MPS Preview: Will the Rate Cut Party Pause today?

Nilam Bano | March 10, 2025 at 01:27 PM GMT+05:00

March 10, 2025 (MLN): After months of steady rate cuts, all eyes are on the State Bank of Pakistan (SBP)’s big call in today’s Monetary Policy Committee (MPC) meeting. With 1,000 bps already slashed, the policy rate sits at 12.

While another cut is widely expected, rising yields and shifting liquidity hint at a possible pause.

Investors' sentiments remain divided as the market consensus indicates a rate cut between 50 to 100 bps, while Mettis Global’s survey leans towards a 100 bps reduction mainly on the back of dropping inflation which reached 1.5% in February.

However, tightening liquidity and a surge in market yields indicate that the central bank may opt for a more cautious stance.

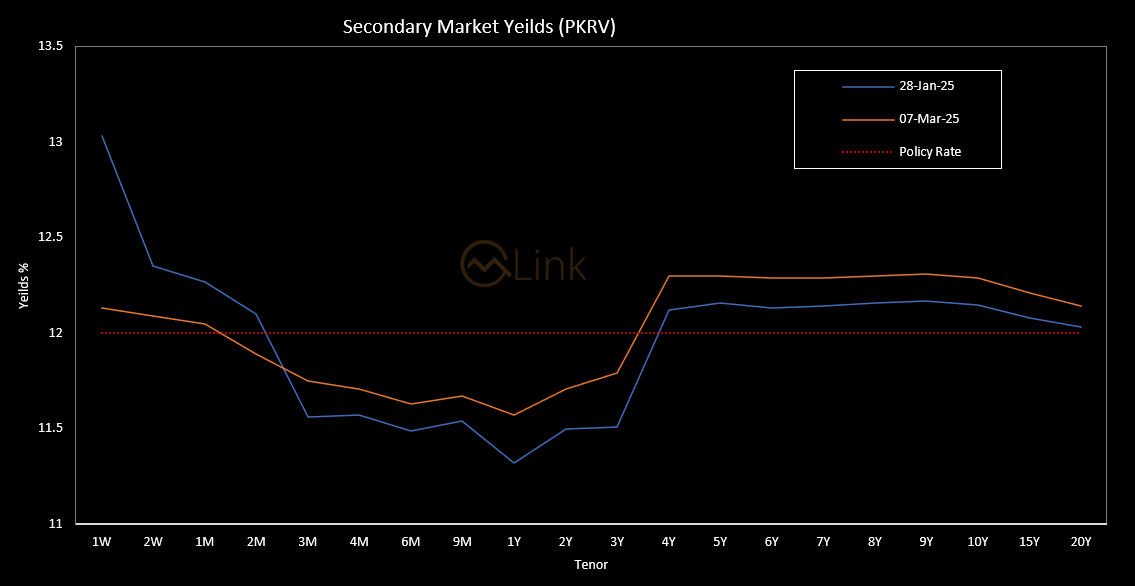

Secondary Market Yields

Since the last MPC meeting, the secondary market has seen a notable increase in yields across various tenors. The 3-year yield surged by 28 bps, while the 1-year tenor rose by 25 bps.

Medium-term tenors also saw gains, with the 2-year and 4-year yields rising by 21 bps and 18 bps, respectively. Long-term yields remained relatively stable, with the 10-year up by 14 bps and the 20-year by 11 bps.

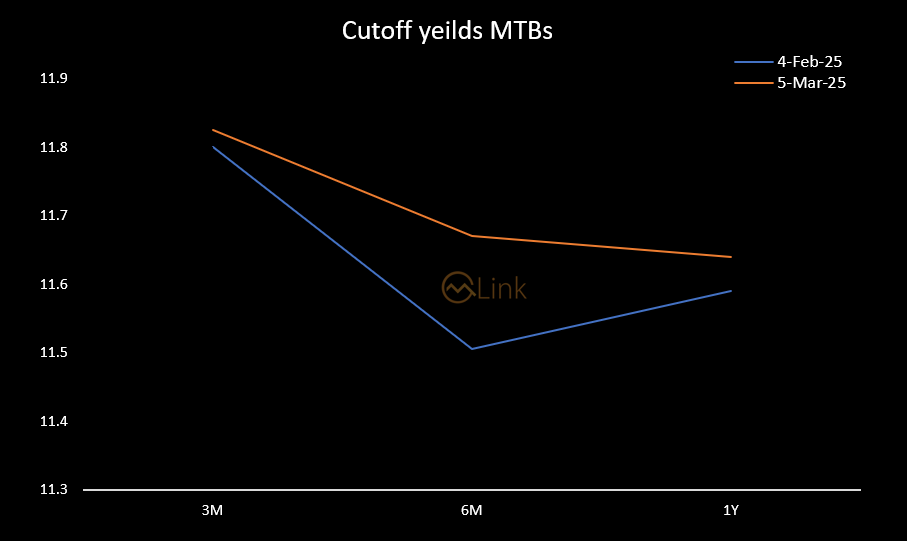

T-Bill Yields

Market Treasury Bills (MTBs) have also exhibited notable shifts. The Cut-off yields increased to 11.8247% for 3 months, 11.6699% for 6 months, and 11.6400% for 12 months.

Since the last MPC meeting, the significant increase was observed in the 6M T-bill yield (+16.51 bps) compared to the 3M (+2.49 bps) and 1Y (+5.02 bps).

This indicates shifting investor sentiment, mainly due to inflation expectations, liquidity conditions, and anticipated monetary policy adjustments.

The Central Bank also absorbed Rs117.1 billion in bids for 2-year and 3-year Floating Rate Pakistan Investment Bonds (PFLs) while rejecting all 5-year bids. Out of Rs334.23bn worth of bids received, only a fraction was accepted, signalling careful liquidity management by the central bank.

