Pakistan economy to record real GDP growth of 4.2 percent in FY22: Fitch

MG News | September 20, 2021 at 09:20 AM GMT+05:00

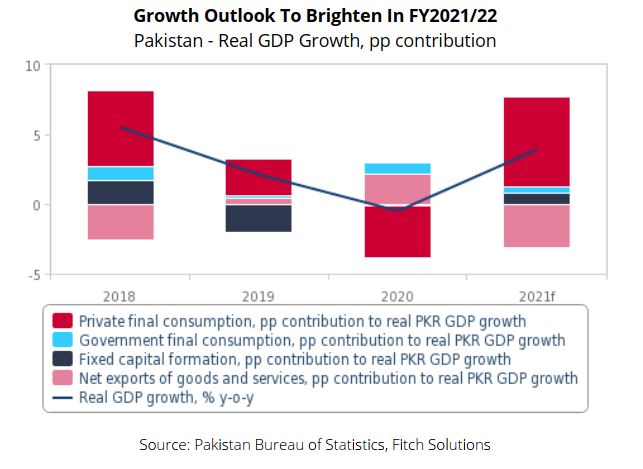

September 20, 2021 (MLN): Pakistani economy is expected to record real GDP growth of 4.2% in FY2021-22 (July 2021-June 2022), up from 3.9% in FY21, says Fitch Solutions in its latest report.

The report noted that improving vaccination rates will buoy private consumption growth while supportive monetary and fiscal conditions will serve as tailwinds for gross fixed capital formation.

As highlighted in its last update, its forecast accounts for the occasional tightening of Covid-19 restriction measures due to the still elevated number of domestic Covid-19 cases. This comes as Pakistan grapples with its fourth wave of Covid-19 outbreaks. Nevertheless, with the government likely to continue with its “smart-lockdown” strategy instead of imposing a nationwide lockdown, Fitch does not expect Pakistan’s growth trajectory to be severely curtailed.

Additionally, the pickup in the vaccination rate in recent months will likely reduce the possibility of extended lockdowns in the future. It also expects the economy to be buoyed by accommodative monetary and fiscal stances (public spending). A more assured economic outlook will bode well for consumption and investments, bolstering economic growth.

With regards to private consumption, Fitch Solutions has revised its forecast to grow by about 3.6% in FY22 compared to 3.4% previously. While this still represents a slowdown from the 7.4% in FY21 due to waning base effects, improving vaccination rates will buoy consumer sentiment, facilitating recovery in consumer spending.

To note, the country’s consumer confidence rose in July, coming in at 44.1, its highest reading since September 2019 (pre-pandemic levels). As a sign of recovering demand, purchases of major items like passenger vehicle sales have surpassed pre-pandemic levels. Additionally, the report’s expectation for still strong remittance growth amid a stronger economic growth outlook in the Gulf Cooperation Council (GCC) economies and the European Union, will also support private consumption.

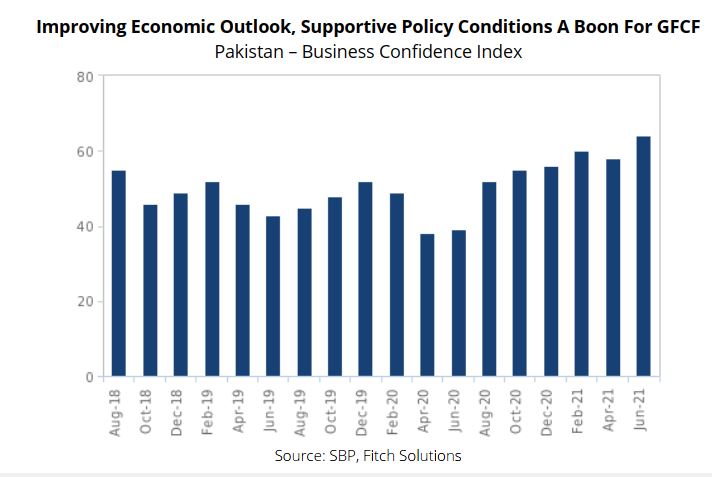

It has also revised up its forecast for Gross fixed capital formation (GFCF) growth to 8.0% in FY22 from 7.2% previously. GFCF will be driven by improving domestic and external demand outlooks alongside supportive monetary and fiscal conditions. The country’s business confidence survey by the State Bank of Pakistan (SBP) recorded its highest ever levels in June (latest data available) since its inception, reflecting optimism surrounding the business outlook of Pakistan. Accommodative monetary policy, coupled with disbursements from the SBP’s Temporary Economic Refinance Facility (TERF) will further serve as tailwinds for capacity enhancing investments. According to the SBP estimates, TERF loan disbursements are expected to increase by 67% this fiscal year.

