PKR FY24 Review: Rising From Ashes to Harmony

Rafay Malik | July 01, 2024 at 08:45 AM GMT+05:00

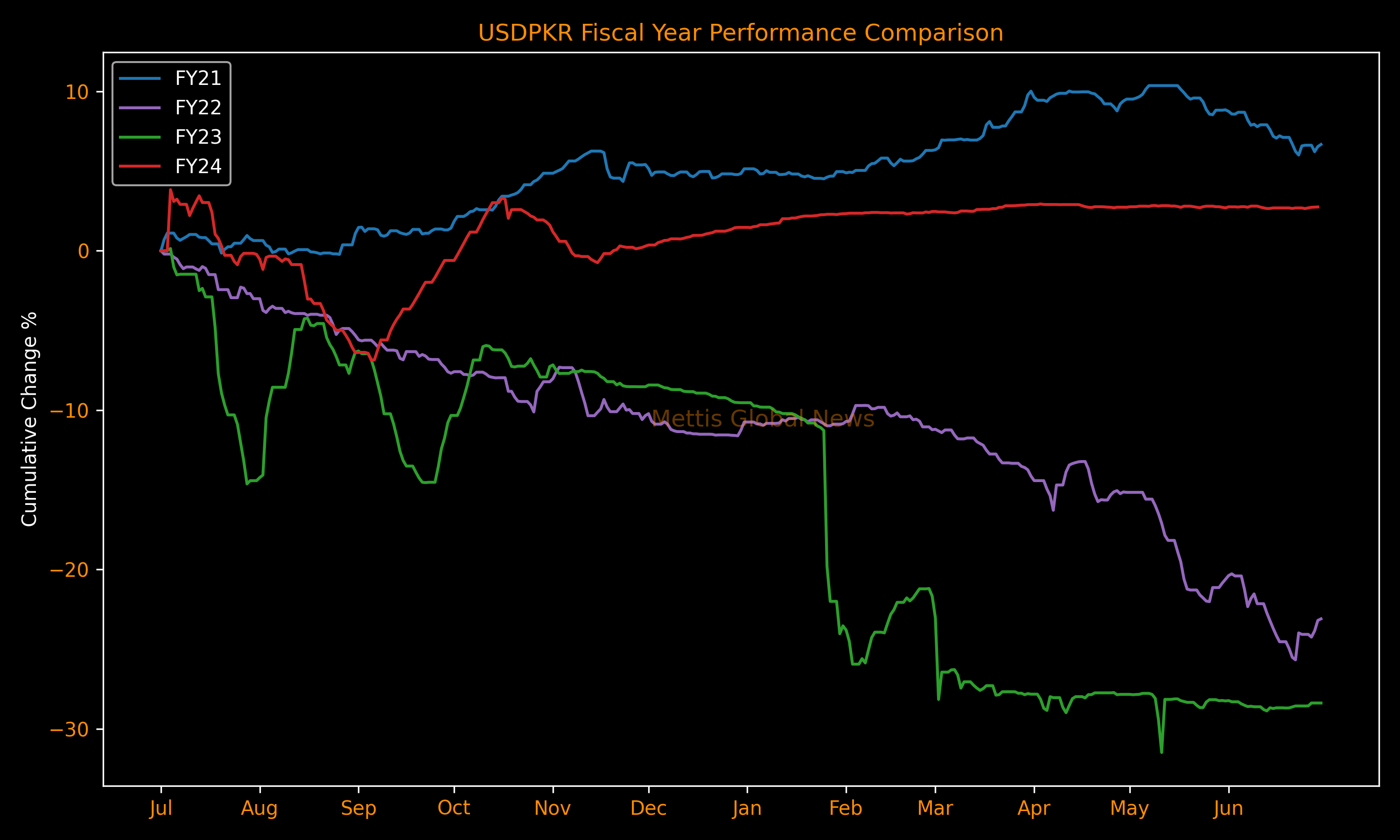

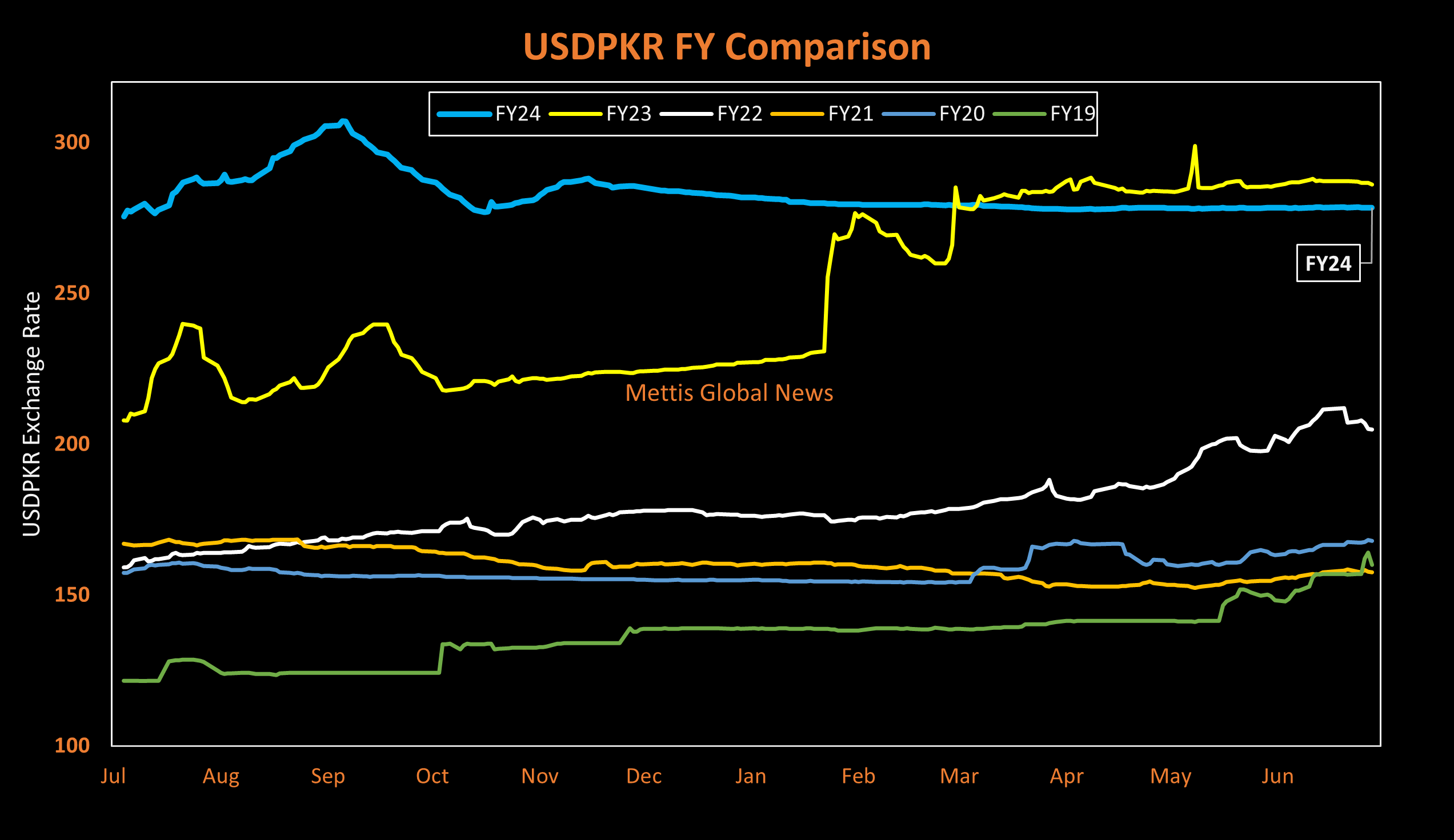

July 01, 2024 (MLN): Pak Rupee’s journey during the fiscal year (FY24) can be described as tough yet remarkable, as the currency rebounded from its all-time low against the mighty Dollar in the early months to a modest gain by the end of the fiscal year.

