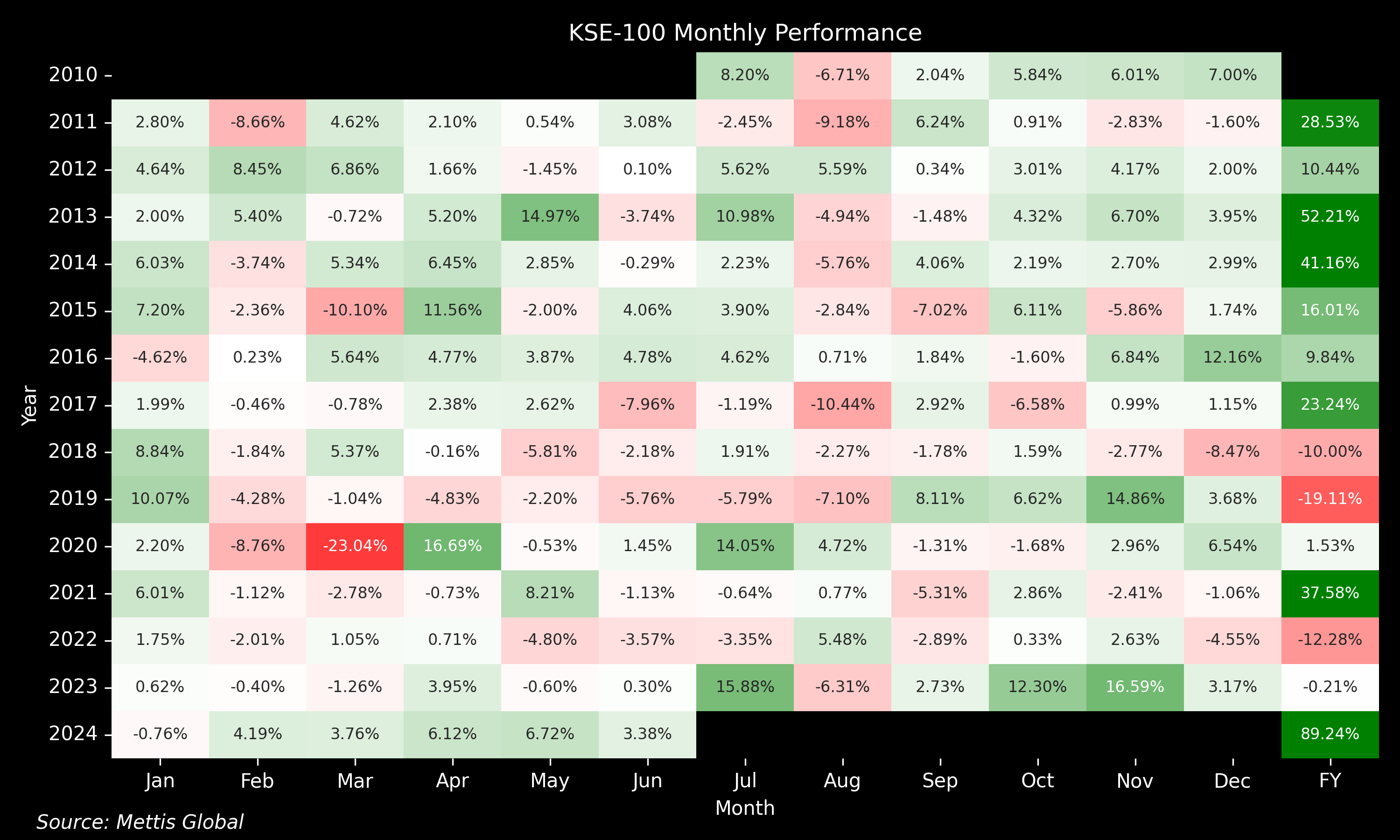

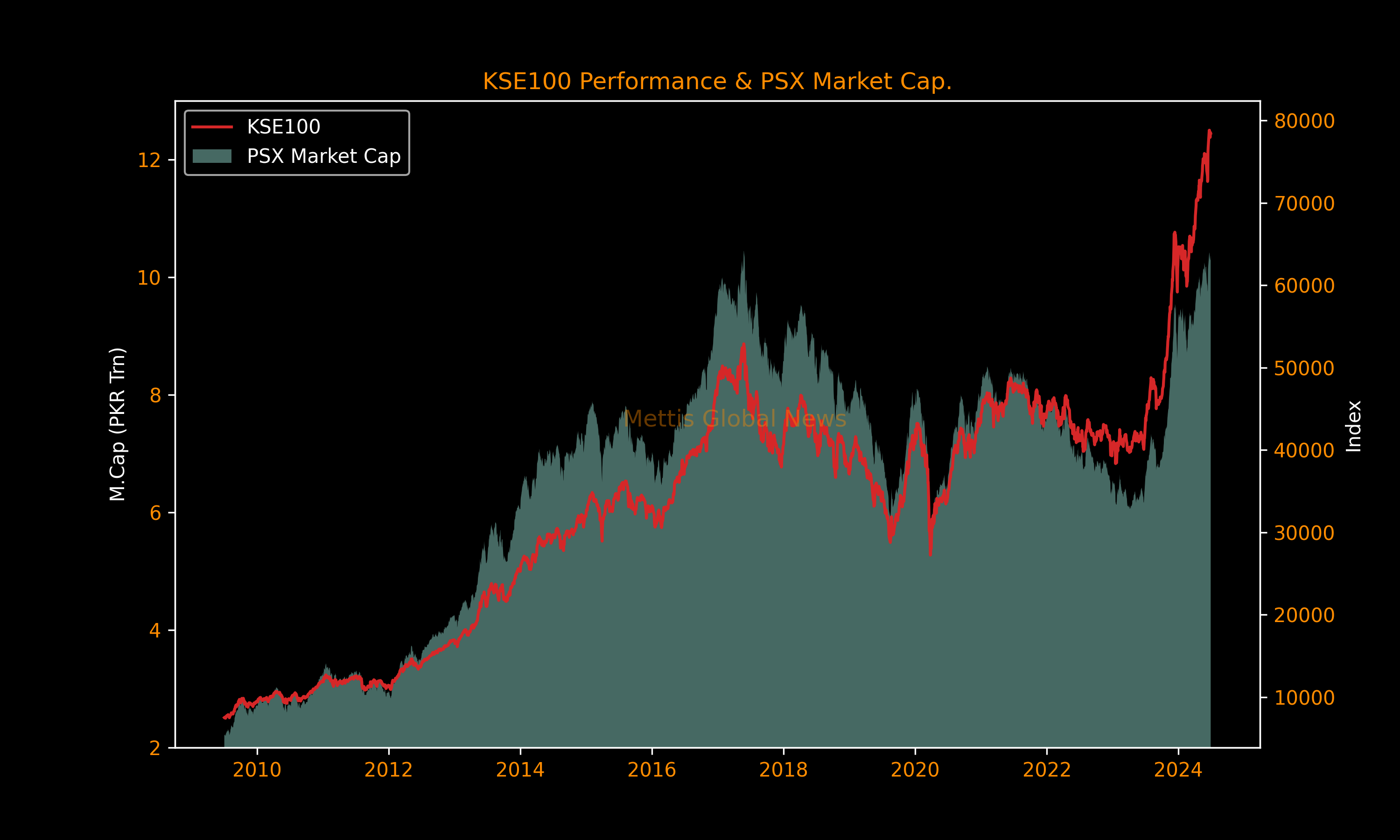

The KSE-100 Index climbed 89.2% or 36,992 points to 78,444.9 in fiscal year ending June 2024 to post its biggest yearly gain since FY 2003.

In USD terms, the gauge climbed 94.4% to become the best-performing market among more than 80 global equity indexes tracked by MG Link.

The historic bull run began when the country narrowly avoided a sovereign debt default, thanks to the International Monetary Fund’s rescue package toward the end of the last fiscal year.

The IMF's $3 billion loan program also helped unlock multilateral and bilateral funding, boosting the country's forex reserves by 99% to $8.9 billion.

The benchmark index in November 2023 hit its first record high in seven years, and continued to set new highs without significant pullbacks throughout the year.

The market participation also remained heightened in FY24, with the average traded volume of PSX surging 140% to 460.9 million shares.

Traded value in PKR terms rose 154% to Rs15.6bn. In USD terms, traded value was recorded at $55.2m, a gain of 118% compared to last year.

PSX Market capitalization rose 62.9% to a record Rs10.4 trillion. In USD terms, market capitalization surged 67.4% to $37.3bn. However, it is still down 62.6% from its 2017 high of $99.6bn.

