MPS Preview: No change in policy rate expected as inflation eases

Abdur Rahman | January 23, 2024 at 12:34 PM GMT+05:00

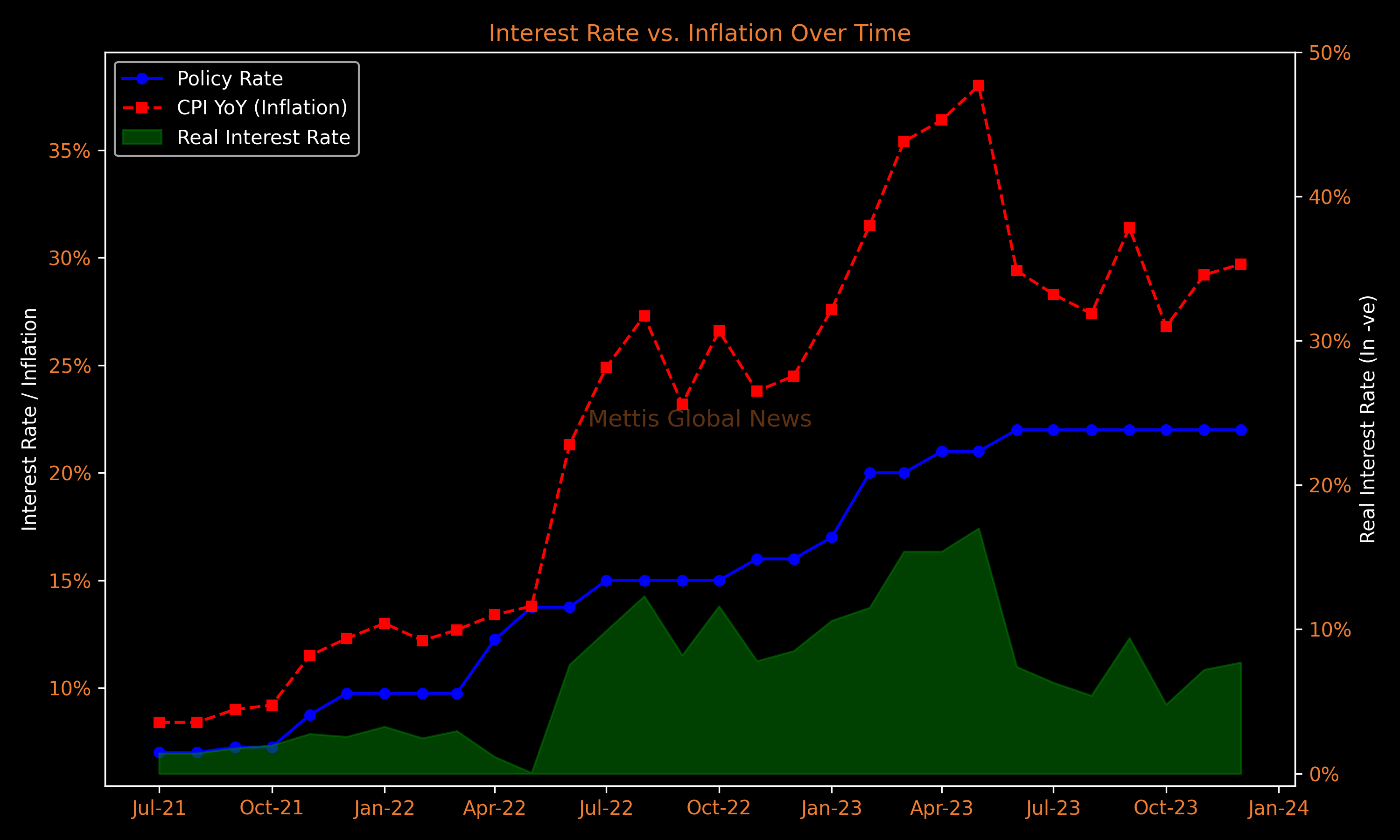

January 23, 2024 (MLN): The Monetary Policy Committee (MPC) of the State Bank of Pakistan (SBP) is widely expected to maintain its policy stance of keeping the interest rate unchanged at 22% in the upcoming meeting, as inflation expectations are on a downward path amid easing food and energy prices.

To gauge market sentiment, Mettis Global News conducted a survey regarding the upcoming central bank's monetary policy decision, which is scheduled to be held on January 29.

The survey results imply a status quo, with the majority of participants (57.69%) expecting the SBP to maintain the policy rate at 22%.

However, this was down significantly from the last MPC survey, wherein 74% of participants expected a status quo.

Accordingly, around 26% anticipate a rate cut of 100 basis points (bps), while 10% expect a 50 bps cut.

