CY24 Review: PSX Living the Dream

Nilam Bano | January 01, 2025 at 05:20 PM GMT+05:00

January 01, 2025 (MLN): Investors who dared to believe in the potential of the local bourse have hit the jackpot, enjoying a jaw-dropping 84.34% return on the benchmark KSE-100 index in CY24, compared to a 54.5% return in 2023.

Surging with unmatched energy and marking new highs, the index closed the year at 115,127 points, marking a year’s high of 117,039.18 on Dec 17, 2024, and a low of 59,191.86 on Feb 19, 2024.

In USD terms, the index gave a massive return of 86.53% in CY24, compared to 24.11% in CY23.

Economic stability including, corporate profitability, and investor-friendly reforms by the government remained the major factors behind this stellar performance.

The easing monetary cycle, which improved liquidity and facilitated funds flowing towards the equity market, also played a vital role.

Moreover, economic stability would have been a distant dream for Pakistan without the IMF program. Thus, the continuation of the IMF program significantly boosted investor confidence.

Pakistan has successfully secured a $7 billion Extended Fund Facility (EFF) from the Fund. Right after this deal, the lender emphasized the importance of shifting away from the state-led growth model that has long dominated Pakistan’s economic landscape.

It urged the need to enhance the business environment, promote freer competition, and create a level playing field for all stakeholders to reverse the decline in living standards.

The Monetary Policy Committee (MPC) of the State Bank of Pakistan (SBP) has reduced the policy rate by 200 basis points to 13%, in line with market expectations.

The reduction was the fifth in a row, bringing the total decrease since June 2024 to 900bps as a slowdown in inflation gives policymakers room to continue monetary easing in a bid to spur growth.

2024 witnessed a gradual decline in inflation that peaked at 38% in May 2023 but fell to 4.1% by December 24.

Meanwhile, the country posted a fourth consecutive current account surplus in November this year, a surplus of $729 million.

On a cumulative basis, the current account surplus in 5MFY25 was recorded at $944m, showing an increase of 156.3% when compared to the deficit of $1.68bn in 5MFY24.

Driven by greater use of formal channels, strong remittances were a key feature for 2024, surging by 29.08% in November to $2.915 billion, compared to $2.259bn in the same month of last year.

On a cumulative basis, in 5MFY25, the total remittances stood at $14.766bn as compared to $11.053bn worth of inflows received in 5MFY24, depicting a rise of 33.59%.

Foreign exchange reserves have risen to $11.85 billion as of the week ending December 20, 2024. The Governor of the SBP expects the country's foreign exchange reserves to increase to $12 billion by March 2025 and $13 billion by the end of FY25.