Top & Bottom Performers

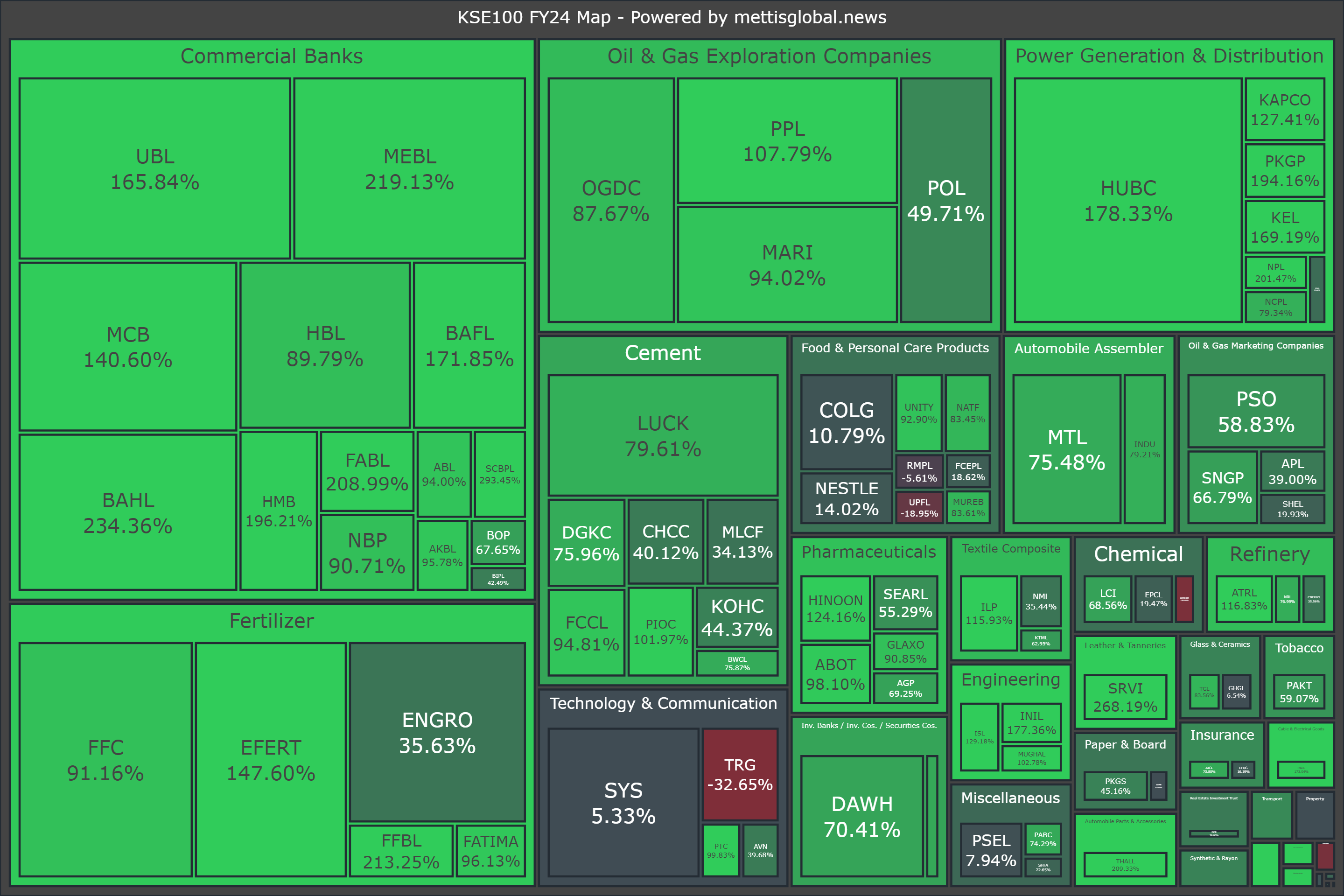

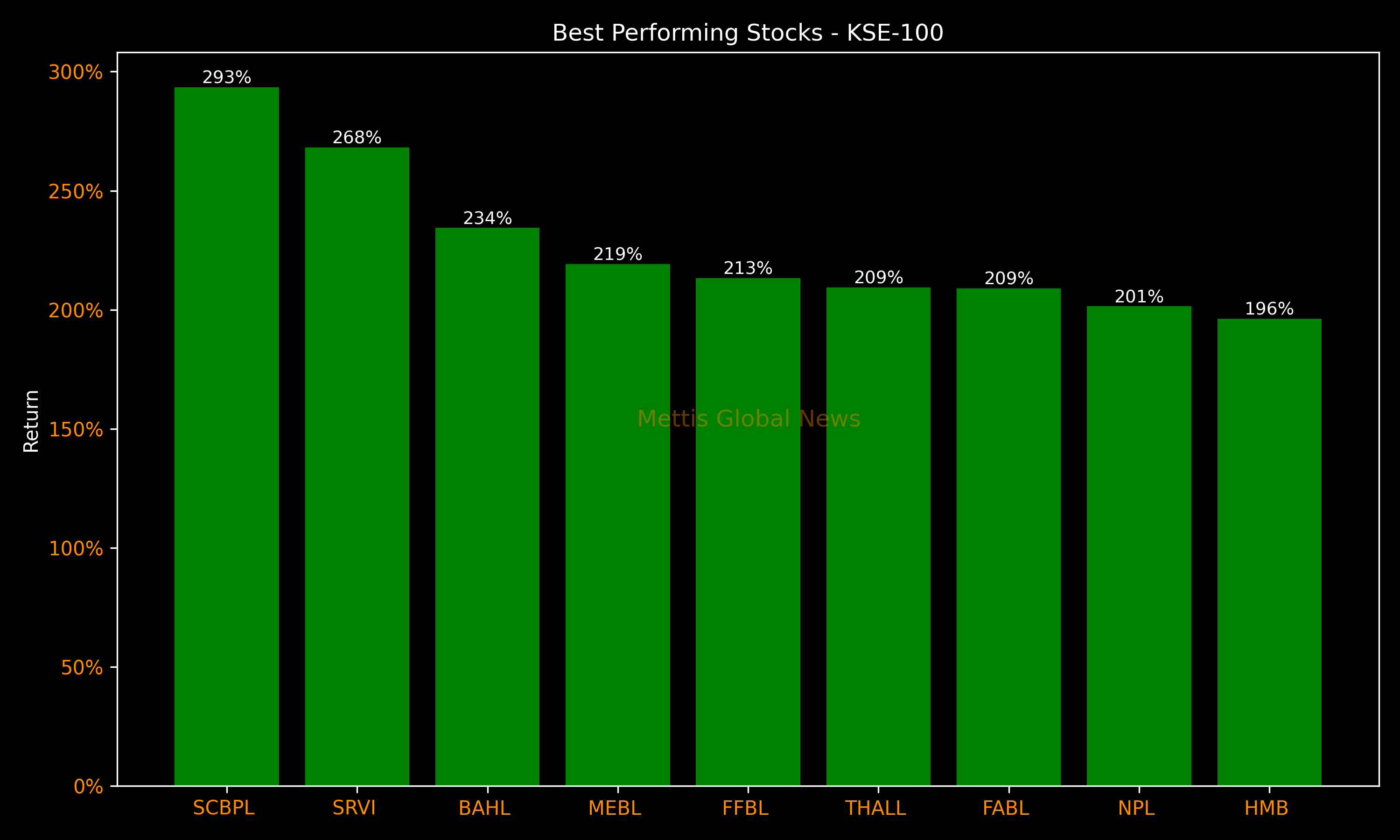

In percentage terms, the top-performing stocks during the year were SCBPL (+293%), SRVI (+268%), BAHL (+234%), MEBL (+219%), and FFBL (+213%).

Notably, three of the top five best-performing stocks were banks, as they benefited significantly from record-high interest rates of 22% for most of the year.