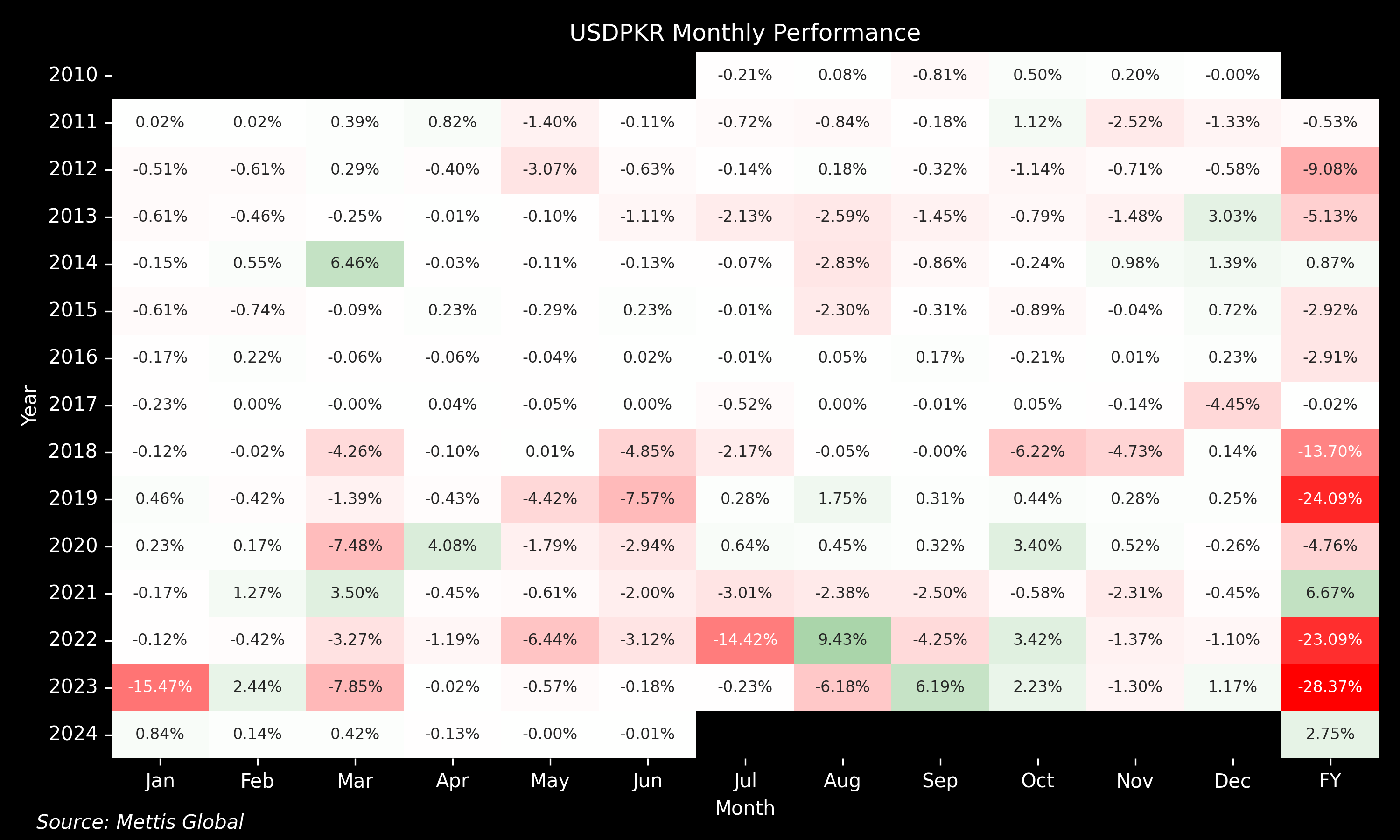

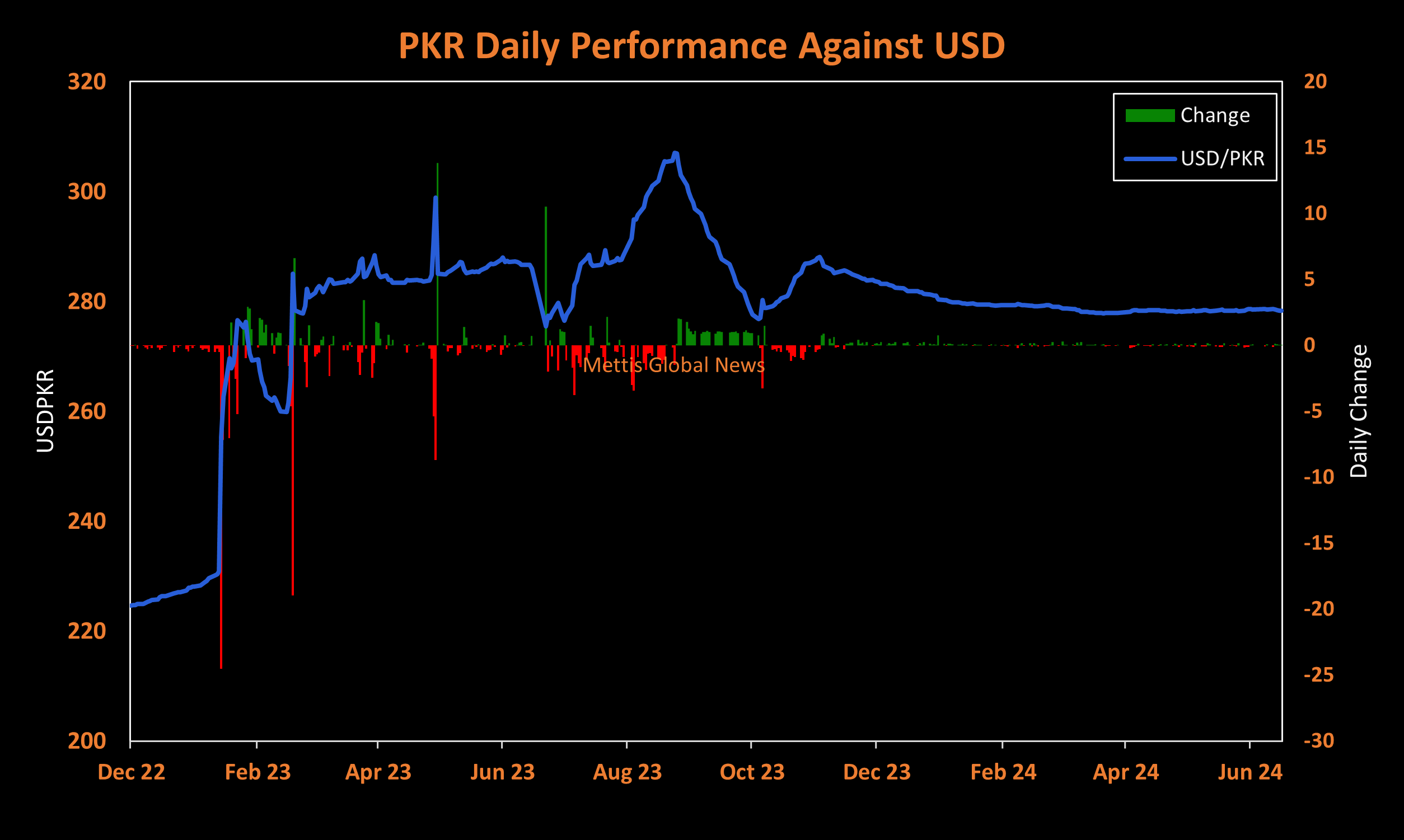

The domestic unit settled FY24 at 278.34 per USD, an improvement of over 7.65 rupees or 2.75% compared to the closing rate of 285.99 for FY23.

This marks PKR’s first appreciation in three fiscal years, which can also be seen as a slight recovery from the cumulative loss of over 128 rupees witnessed in the past two fiscal years.

The average exchange rate during this period stood at 283.23 per USD compared to the average of 248 per USD in FY23, reflecting a seesaw journey with continuous fluctuations.

Nonetheless, several positive triggers helped the country’s currency achieve a favorable closure.

Pakistan’s 9-month SBA with the International Monetary Fund (IMF) emerges as one of the primary factors contributing to the resilience of PKR as it provided a policy anchor to eliminate FX shortages by returning to proper FX market functioning.

The government eliminated the multiple currency practices related to exchange rates applied to transactions with the SBP, along with all the remaining exchange restrictions resulting from the limitation on advance payments for imports.

However, the removal of restrictions on letters of credit (LCs) led to a widening gap between the interbank and open market rates as the demand for dollars spiked.

This became a major concern until the government launched a robust crackdown against culprits dealing in the black market and draining dollars from the country.

The restriction of illegal Dollar trade shifted Pakistani diasporas to formal channels, which boosted the flow of remittances into the country.

Subsequently, the spread between interbank and open market rates, which had reached a high of around 9% in May 2023 almost vanished and currently stands well below the IMF's recommended limit of 1.25%.

The central bank also took several initiatives to pump transparency into the forex market as it decided to consolidate and transform various types of ECs into a single category with a well-defined mandate.

Additionally, leading banks actively engaged in foreign exchange business were directed to establish their wholly owned ECs to cater to the legitimate foreign exchange needs of the general public.

As of now, several well-reputed and large banks, such as UBL, Meezan, HBL and BAHL, have launched their exchange companies across various cities in the country.

In a related development, the central bank even raised the validity of allowing ECs to import cash US Dollars up to 50% of the value of their export consignments by another 6 months, to ensure an adequate supply of cash Dollars in the open market.

On a parallel note, the successful reviews following the agreement with the IMF helped build the nation’s foreign exchange reserves, by unlocking funds and opening new avenues of borrowing and rollovers through multilateral and bilateral partners.