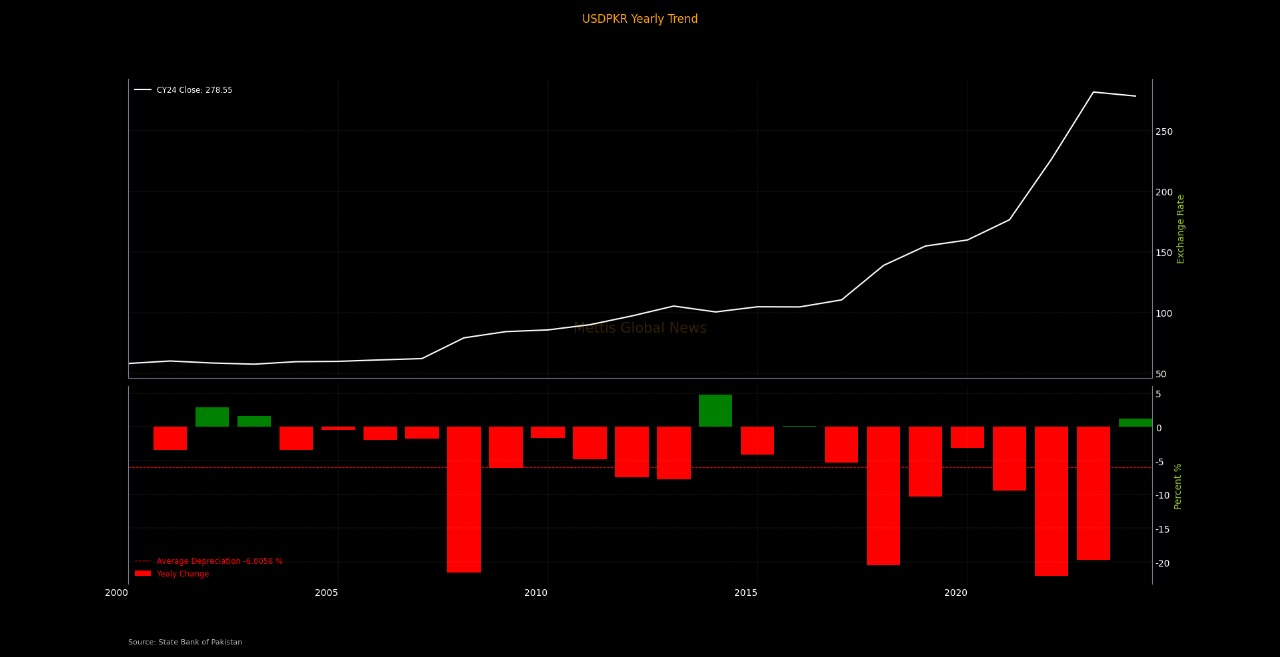

Owing to the aforementioned factors, the local unit has also stabilized which has strengthened investors’ confidence.

In CY24, the Pakistani Rupee has staged a notable recovery, achieving a 1.3%YoY appreciation against the US dollar.

Thanks to government policies and SBP measures that led the gap narrowed between interbank and open market rates.

Following the ease in monetary cycle, fixed income yields have been declined, making equity investments more attractive led the capital directed towards the stock market.

On January 10, 2024, the cutoff yields for 3-month, 6-month, and 12-month T-bills were 20.9996%, 20.9601%, and 20.8449%, respectively, during a T-bill auction. However, in the final auction of 2024, the cutoff yields stood at 11.9999% for 3-month T-bills, 11.9949% for 6-month T-bills, and 12.2977% for 12-month T-bills.

.jpeg)

In addition, the government's clear roadmap for debt management, ambitious privatization efforts, and FDI commitments from friendly countries under the SIFC remained a major glimmer for investors.

Specifically, the Reko Diq project kept the energy sector in the spotlight, and the opportunities to leverage these developments at the PSX continued to hold investors’ interest.

Top Index Movers

Sector-wise, Commercial Banks, Fertilizer, Oil & Gas Exploration Companies, Cement, Oil & Gas Marketing Companies, and Pharmaceuticals were the major contributors with contributions of 13,910.48, 11,047.79, 9,908.79, 2,997.11, 2,541.66, and 2,203.08 points, respectively.

Whereas, Textile Spinning and Synthetic & Rayon made minor dents with -13.44 and -7.05 points, respectively.

.jpeg)

Scrip-wise, FFC, MARI, UBL, OGDC, EFERT, and PPL recorded stellar performances, contributing 6,094.21, 3,951.40, 3,900.99, 2,607.03, 2,144.15, and 2,087.93 points to the index, respectively.

Conversely, PSEL, TRG, EPCL, and NESTLE recorded minor losses with -125.74, -88.90, -60.54, and -39.87 points, respectively.