Meanwhile, Service Industries Limited (SRVI), one of the dark horse of the group, saw a remarkable 268% surge driven by the impressive performance of its tyre and tube segment, SLM.

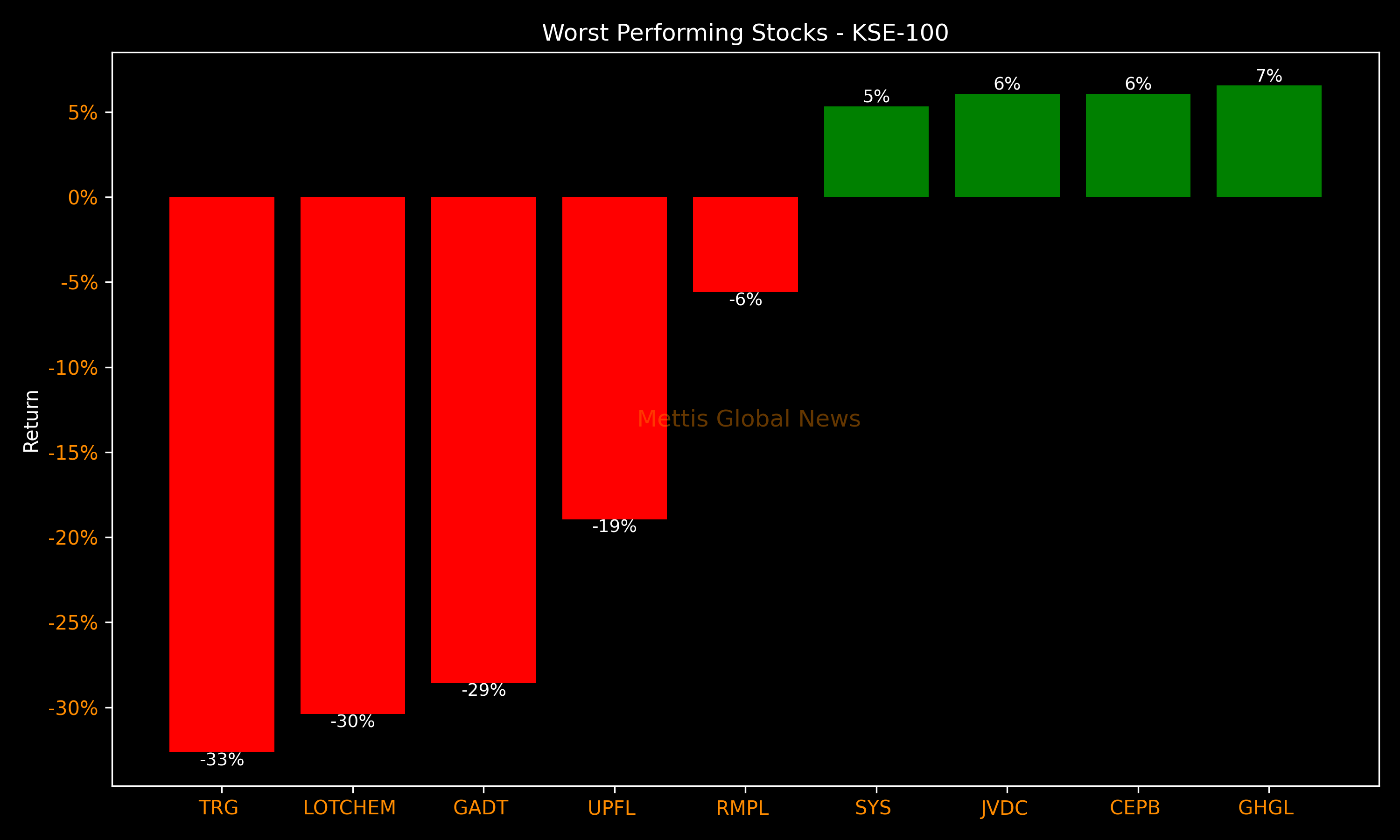

On the other hand, the worst-performing stocks during the year were TRG (-33%), LOTCHEM (-30%), GADT (-29%), UPFL (-19%), and RMPL (-6%).

Top Index Movers

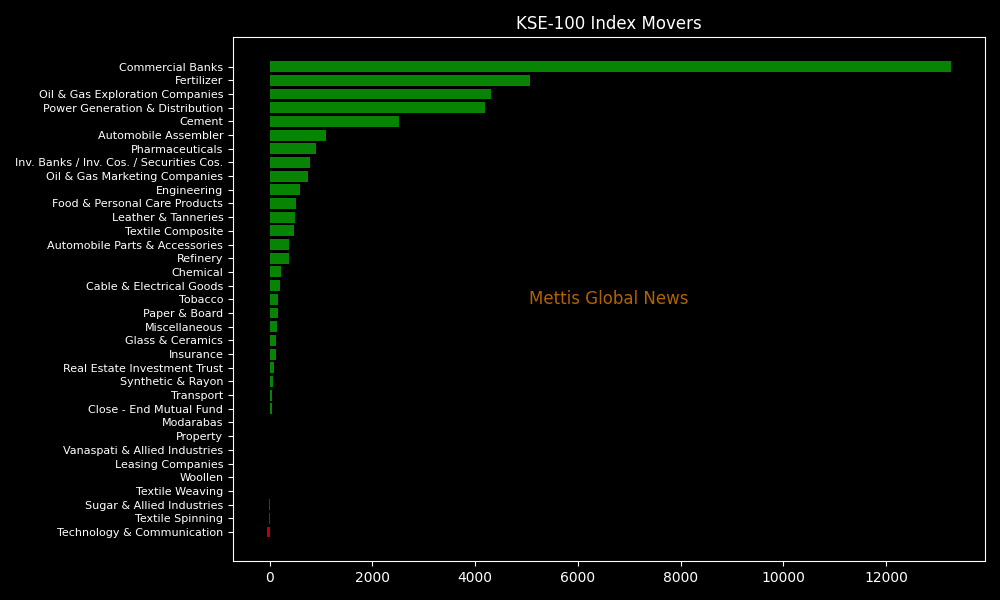

The banking sector, benefiting from high interest rates, along with cyclical sectors like energy, fertilizer, and cement, led the rally.