Another catalyst for growth in this component is increased development spending by the government According to Pakistan’s FY22 fiscal budget, allocations to the Public Sector Development Programme surged by 61.3% compared with the budgeted amount in the previous fiscal year, coming in at PKR2.1trn.

Meanwhile, it revised up its forecast for government consumption growth to register at 4.3% in FY22 from its previous forecast of 3.5%. This is broadly similar to the growth rate of 4.1% witnessed in FY21.

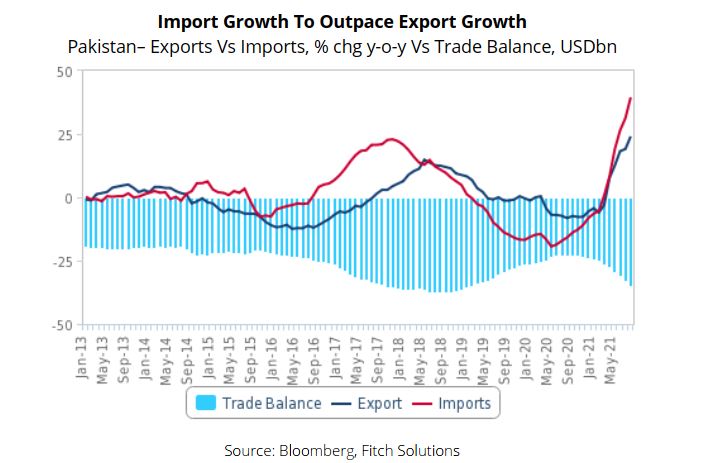

Lastly, it is now expected that net exports to subtract 1.0pp from headline growth, revised from -0.4pp previously. This comes as it expects imports to rebound more strongly than exports. Imports will be supported by increased demand for vaccines with the government recently committing USD1.1bn to procure Covid-19 vaccines. Additionally, the improving economic outlook will likely see a rebound in consumer spending and increased demand for capital goods.

Finally, with petroleum products accounting for approximately 18.0% of total imports value in FY21, elevated fuel prices will further increase Pakistan’s imports bill. Fitch Oil & Gas team forecasts Brent crude oil prices to average USD72.00 per barrel (/bbl) in 2021 and USD69.00/bbl in 2022 from USD43.20/bbl in 2020. Hence, the report pencils in 8.0% growth in imports for FY22, a revision upwards from its previous expectation of 5.0% growth.

Risk To Outlook

The risk to the growth outlook is weighted to the downside. On the domestic front, given the more virulent delta strain in the community, amid a still low percentage of the population that are fully vaccinated, a strong resurgence in Covid-19 infections could weigh heavily on growth.

On the external front, heightened security threats posed by radical groups such as the Pakistan Taliban Group could lead to social instability and the destruction of infrastructure. This might weigh on the country’s gross fixed capital outlook and exporting capabilities as businesses become hesitant to invest in capacity-building infrastructure.

Copyright Mettis Link News

Related News

.png?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 176,282.16 179.12M | 3.08% 5260.96 |

| ALLSHR | 106,822.08 424.54M | 2.88% 2985.69 |

| KSE30 | 52,627.62 61.53M | 3.29% 1675.63 |

| KMI30 | 248,687.20 58.77M | 3.35% 8053.34 |

| KMIALLSHR | 68,550.41 226.82M | 2.97% 1977.66 |

| BKTi | 50,167.05 17.70M | 3.07% 1493.82 |

| OGTi | 34,909.78 4.81M | 3.58% 1207.52 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 65,555.00 | 66,075.00 63,875.00 | 1340.00 2.09% |

| BRENT CRUDE | 90.95 | 93.60 89.58 | -5.83 -6.02% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 0.00 0.00 | 0.85 0.71% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.97 | 86.20 83.10 | -5.34 -5.98% |

| SUGAR #11 WORLD | 14.76 | 0.00 0.00 | -0.01 -0.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|