.jpeg)

FIPI/LIPI

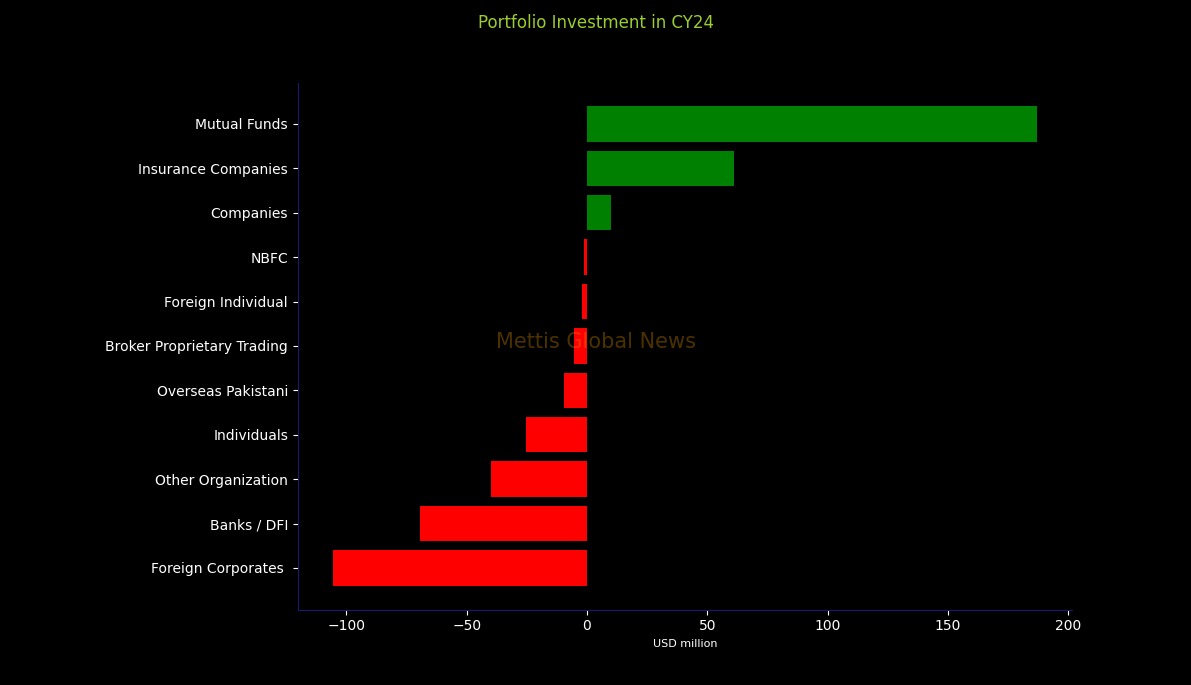

Foreign investors were net sellers during the year, offloading a significant $117m worth of equities.

Flow-wise, the leading sellers were foreign corporates, with a net sale of $105.5m.

Meanwhile, Overseas Pakistanis and foreign individuals sold equities worth $9.34m and $2.11m in the review period.

On the other hand, local investors remained net buyers worth $117m. Among them, Mutual Funds emerged as the dominant buyers, with an investment of $186.83m.

Going forward, the local bourse is poised for a bull run in CY25 supported by easing inflation, lower interest rates, a stable PKR, and improving liquidity.

However, the risk of domestic political instability and international political issues, including tensions in the Middle East that could disrupt commodity prices, may hurt investor sentiment.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,430.02 376.06M | -0.19% -346.57 |

| ALLSHR | 109,168.67 713.66M | -0.13% -139.83 |

| KSE30 | 54,263.26 125.13M | -0.24% -128.56 |

| KMI30 | 255,651.73 86.61M | -0.19% -483.04 |

| KMIALLSHR | 69,991.04 446.60M | -0.05% -33.30 |

| BKTi | 52,205.98 60.34M | -0.31% -161.74 |

| OGTi | 35,363.45 11.64M | 0.17% 60.63 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 65,000.00 | 65,355.00 65,000.00 | -175.00 -0.27% |

| BRENT CRUDE | 82.38 | 84.44 81.50 | -0.11 -0.13% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 105.50 105.50 | -0.25 -0.24% |

| ROTTERDAM COAL MONTHLY | 116.25 | 117.00 116.25 | -0.10 -0.09% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 77.08 | 78.77 76.53 | -0.21 -0.27% |

| SUGAR #11 WORLD | 16.49 | 16.50 15.49 | 0.92 5.91% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|