Commercial banks alone added a significant 13,265pts points to the index, standing out as the top performers of the rally.

The sector’s financial results have also justified this rally. Earnings per share for the sector rose a combined 18% in the first nine months of FY24 from a year earlier.

Other top performing sectors based on points added were Fertilizer (5,072pts), Oil & Gas Exploration Companies (4,301pts), Power Generation & Distribution (4,193pts), and Cement (2,508pts).

The only sectors that landed in the red zone were Technology & Communication (-52pts), Textile Spinning (-17pts), and Sugar & Allied Industries, (-8pts).

As for individual stock performance, the index's rally since July 2023 was largely driven by the megacap companies.

HUBC took the top spot with a significant gain of 3,282pts, fueled by its diversification strategy and attractive dividend yields.

Other top stocks based on points added included UBL (2,719pts), MEBL (2,394pts), EFERT (1,997pts), and BAHL (1,945pts).

Due to their heavy weighting in the KSE-100 Index, these five stocks accounted for 33% of the index's total return in FY24.

Meanwhile, the worst-performing stocks based on points snatched were TRG (-347pts), LOTCHEM (-55pts), UPFL (-41pts), HABSM (-20pts), and GADT (-17pts).

Portfolio Investment

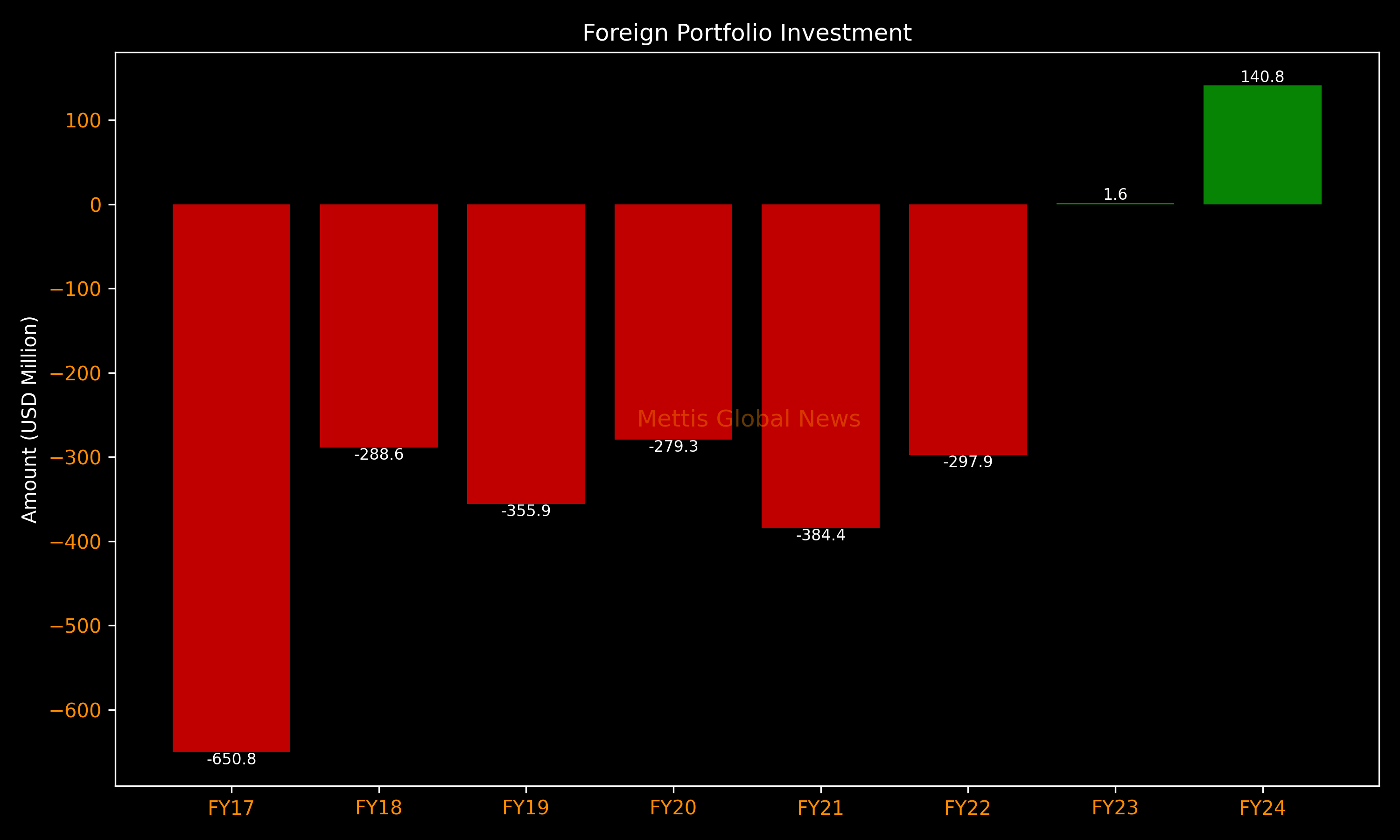

Foreign investors returned to Pakistani equities after almost a decade. Overseas investors purchased stocks worth a total of $140.8m in the fiscal year ending June 2024.

