CPI Preview: Inflation to Find Steady Ground in 26.4-26.5% Range

Abdur Rahman | October 28, 2023 at 05:10 PM GMT+05:00

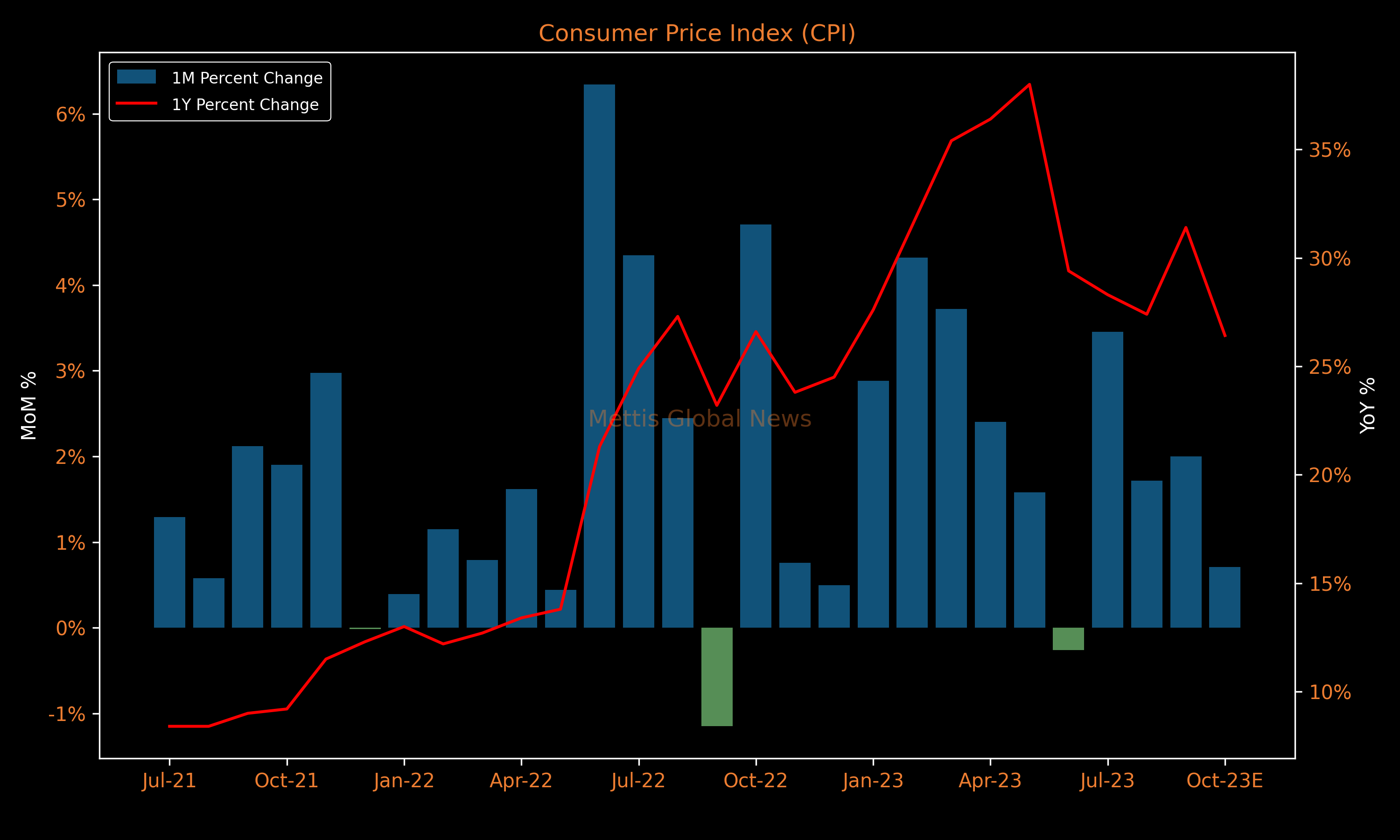

October 28, 2023 (MLN): The surging prices that have continuously been hurting the purchasing power of ordinary citizens in Pakistan are expected to bring relief in October, with headline inflation anticipated to settle at around 26.4-26.5% YoY and 0.7% MoM.

