Oil heads for weekly decline on surging dollar, demand concerns

MG News | November 15, 2024 at 04:06 PM GMT+05:00

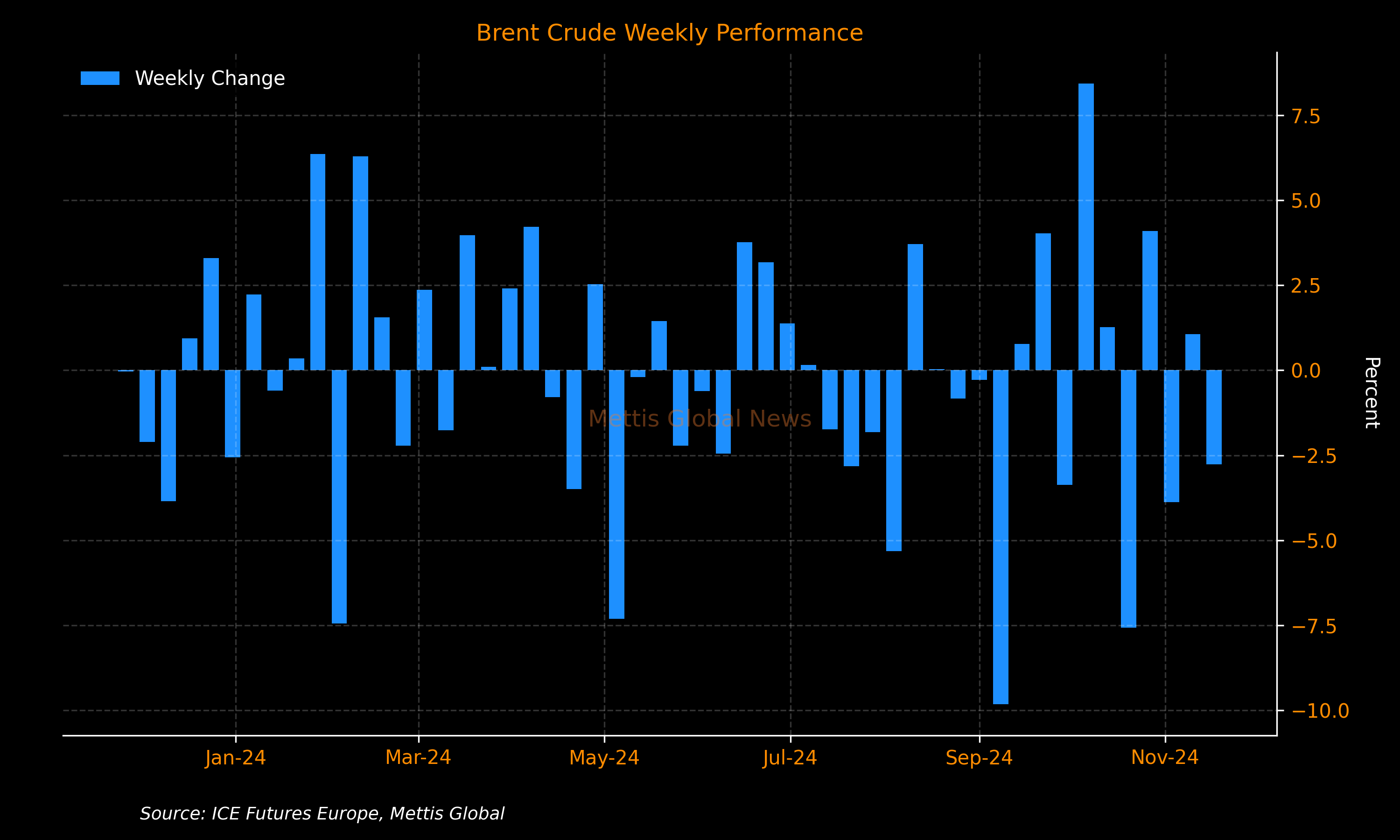

November 15, 2024 (MLN): Oil fell on Friday and remained on track for a weekly loss as a surging US dollar and concerns about demand growth weighed on the outlook for prices.

Brent crude dropped 1.1% to $71.76 a barrel and was down by around 2.8% this week.

While West Texas Intermediate crude (WTI) was at $67.92 per barrel, down by 1.1% on the day.

The International Energy Agency said on Thursday it expects a surplus next year as demand growth in China slows, while global output swells, Bloomberg reported.

The glut will be even bigger if OPEC+ presses on with plans to revive halted production.

In China, while figures on Friday showed some encouraging signs for the wider economy after Beijing’s latest round of stimulus, apparent oil demand still declined in October from a year earlier.

In addition, local refiners processed 4.6% less oil than in the same month of 2023.

Crude has been alternating between weekly gains and losses since mid-October, buffeted by tensions in the Middle East, the prospect of oversupply, and shifts in currency markets.

Year-to-date, Brent has retreated by more than 6%, after touching its lowest since 2021 in September.

“While there are some positive signs in the broader data, clearly we are not out of the woods yet,” said Warren Patterson, head of commodities strategy for ING Groep NV, referring to the Chinese economic figures. “Industrial production was weaker than expected; oil-specific numbers were also not great, with both refinery activity and implied demand weaker.”

Other commodities such as copper have also struggled this week as a gauge of the dollar rallied to the highest in two years, powering upward in the aftermath of Donald Trump’s election victory.

Despite a retreat on Friday, the US currency is set for its seventh weekly gain, making raw materials priced in the greenback less appealing.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 134,299.77 290.06M |

0.39% 517.42 |

| ALLSHR | 84,018.16 764.12M |

0.48% 402.35 |

| KSE30 | 40,814.29 132.59M |

0.33% 132.52 |

| KMI30 | 192,589.16 116.24M |

0.49% 948.28 |

| KMIALLSHR | 56,072.25 387.69M |

0.32% 180.74 |

| BKTi | 36,971.75 19.46M |

-0.05% -16.94 |

| OGTi | 28,240.28 6.19M |

0.21% 58.78 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 118,140.00 | 119,450.00 115,635.00 |

4270.00 3.75% |

| BRENT CRUDE | 70.63 | 70.71 68.55 |

1.99 2.90% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

1.10 1.14% |

| ROTTERDAM COAL MONTHLY | 108.75 | 108.75 108.75 |

0.40 0.37% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.75 | 68.77 66.50 |

2.18 3.27% |

| SUGAR #11 WORLD | 16.56 | 16.60 16.20 |

0.30 1.85% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|