In the previous year, foreign investment stood at a meager $1.6m, while the five-year average was -$263.2m. From FY17 to FY23, foreign investors had dumped equities worth over $2.3 billion.

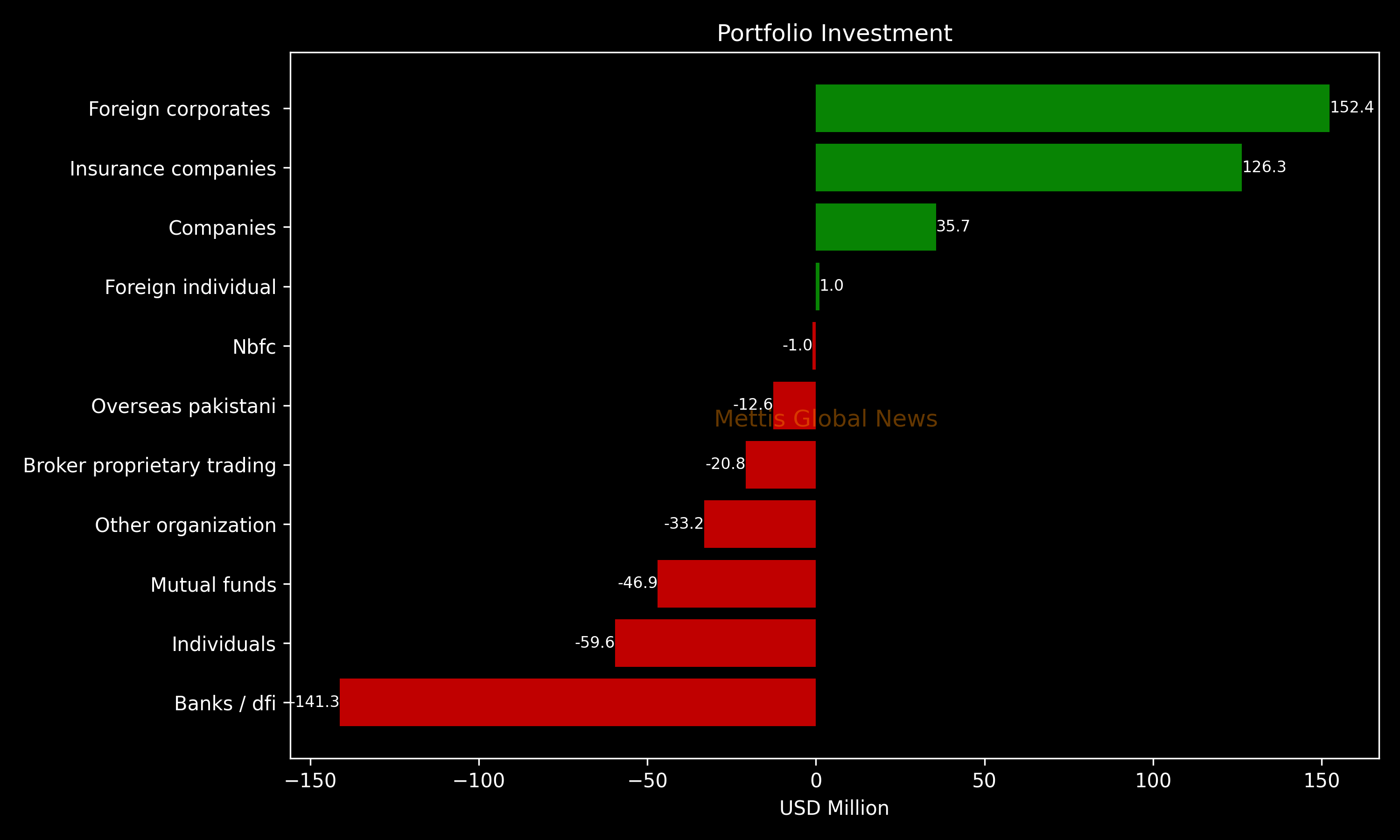

Flow-wise, Foreign Corporates were the dominant buyers, with a net investment of $152.4m.

They allocated the majority of their capital, $62.7m, to Commercial Banks, while divesting from the Debt Market sector, amounting to $16.6m in sales.

On the other hand, the leading sellers were Banks / Dfi, as they dumped stocks worth $141.3m.

Their most substantial sales activity was in Commercial Banks, amounting to $56.4m, while they acquired $8.5m of equities in the Debt Market.

Economic Indicators

Following a rough year, the economy has started to show signs of improvement.

