July CAD: A Bad Omen for Ailing Economy

Muhammad Ghazanfar Sakrani | August 23, 2023 at 11:00 AM GMT+05:00

August 23, 2023 (MLN): As rightly said, whatever goes up must come down! This saying when taken in the context of the current account balance may haunt the policymakers as depicted by the current account figures for July 2023.

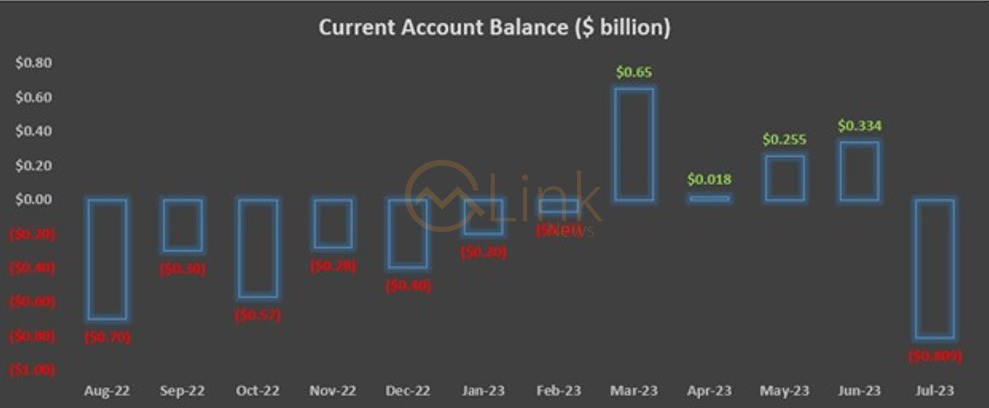

After remaining in a positive trajectory for four consecutive months with the surplus of June touching $334 million taking the four-month cumulative surplus to $1.4 billion (March to June 2023), the current account balance turned adverse.

The current account deficit (CAD) of $809mn in July 2023 is the highest since FY23 and has rang the alarm bells for the already fragile economy.

Compared to FY22 where the current account deficit reached a whopping $17.5bn, the deficit in FY23 shrank by 85.14% to settle at $2.6bn in FY23. The predominant reason for this meagre deficit was the policy of import restriction.

Amid reserves at nadir and stalemate in talks with IMF, the incumbents pursued import restriction policy. This helped in slashing the trade deficit by 43% to $27.55bn compared to $48.35bn in the same period last year.

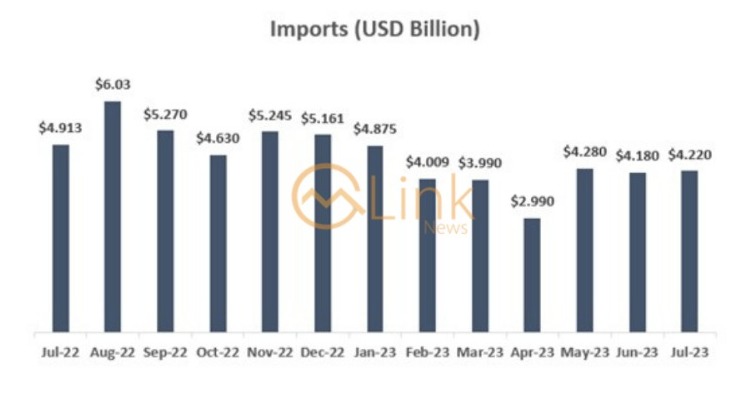

The imports also witnessed a plunge of 31% to settle at $55.29bn compared to $80.13bn in FY22. On the contrary, export earnings didn’t manage to pick up as recorded at $27.74bn, compared to $31.78bn in FY22.

Remittances also slowed down to $27bn from $31.3bn in the same period last year. This shows that the government ensured to restrict import bills in the range of export & remittance earnings.

Amid the ballooning deficit in July 2023 with more to come in the future, one cannot claim that the current account deficit was unprecedented. One of the conditions of the IMF was to lift the curb on imports.

This was bound to pressurize the external account position of the country and result in mounting deficits.

The clearing of the import backlog will aggravate the external account position at a time when exports are not accelerating and the remittances are also muted with many overseas residents preferring to send money through informal banking channels.

Though the imports were recorded at $4.2bn in July 2023, the decline in exports and remittances by 12.7% and 7.3% respectively resulted in the current account deficit.

Ceteris paribus, the external account position of the country is bound to get uglier. To add fuel to the fire, the prices of crude oil in the international market are also surging.

The OPEC+ crude protection is at its lowest since August 2021 following the decision of Saudi Arabia to extend oil cuts. Any rebound in the Chinese economy is set to uplift the prices further in the international market which has already rallied to three months high on July 31.

The import bill of the petroleum group made up almost 22% of the total import bill in July. Any increase would prove to be elastic for the country’s import figures and detrimental to the economy.

The pressure on the external account position will result in currency depreciation. The PKR has already crossed 300/$.

It is also bound to test the resilience of reserves position which are precarious and rely on funding from the fund and other bilateral and multilateral sources.

The depreciating currency is not able to attract remittances. In case the imports revive to a per month average of $6bn with the status quo in export and remittances figures from the current level, the situation may be daunting!

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 136,502.54 259.91M |

1.64% 2202.77 |

| ALLSHR | 85,079.90 838.35M |

1.26% 1061.74 |

| KSE30 | 41,552.62 97.27M |

1.81% 738.33 |

| KMI30 | 193,330.76 84.69M |

0.39% 741.60 |

| KMIALLSHR | 56,315.31 366.02M |

0.43% 243.06 |

| BKTi | 38,498.08 37.91M |

4.13% 1526.33 |

| OGTi | 28,138.38 5.66M |

-0.36% -101.89 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 120,260.00 | 123,615.00 118,675.00 |

1730.00 1.46% |

| BRENT CRUDE | 69.16 | 71.53 69.08 |

-1.20 -1.71% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

0.25 0.26% |

| ROTTERDAM COAL MONTHLY | 106.50 | 106.60 106.50 |

-2.20 -2.02% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 66.92 | 69.65 66.84 |

-1.53 -2.24% |

| SUGAR #11 WORLD | 16.31 | 16.67 16.27 |

-0.26 -1.57% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|