The YoY Consumer Price Index (CPI) is expected to settle lower on the back of the high base effect, coupled with a significantly lower pace of MoM increase as compared to the 12-month average of 3.2% MoM.

Accordingly, this will take the average inflation of 4MFY24 to 28.37% YoY compared to 25.48% YoY in 4MFY23.

| National Consumer Price Index | ||||||

|---|---|---|---|---|---|---|

| Oct 2023E | Indices | |||||

| Weight | YoY | MoM | Oct-23E | Sep-23 | Oct-22 | |

| Headline CPI | 100% | 26.42% | 0.71% | 245.78 | 244.05 | 194.42 |

| Food & Non-alcoholic Bev. | 34.58% | 24.78% | -0.98% | 275.76 | 278.48 | 221 |

| Alcoholic Bev.& Tobacco | 1.02% | 83.59% | -0.26% | 360.22 | 361.16 | 196.21 |

| Clothing & Footwear | 8.60% | 20.34% | 0.81% | 214.78 | 213.05 | 178.48 |

| Housing, Water, Electricity, Gas & Fuels | 23.63% | 20.61% | 3.09% | 200.89 | 194.86 | 166.56 |

| Furnishing & Household Equipment Maintenance | 4.10% | 35.44% | 0.00% | 252.67 | 252.67 | 186.56 |

| Health | 2.79% | 24.27% | 2.00% | 226.76 | 222.31 | 182.47 |

| Transport | 5.91% | 35.87% | 1.64% | 333.49 | 328.11 | 245.44 |

| Communication | 2.21% | 6.35% | -0.60% | 118.94 | 119.66 | 111.84 |

| Recreation & Culture | 1.59% | 55.17% | -0.37% | 253.85 | 254.8 | 163.6 |

| Education | 3.79% | 10.34% | 0.26% | 179.72 | 179.25 | 162.87 |

| Restaurants & Hotels | 6.92% | 32.99% | 1.52% | 256.36 | 252.51 | 192.77 |

| Miscellaneous | 4.87% | 35.18% | 0.00% | 262.92 | 262.92 | 194.49 |

Inflation is expected to slow down primarily due to a notable 1% MoM decline in the food index. This decline can be attributed mainly to lower prices for items such as chicken, fruits, sugar, and pulses.

Conversely, the housing index is projected to experience around a 3% MoM increase, primarily attributed to the quarterly rent adjustment.

Meanwhile transport index is also likely to see an uptick in the MoM change.

It is worth noting that the recent Rs40 per litre decrease will be factored in the next month.

Following a rough year, the economy has started to show some early signs of improvement.

Towards the end of FY23, Pakistan secured a $3 billion Stand-By Arrangement (SBA) from the International Monetary Fund (IMF), which saved the cash-strapped nation that was on the brink of default.

The initial disbursement of $1.2bn under the SBA in July 2023, alongside $3bn bilateral inflows from the Arab countries gave a substantial boost to the depleting foreign reserves held by the country.

Consequently, in the current fiscal year, total liquid foreign reserves have increased by $3.5bn or 38.16%.

Furthermore, the government-backed administrative measures have helped the Pakistani Rupee (PKR) to completely recover all year-to-date losses against the USD and strengthen significantly to 280 per USD.

To recall, Pakistan’s economy faced multifaceted challenges in the latter half of FY22 and throughout FY23 owing to higher global commodity prices, strong global inflation, second-round effects, continuous PKR depreciation, supply chain disruptions due to floods, soaring trade deficits, and rapid reserve depletion.

The impact of these challenges pushed the CPI inflation to a multi-decade high of 29.2% during FY23.

