Monetary Policy: Is a gradual hike on cards?

MG News | September 19, 2021 at 05:00 PM GMT+05:00

September 19, 2021 (MLN): There is a strong possibility that the State Bank of Pakistan (SBP) could deliver a surprise in the upcoming monetary policy announcement tomorrow. Although most of the market participants aren’t expecting any shock, however, a reasonable amount of individuals think that the monetary policy committee of SBP will give a little jolt in the form of a rate hike.

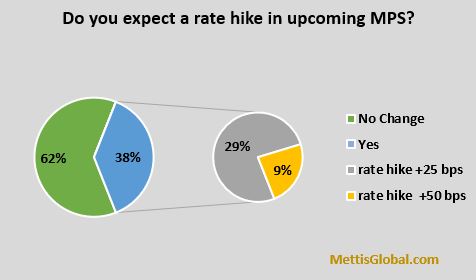

A survey of financial market participants conducted by Mettis Global Pvt Limited also suggests the same as around 62% of the total participants are of the view that the SBP will keep the policy rate at 7% in Sep 2021, monetary policy announcement. In total, 38% of the respondents are expecting a change in the policy rate.

Further bifurcation of this percentage shows that 29% of these participants expect a 25bps rate hike while the remaining 9% expect a hike of 50bps.

For the last 15 months, SBP has been keeping the policy rate unchanged at 7% to support economic growth in the aftermath of the COVID-induced lockdown. Since its last MPC announcement, it has been noticed that most of the variables that SBP had highlighted as upside risks to its inflation forecasts have moved adversely which include higher than expected rise in global commodity prices, unfavorable exchange rate movement, unexpected fiscal expansion, and rise in PDL and domestic energy prices. The unpleasant movement of these variables is clearly indicating a potential violation of the 7-9% inflation target range and 2-3% (as % of GDP) current account deficit target range, to change the policy of interest rates.

Meanwhile, it is important to note that SBP has been providing forward guidance on monetary policy in MPS since January 2021 and at its last MPS in July’21 it stated that in the absence of unforeseen circumstances, monetary policy will remain accommodative in the near term, and any adjustments in the policy rate to be measured and gradual to achieve mildly positive real interest rates over time. However, if signs emerge of demand-led pressures on inflation or of vulnerabilities in the current account, the MPC noted that it would be prudent for monetary policy to begin to normalize through a gradual reduction in the degree of accommodation.

Now it seems that the conditions that SBP had set for itself to raise the interest rate in the future have been met. First, we have seen that in global markets, barring oil, which is relatively stable since the last MPS, commodity prices have doubled whether it is a Food item, steel, Plastic, or freight costs. Metals are rallying on the back of massive stimulus measures and stricter emission standards. Record low European gas stocks are driving gas prices ahead of the winter season. To make things worse, global container freight costs are averaging four times higher than a year ago.

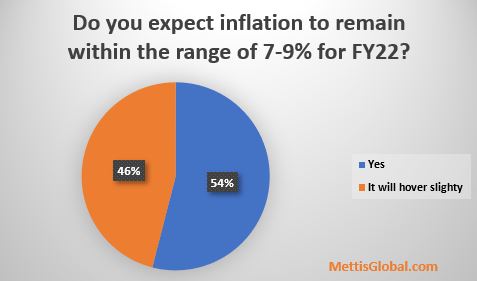

On the inflation front, SPI readings suggest that Sep’21 is likely to witness higher inflation compared to Aug’21 of 8.4% YoY due to increasing pressure on the food index. Additionally, NEPRA has announced fuel price adjustment for Jul’21 of Rs1.37/unit, applicable in Sep’21 across all consumer categories except lifeline consumers as against the previous adjustment of -0.19/unit applicable only on consumers utilizing >300 units. In a survey, 46% of the participants believe average inflation during FY22 will remain within the range of 7-9%, while 54% expect inflation will average slightly higher than this range.

This seems plausible as a hike in energy prices including oil, RLNG, and coal along with PKR depreciation against USD could accelerate the pace of the price hike. Moreover, an upsurge in food prices due to supply constraints could also challenge the inflation pace.

