IMF flags growth risks for Pakistan after steep US tariffs

MG News | May 18, 2025 at 12:21 PM GMT+05:00

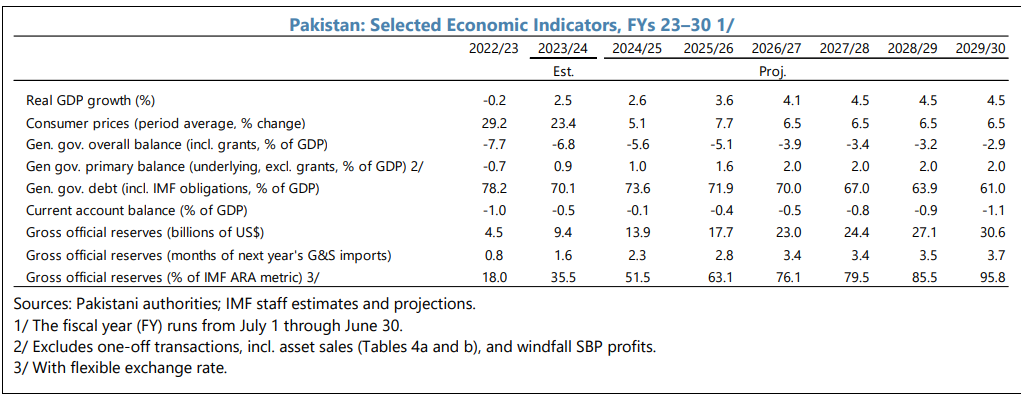

May 18, 2025 (MLN): The International Monetary Fund (IMF) has revised down Pakistan’s near-term macroeconomic projections, citing a weakening growth outlook primarily driven by the imposition of hefty US tariffs on Pakistani exports.

The downgrade also reflected a broader softening in inflation and current account deficit forecasts, offering some temporary relief to external pressures.

The IMF report highlighted that Pakistan is now facing significant uncertainties following the US government’s announcement on April 2, 2025, of steep country-specific tariffs, including a 29% tariff on Pakistani goods.

With the US serving as Pakistan’s largest export destination, particularly for textiles and apparel, the new trade restrictions are expected to have a tangible impact on the country’s GDP, shaving off around 0.3 percentage points from growth in FY26.

Although some reprieve may come through post-announcement negotiations, the global landscape remains fraught.

Major regional competitors like China, Vietnam, Bangladesh, and India have also been hit with substantial tariffs, intensifying competition in an already strained global market.

Beyond the direct trade hit, the IMF warns of a cascade of indirect effects from potential downturns in key trading partners’ economies and reduced remittance inflows to tighter global financial conditions.

The cumulative impact, though moderated by declining commodity prices and a weaker import bill, poses fresh risks to Pakistan’s fragile external stability.

While the inflation outlook is projected to ease slightly due to softer global commodity prices and subdued domestic activity, the report underscores high downside risks.

These include climate shocks, rising geopolitical tensions, a deterioration in remittance flows, and policy slippages as domestic pressures mount for tax breaks and subsidies.

Pakistan’s sovereign spreads have widened significantly since the tariff announcement, though the IMF notes that limited access to global capital markets in the near term may dampen immediate financial repercussions.

However, it stressed that, should capital outflow pressures mount, the rupee must be allowed to adjust freely to maintain external balance.

GDP and Inflation

FY25 growth is revised down to 2.6% based on the weaker activity in H1 and broader global uncertainty, but the recent monetary easing is expected to support an acceleration in FY25H2 and beyond.

FY25 inflation is also revised down, although it is projected to increase notably in the coming months due to adverse base effects, with a durable return to the target range (5–7%) expected during FY26 provided policy remains appropriately tight.

Balance of Payments

The current account deficit (CAD) for FY25 is now projected at about $0.2bn (0.1% of GDP), helped by resilient exports and a stronger remittance outlook, as improved macro and FX stability has supported a rebound in remittance inflows through formal channels.

Over the medium term, the CAD is expected to widen modestly to around 1% of GDP as imports rebound. Gross international reserves are expected to continue to strengthen, supported by financing committed by multilateral and bilateral creditors, as well as prospective RSF disbursements ($1.3bn).

Access to external commercial financing is expected to remain limited during the program, with a small “Panda” bond issuance anticipated in FY26, ahead of a gradual return to the Eurobond/Global Sukuk market assumed in FY27, reflecting a restoration of policy credibility.

Fiscal

The FY25 primary deficit target is within reach, although reflecting the anticipated lower nominal GDP in FY25, nominal tax revenues have been revised down, and efforts to accelerate revenue collection will continue in the coming months.

Offsetting expenditure savings are expected to deliver the programmed FY25 nominal EFF primary balance. Ongoing revenue mobilisation and spending rationalisation efforts, including with considerable CD assistance, are expected to support the fiscal path for FY26 and beyond.

Public debt

Under the baseline, public debt remains sustainable over the medium-term. Notwithstanding the continuation of fiscal consolidation and progress with lengthening maturities of domestic debt, near-term risks of sovereign stress remain high, reflecting Pakistan’s very large gross financing needs and past challenges in obtaining external financing.

Copyright Mettis Link News

Related News

_20260101112329999_0153db_20260209062258909_9180ec.webp?width=280&height=140&format=Webp)

_20251003092603298_af0c50_20251010094012153_327c07.webp?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 154,421.43 202.93M | -0.92% -1437.05 |

| ALLSHR | 92,487.78 401.80M | -0.96% -898.05 |

| KSE30 | 47,322.74 112.52M | -1.11% -528.79 |

| KMI30 | 221,927.00 101.40M | -0.80% -1792.09 |

| KMIALLSHR | 59,889.41 199.88M | -1.08% -652.12 |

| BKTi | 44,127.70 34.85M | -1.99% -894.82 |

| OGTi | 31,715.42 8.74M | -2.31% -748.93 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 70,600.00 | 71,145.00 69,345.00 | -225.00 -0.32% |

| BRENT CRUDE | 98.34 | 101.59 95.20 | 6.36 6.91% |

| RICHARDS BAY COAL MONTHLY | 99.40 | 0.00 0.00 | -10.20 -9.31% |

| ROTTERDAM COAL MONTHLY | 124.50 | 124.60 123.85 | 3.10 2.55% |

| USD RBD PALM OLEIN | 1,083.50 | 1,083.50 1,083.50 | 0.00 0.00% |

| CRUDE OIL - WTI | 93.66 | 97.19 88.61 | 6.41 7.35% |

| SUGAR #11 WORLD | 14.37 | 14.49 14.12 | 0.12 0.84% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|