Another favorable transition for the local Rupee was observed as the real interest rates in the economy turned positive in March 2024, after over 3 years as inflationary pressures eased due to the high base effect.

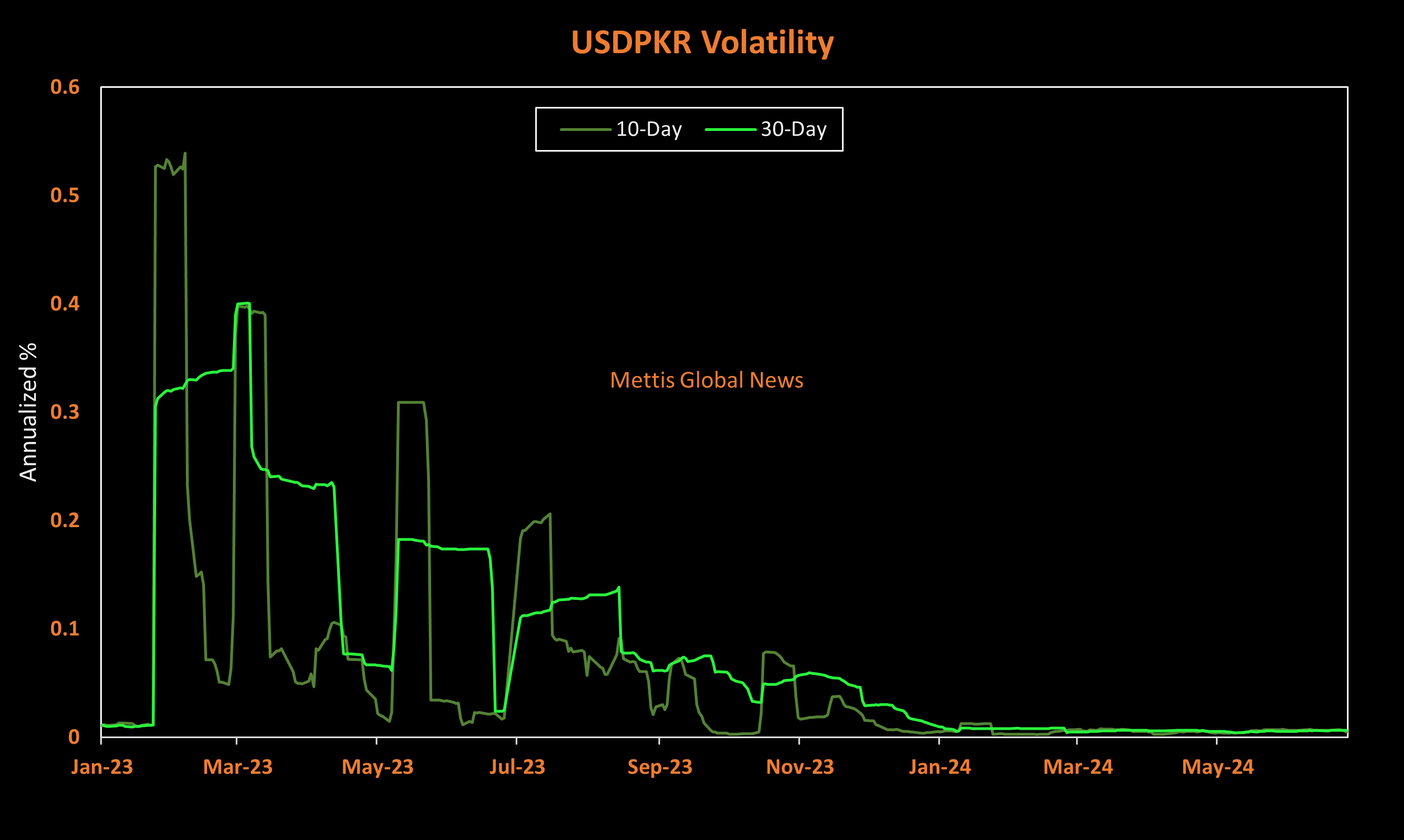

As the economy stabilized with these positive pushes, Pakistan's currency significantly reduced its exposure to volatility and entered the dead flat arena.

What stands out is the robust comeback that PKR has made, transitioning from one of its most volatile phases before this fiscal year (January-May 2023) to the zone of stability and consistency.

Hence, the success story of the domestic unit can be attributed to both administrative measures and foreign support, which in turn bolstered the confidence of the local population and other countries.