The survey results further revealed that market participants are now more inclined toward rate cuts starting in the first quarter of 2024.

The majority (43.3%) believe the SBP will begin rate cuts in the first quarter of FY24, with 25% expecting it to be cut in the very next meeting.

Additionally, 27% of participants anticipate rate cuts beginning in the second quarter of FY24.

Furthermore, there was a strong consensus among participants that the policy rate would fall within the range of 15-19% by the end of FY24, with the majority (60.6%) expecting a cumulative cut of 300-700 bps.

Despite the sticky inflation, which stood at 29.7% in December, this is a stark contrast to the previous MPC survey results, wherein only 37.2% of participants expected it to be within this range.

Meanwhile, 32.7% of participants expect it to be within the 19-21% range by the end of FY24.

Market participants continued to believe the central bank would cut rates even before inflation drops below 22%.

The survey revealed that 34.6% of participants do not expect the real interest rate to turn positive until the second quarter of FY24, while 28.9% do not believe that the real interest rate will turn positive until the fourth quarter of 2024.

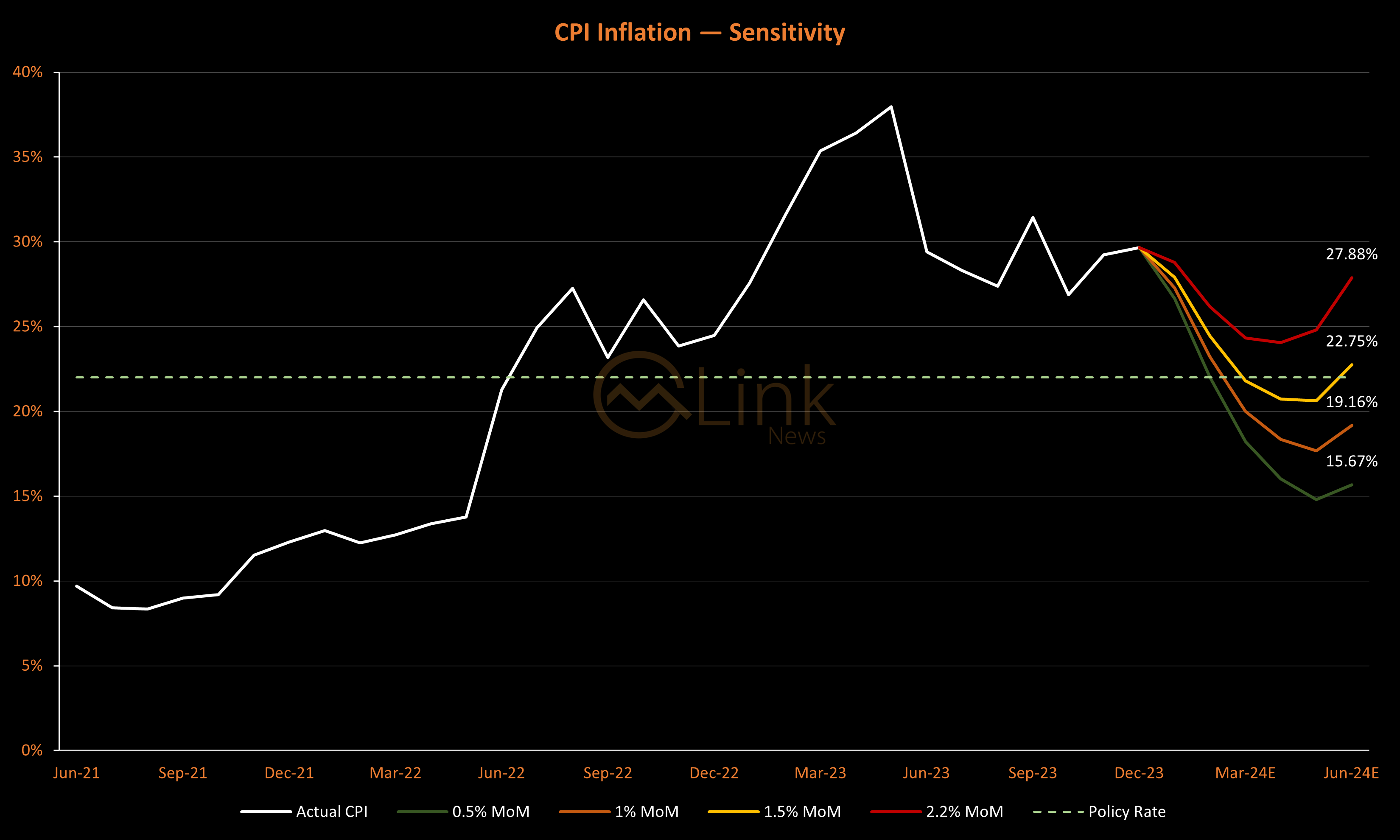

Inflation forecast

With a 0.5% month-over-month (MoM) inflation rate, the annual headline inflation will stand around 22% by February and fall below 16% by June 2024.