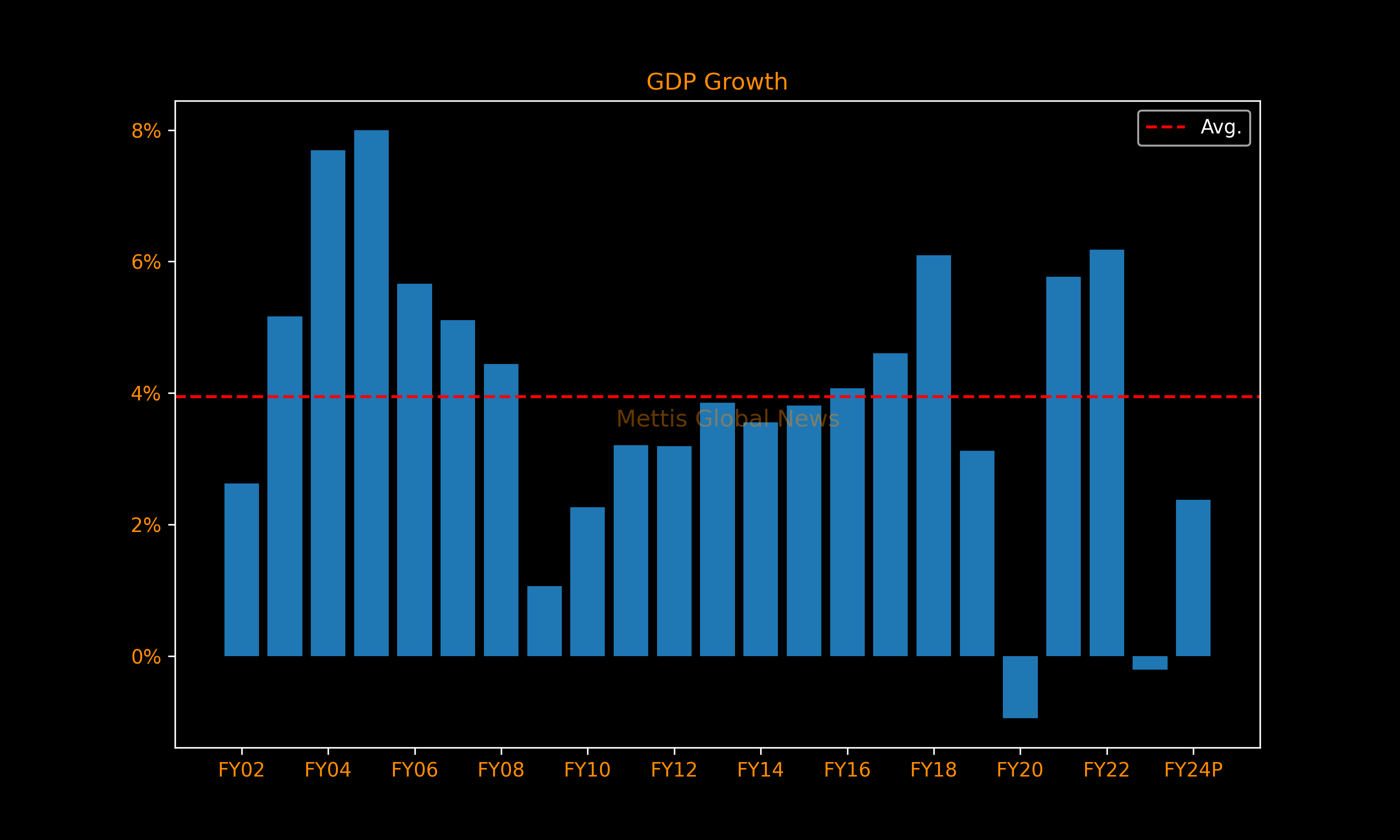

Pakistan’s real Gross Domestic Product (GDP) growth rate witnessed a modest recovery in FY24.

The country’s economy grew 2.38% in the fiscal year 2023-24 against a contraction of 0.21% in the previous year, but lower than the targeted 3.5%.

The size of Pakistan’s economy (nominal GDP) stood at Rs106.045 trillion in FY24, showing a growth of 26.4% over last year (Rs83.87tr). In US Dollar terms, it rose to $374.9 billion.

During FY24, per capita income increased by $129 or 8.3% to $1680 as compared to $1,551 last year. That compares with the last 10-year average of $1,626.

The increase was on the account of increase in economic activity and appreciation in the exchange rate.

In PKR terms, it stood at Rs475,281 compared to Rs384,747 in the previous year, up 23.5%.

The investment to GDP ratio, however, fell to 13.14% in FY24 compared to 14.13% in FY23 mainly due to contractionary macroeconomic policies and political uncertainty.

The saving to GDP ratio was recorded at 13.0% in FY24 compared to 13.2% in FY23.

The growth of agriculture sector was at 6.25% in FY24. This growth is mainly driven by 16.82% growth in important crops such as wheat, rice, and cotton.

The robust growth in agriculture sector, the highest in last 19 years emerged as the key driver of economic growth in FY24.

The industrial sector posted a positive growth of 1.21% in FY2024. Industrial sector performance is mainly driven by the manufacturing sector (2.42%) and construction sector (5.86%).

Services sector constitutes the largest share of 57.7% in GDP for FY2024. This sector also witnessed a moderate growth of 1.21%.

External Sector

The current account deficit during July-May FY24 narrowed significantly to $464m, showing an improvement of 87.7% YoY when compared to the deficit of $3.77bn in 11MFY23.

During the first 11 months of current fiscal year, exports rose 9.3% YoY to $35.81bn compared to $32.77bn in the same period last year.

Imports rose 0.4% YoY to $57.63bn in 11MFY24 compared to $57.41bn in the same period last year.

The trade deficit in 11MFY24 was recorded at $21.82bn, a drop of 11.4% YoY when compared to the deficit of $24.64bn in 11MFY23.

Furthermore, the Pakistani Rupee (PKR) remained largely stable against USD. The local unit gained 7.65 rupees or 2.75% against USD.

Fiscal sector

Fiscal indictors also showed improvement during July-March FY24.

The primary surplus increased to 1.5% of GDP, while the overall deficit remained almost at last year’s level.