The back-to-back visits from Saudi Arabia and China for investment talks are a major indicator of the increased focus of countries on investing in and supporting Pakistan.

However, the journey was not entirely advantageous for the currency as certain hardships arose due to the sudden and usual uncertainty arising on the political front.

The instability regarding the new government's formation created a state of confusion for the economy. Furthermore, disputes over decisions within the coalition government worsened the situation.

The U.S. Dollar Index (DXY), which tracks the value of the greenback against six other top currencies also placed slight pressure on PKR as it improved by 4.89% to 100.85 by FY24.

Nonetheless, as the economy progressed and the macroeconomic condition across various segments improved, the Rupee somehow managed to enter back into its stable zone and closed the fiscal year with a bang performance.

Improved Macro-economic triggers

The cash-strapped nation’s foreign exchange reserves witnessed a boost of over 57% to reach $14.4bn, compared to the reserve position of $9.6bn as of FY23.

Likewise, the dollar-desired foreign investment into the country as of the 11 months of FY24 spiked to $1.17 billion, around 143% higher than that in the previous fiscal year.

Though remaining in the deficit zone, the country's current account balance still demonstrated a major recovery as the deficit balance shrank by 87.68% to just $464m in 11MFY24.

Given this, the export sector found itself in a sweet spot, experiencing a growth of over 9% and reaching Rs35.81bn in 11MFY24.

Despite easing import restrictions, the country managed to control its outflow of foreign currency, with figures recorded as just 0.38% higher compared to 11MFY23.

The most burdensome payment, that of petroleum imports, was lowered due to reduced volumes, even though global oil prices moved higher

Meanwhile, Pakistan's Rupee Real Effective Exchange Rate Index (REER) showed a strong recovery, rising from historical lows in May 2023 to 100.67 as of May 2024.

Outlook

The currency's outlook appears quite gloomy, considering both the anticipated positive and negative pressures.

IMF has flagged that the recent stability of the rupee should not lead to renewed expectations that this will persist in the future as policy slippages, together with lower external financing, could undermine the narrow path to debt sustainability and place pressure on the exchange rate.

Furthermore, a potential resurgence in Pakistan's social tensions, reflecting the complex political scene and high cost of living could weigh on policy and reform implementation.

The currency will also remain exposed to geopolitical tensions, which could drive commodity prices higher and tighten global financial conditions.

On the other hand, productive engagements with Saudi Arabia and China are expected to boost trade, cooperation, and FDI into the country, which would in turn attract Dollars into the country.

Going ahead, the central bank will remain stringent and proactive to ensure transparency in the forex market through effective monitoring.

The next expanded program with the IMF, worth $6 to $8 billion, is on the cards. Accordingly, it is expected to be a key influencer for Pakistan's currency and could potentially help the country navigate towards a stable and secure economic zone.

Majority of the well-reputed agencies sight the highest probability of a successful conclusion due to the aggressive budget, released back on June 12, 2024.

However, one significant threat that has the potential to overshadow all good desires for the Pak Rupee is the soaring debt obligations, which would create an external funding gap and might push Pakistan away from stability to the bad books once again.

Whoever assumes the country's leadership will need to make smart, strict, and mainly transparent decisions, as there remains much yet to be resolved.

Copyright Mettis Link News

Related News

.jpg_20260424071638623_13fb19.jpeg?width=280&height=140&format=Webp)

_20260101112329999_0153db_20260209062258909_9180ec.webp?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,430.02 376.06M | -0.19% -346.57 |

| ALLSHR | 109,168.67 713.66M | -0.13% -139.83 |

| KSE30 | 54,263.26 125.13M | -0.24% -128.56 |

| KMI30 | 255,651.73 86.61M | -0.19% -483.04 |

| KMIALLSHR | 69,991.04 446.60M | -0.05% -33.30 |

| BKTi | 52,205.98 60.34M | -0.31% -161.74 |

| OGTi | 35,363.45 11.64M | 0.17% 60.63 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 65,150.00 | 65,355.00 65,035.00 | -25.00 -0.04% |

| BRENT CRUDE | 82.38 | 84.44 81.50 | -0.11 -0.13% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 105.50 105.50 | -0.25 -0.24% |

| ROTTERDAM COAL MONTHLY | 116.25 | 117.00 116.25 | -0.10 -0.09% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 77.08 | 78.77 76.53 | -0.21 -0.27% |

| SUGAR #11 WORLD | 16.49 | 16.50 15.49 | 0.92 5.91% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|