In contrast, even a 1% MoM inflation rate, which is also significantly lower than the 12-month average of 2.2% MoM, will keep real interest rates from turning positive until March 2024.

The following chart maps out the yearly inflation trajectory based on monthly inflation rates of 0.5%, 1%, 1.5%, and the 12-month average of 2.2%

Inflation easing, but challenges persist

To note, the International Monetary Fund (IMF) has revised down the inflation forecasts, projecting CPI to average 24% in FY24 from earlier projection of 25.9% amid easing food and energy prices, as per the first review report published by the fund.

Although it noted that the November gas tariff increase will add to headline inflation in coming months, but gradual declines are expected given lower core inflation and recent commodity price movements.

The report said that the year-end inflation is projected to be 18.5% in FY24 and 9% in FY25, respectively.

However, IMF stressed that downside risks remain exceptionally high for the country.

External financing risks are exceptionally high and delays in the disbursement of planned financing from IFIs or bilateral partners could pose major risks to the government's program given limited buffers, it said.

Any external financing shortfalls would increase the government’s reliance on expensive financing from domestic banks, and could further crowd out private credit.

Higher commodity prices and tighter global financial conditions, including due to the intensification of geopolitical conflicts, could put pressure on the exchange rate and external stability.

Additionally, the IMF highlighted that a tight monetary stance is critical to reduce inflation, re-anchor expectations, and support external sector rebalancing through the exchange rate.

The staff sees the stance as broadly appropriate at the current juncture given weak domestic demand.

However, the MPC needs to respond resolutely if near-term price pressures reemerge, including due to second-round effects, and ensure that the real policy rate remains in clear positive territory, it said.

| MPC Survey Results | ||

|---|---|---|

| Questions | Current Results | Previous Results |

| What do you expect from the MPC decision in January, considering the sticky inflation of 29.7% in December? | ||

| +100 bps | 2.88% | 6.98% |

| >-100 bps | 3.85% | 2.33% |

| -100 bps | 25.96% | 16.28% |

| -50 bps | 9.62% | -- |

| Unchanged at 22% | 57.69% | 74.42% |

| When do you anticipate the SBP to begin rate cuts? | ||

| 1Q 2024 | 43.27% | 37.21% |

| 2Q 2024 | 26.92% | 23.26% |

| 3Q 2024 | 4.81% | 13.95% |

| Next meeting | 25.00% | 25.58% |

| Expected Policy Rate by the end of FY24 | ||

| 22% | 4.81% | 4.65% |

| >22% | 1.92% | 11.63% |

| 15-19% | 60.58% | 37.21% |

| 19-21% | 32.69% | 46.51% |

| When do you anticipate the real interest rate turning positive? | ||

| 1Q 2024 | 17.31% | 18.60% |

| 2Q 2024 | 34.62% | 34.88% |

| 3Q 2024 | 19.23% | 9.30% |

| 4Q 2024 | 28.85% | 37.21% |

| Expected USDPKR exchange rate by the end of FY24 | ||

| <270 | 13.46% | 9.30% |

| 270-280 | 20.19% | 9.30% |

| 280-290 | 14.42% | 11.63% |

| 290-300 | 26.92% | 37.21% |

| >300 | 25.00% | 32.56% |

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,846.68 370.24M | -0.81% -1463.60 |

| ALLSHR | 108,777.96 842.70M | -0.57% -624.36 |

| KSE30 | 53,571.08 118.45M | -0.81% -434.78 |

| KMI30 | 253,007.72 126.35M | -1.06% -2717.47 |

| KMIALLSHR | 69,727.55 549.62M | -0.70% -488.73 |

| BKTi | 52,178.22 35.92M | -0.12% -62.01 |

| OGTi | 35,518.90 13.54M | -0.77% -274.36 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,800.00 | 63,810.00 63,760.00 | 200.00 0.31% |

| BRENT CRUDE | 89.32 | 90.03 86.60 | 1.60 1.82% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -4.00 -3.65% |

| ROTTERDAM COAL MONTHLY | 122.00 | 122.00 122.00 | 0.75 0.62% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 83.23 | 84.61 81.27 | 1.10 1.34% |

| SUGAR #11 WORLD | 16.74 | 16.75 16.33 | 0.27 1.64% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|