LPG prices are up 4% since mid-July. Petrol and Diesel prices are up 4.9 and 0.9% since last MPS; the government still hasn’t passed on the full impact of an oil price increase and has taken a hit on taxes and levies, Fahad Irfan, an analyst at Alfalah Securities said. The government is charging Petroleum Development Levy (PDL) of Rs5.14 per litre on diesel, last year it was charging around Rs30/lt on petrol and HSD. Under the IMF, Pakistan will most likely have to increase PDL on retail fuels, suggesting that energy inflation is likely to remain high in the near future, he added.

Although at the moment stimulus to economic recovery is crucial for SBP and a symbolic increase i.e., 25-50bps could deeply hit sentiment and may even exacerbate the current situation however, precautionary measures are needed to curtail inflation caused by devaluation in PKR against USD and skyrocket energy and food prices in the international market.

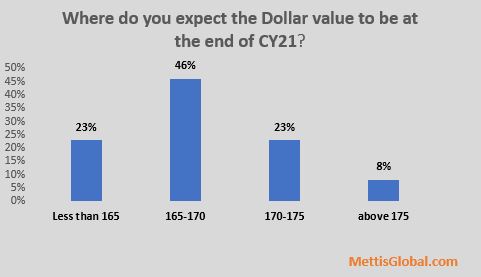

Second, PKR devaluation against the USD despite the rise in FX reserves is fueling import inflation. PKR has lost over 4% to USD since the last MPS as it trades at a rate of 168.19 per USD. A higher import bill is putting pressure on the current account balance; monthly CAD is averaging above $1bn since June -21. As per recently released current account figures by SBP for Aug’21, the deficit reached $1.47bn relative to a surplus of $225mn during SPLY. With oil trading around $70/bbl and record high coal prices, things are unlikely to change on this front. Furthermore, in a survey, 46% of the participants expect a dollar value between Rs165-170 at the end of CY21, while 23% expect it to settle between Rs170-175 and 8% of the respondents think it will go above Rs175. However, 23% of the participants think the dollar value will remain less than Rs165 by the end of CY21.

Mr Mustafa Mustansir, analyst at Taurus Securities said that the ongoing slide of the Rupee reflects short-term pressures due to various reasons including advance booking of LCs by importers; USD buying from Pakistan due to shortage in Afghanistan; switching from prize bonds (September 30, last date to surrender PKR 40,000 prize bonds). However, soaring trade deficit and continuing increase in international commodity prices are also factors contributing to the Rupee’s slide, but these were already built into expectations earlier. The SBP has already projected at a 2-3% CAD for FY22. Elsewhere, the Real-Effective Exchange Rate (REER) as of Jul’21 also indicated that the Rupee was fairly valued.

On the fiscal side, Pakistan posted a primary deficit of 1.4% of GDP in FY21 vs 1.8% in FY20. Under Shaukat Tarin, the focus would remain on economic growth. Fiscal policy would remain expansionary, over the next two years, as Pakistan nears elections. In this backdrop, monetary policy should remain tight and a strong case for a 25bps hike in policy rates can not be ruled out, Fahad Irfan, from Alfalah securities said.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,310.28 434.73M | -0.07% -119.74 |

| ALLSHR | 109,402.32 910.03M | 0.21% 233.65 |

| KSE30 | 54,005.86 184.89M | -0.47% -257.39 |

| KMI30 | 255,725.19 167.56M | 0.03% 73.46 |

| KMIALLSHR | 70,216.28 547.59M | 0.32% 225.24 |

| BKTi | 52,240.23 69.77M | 0.07% 34.26 |

| OGTi | 35,793.26 17.01M | 1.22% 429.81 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,735.00 | 65,700.00 64,585.00 | -440.00 -0.68% |

| BRENT CRUDE | 86.10 | 86.38 83.33 | 2.55 3.05% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -0.90 -0.85% |

| ROTTERDAM COAL MONTHLY | 120.00 | 120.00 119.50 | 3.25 2.78% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 80.72 | 80.98 77.79 | 2.54 3.25% |

| SUGAR #11 WORLD | 16.46 | 16.63 16.29 | 0.01 0.06% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|