This move hints that the SBP may not rush into aggressive rate cuts and could adopt a wait-and-watch approach.

In addition, a possible reduction in the Cash Reserve Requirement (CRR) could be on the table in the upcoming Monetary Policy which will add another layer to SBP’s rate decision.

The local unit is also started facing pressure as it neared the 280-mark, hitting a 52-week low as it depreciated by 15.33 paisa or 0.05% against the US Dollar (USD) in Friday’s interbank session. It settled at PKR 279.97 per USD, compared to the previous close of PKR 279.82.

This decline marks a 0.88% depreciation from its 52-week high of 277.5179, recorded on October 4, 2024.

On the external front, breaking the streak of three consecutive surplus, Pakistan recorded a current account deficit of $420m in January 2025.

Last month, the country recorded a current account surplus of $474m in January 2024, the current account deficit stood at $404m.

Pakistan’s trade deficit in February 2025 widened by 33.43% YoY to $2.3bn, up from $1.72bn in February 2024, driven by a 10% YoY surge in imports to $4.7bn.

On the IMF front, the Fund has begun review talks under Pakistan’s $7 billion loan program, with a primary focus on economic and structural reforms.

The government is also negotiating a Rs1.25 trillion ($4.47 billion) loan with commercial banks to reduce its bulging energy sector debt.

Last time, the SBP reduced the policy rate by 100 basis points to 12%, effective January 28, 2024. The reduction was the sixth in a row, bringing the total decrease since June 2024 to 1,000bps as a slowdown in inflation gave policymakers room to continue monetary easing in a bid to spur growth.

With inflation easing to 1.5% in February from 2.4% in January, the 8-month average now stands at 5.85%. However, inflation is expected to rise in the coming days due to Ramadan, Eid, and the low base effect.

Furthermore, global inflationary pressures particularly in light of Trump’s proposed tariffs on major trading partners like Mexico, Canada, China, and the EU will be a key factor influencing SBP’s decision-making.

Not to forget, Pakistan’s fragile foreign exchange reserves also pose a risk. A surge in domestic demand could trigger currency devaluation and drive inflation higher.

Thus, given the ongoing global uncertainty and external vulnerabilities, SBP is likely to adopt a cautious stance.

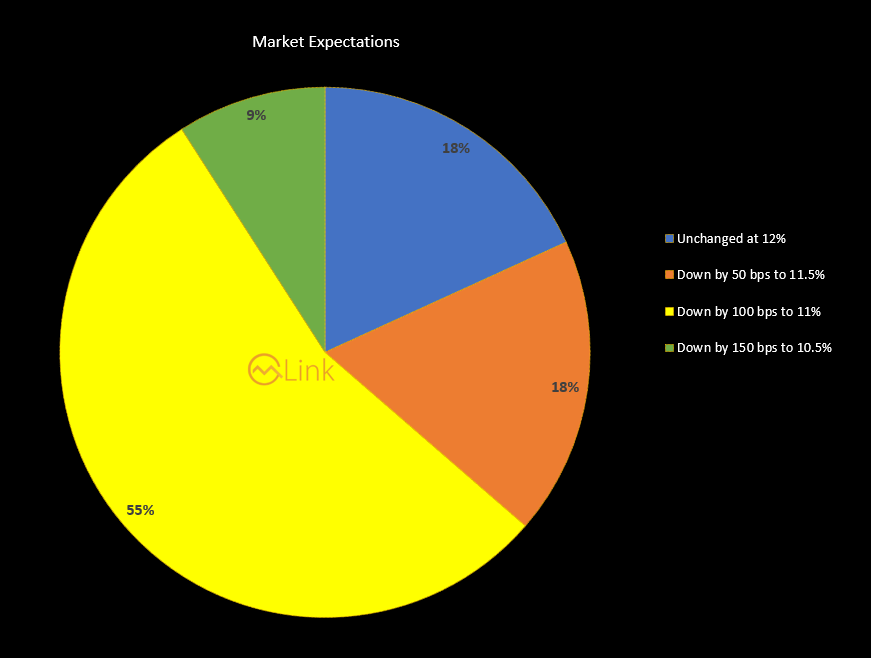

Survey Result

To estimate market expectations for the upcoming monetary policy meeting scheduled for today, Mettis Global surveyed various sectors.

Our survey reveals a strong expectation for a rate cut in the upcoming monetary policy statement.

A majority (55%) of respondents expect a 100bps reduction, while 18% anticipate a 50bps cut, and another 18% believe the policy rate will remain unchanged at 12%. Meanwhile, 9% predict a 150bps reduction.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 150,398.71 270.15M | -1.06% -1612.55 |

| ALLSHR | 90,084.08 469.39M | -0.93% -849.88 |

| KSE30 | 45,453.36 99.47M | -1.14% -522.50 |

| KMI30 | 218,271.12 195.05M | -0.92% -2019.44 |

| KMIALLSHR | 58,965.48 294.49M | -0.81% -483.69 |

| BKTi | 41,775.34 33.94M | -0.76% -317.96 |

| OGTi | 31,328.42 11.96M | -0.61% -192.61 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 67,165.00 | 67,625.00 66,480.00 | -15.00 -0.02% |

| BRENT CRUDE | 109.24 | 109.74 99.08 | 8.08 7.99% |

| RICHARDS BAY COAL MONTHLY | 112.50 | 0.00 0.00 | 6.40 6.03% |

| ROTTERDAM COAL MONTHLY | 113.00 | 114.50 113.00 | -0.40 -0.35% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 112.06 | 113.97 97.50 | 11.94 11.93% |

| SUGAR #11 WORLD | 14.96 | 15.50 14.91 | -0.33 -2.16% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|