Inflation

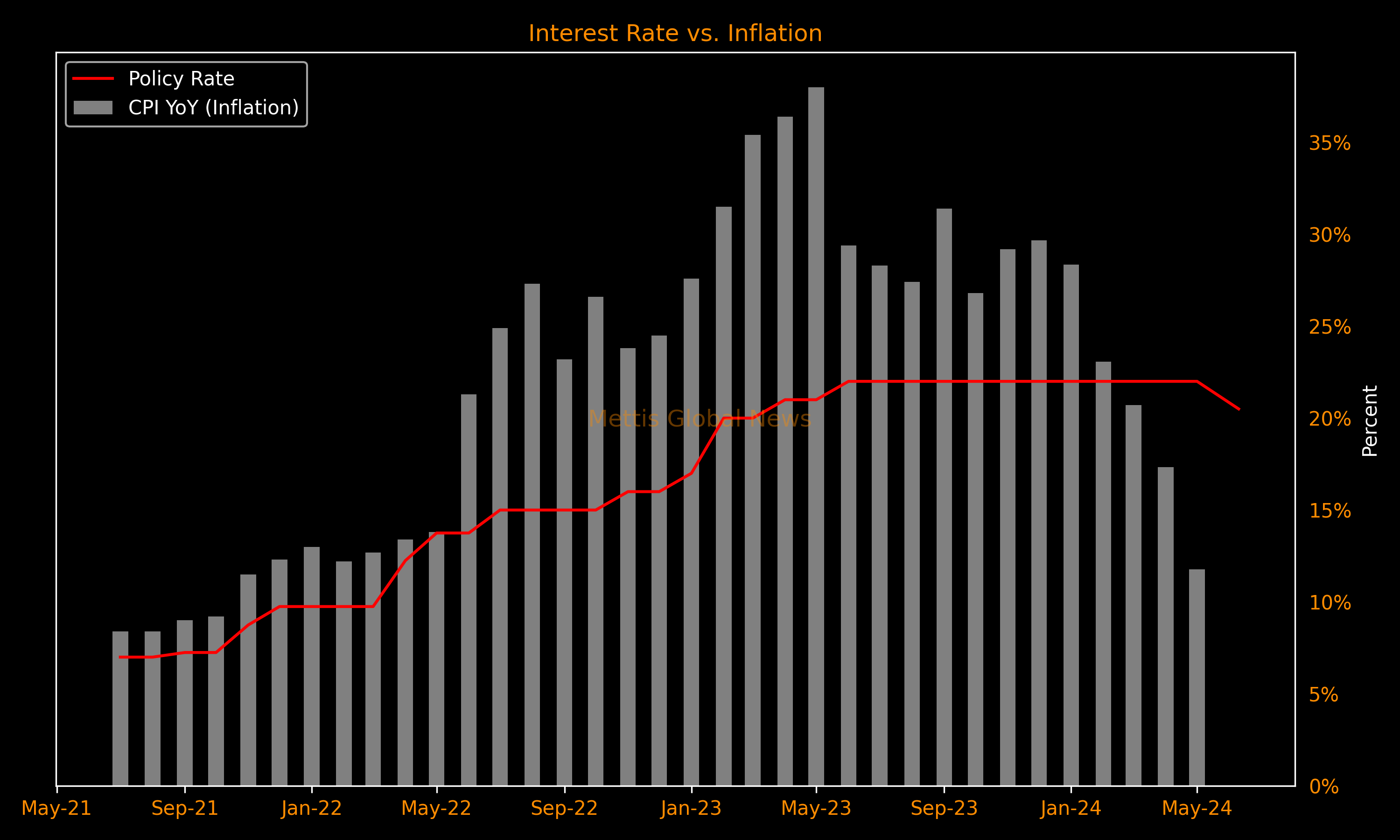

Headline inflation decelerated to 11.8% in May 2024 from a record 38% in May 2023.

The average yearly inflation of 11MFY24 fell to 24.5% YoY compared to 29.2% YoY in 11MFY23.

Core inflation also decelerated to 14.2% in May 2024 from 22.7% in May 2023. However, average yearly core inflation remained sticky at 19.3% in 11MFY24 as against 17.5% in the same period of last year.

The State Bank of Pakistan (SBP) lowered its key policy rate by 150 basis points to 20.5% this, a bigger margin than expected by market analysts.

The reduction was the first in almost four years.

Outlook

The bullish trend is seen extending into FY 2024-2025, driven by one of the cheapest valuations in Asia, coupled with strengthened prospects of securing a new IMF loan amidst a tax-heavy budget.

Despite nearly doubling in value over the past year, the KSE-100 Index still trades at a price-to-earnings ratio of 5.86, a 21% discount to the last 5-year average of 7.42.

Furthermore, inflation has decelerated significantly, pushing the real interest rates to 8.7%. The SBP — which kicked off an easing cycle this month — is expected to further lower rates in the near term.

Historical data show start of a rate-cut cycle bodes really well for the local stock market.

Six months following the first rate cut, the KSE-100 index has averaged a 14.9% gain, data from the past six easing cycles compiled by Mettis Global show.

Similar sentiments were echoed in the median estimate of market strategists in a Mettis Global survey.

The survey's median projection is for the KSE-100 Index to finish 2024 in the 80,000-90,000 range, an average 8% above Friday’s close.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,295.00 | 64,390.00 63,875.00 | 80.00 0.12% |

| BRENT CRUDE | 98.70 | 101.19 95.13 | -1.99 -1.98% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 121.10 121.10 | 0.70 0.58% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.47 | 92.83 87.68 | -1.72 -1.87% |

| SUGAR #11 WORLD | 14.76 | 14.79 14.54 | 0.07 0.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|