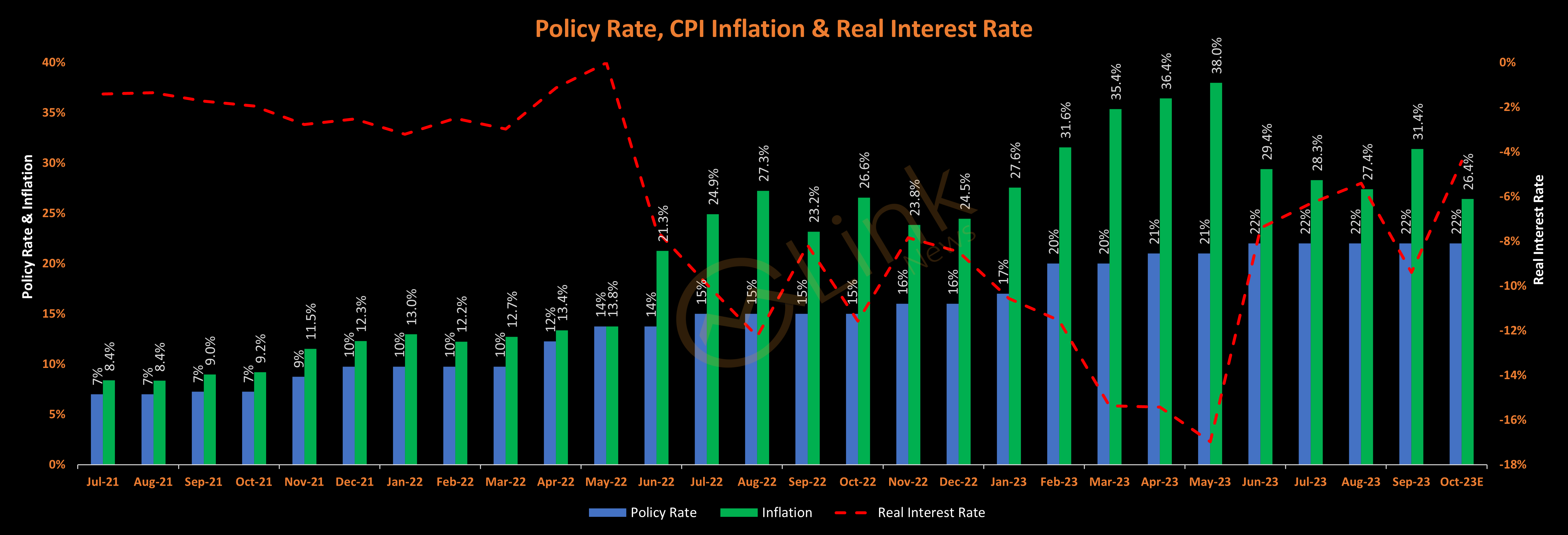

On the policy front, the State Bank of Pakistan (SBP) responded to these escalating macroeconomic challenges by continuing the contractionary monetary policy that it had started in September 2021.

Resultantly, the SBP raised the policy rate by a cumulative 825 basis points (bps) during FY23, on top of a 675 bps increase in the previous fiscal year.

While the cumulative increase in the policy rate since September 2021, when the SBP started contracting the economy is 1,500bps, taking the policy rate from 7% to 22%.

Though the central bank has now kept the policy rate unchanged at 22% since June 2023, foreseeing the downward trend in inflation.

Outlook

In the coming months, inflation is anticipated to start steadily declining on the back of the high base effect, lagged impact of monetary tightening, and other administrative measures.

Additionally, a more steady decrease is projected for the second half of FY24, starting from January.

It is important to mention that unforeseen climate events, volatility in global commodity prices, especially oil, and external account pressures are some important upside risks to the inflation outlook.

Furthermore, the successful completion of the IMF review is crucial. The remaining amount of $1.8bn under SBA is phased over the program's duration, subject to two quarterly reviews, with the next review in November 2023.

The following chart maps out the yearly inflation trajectory if 0.5%, 1%, 1.5%, and the 12-month average of 2.32% MoM is taken.

This is what is referred to as the — high base effect.

At 0.5% and 1% MoM CPI, yearly inflation will drop below the 22% policy rate by January-February 2024.

Moreover, by the end of FY24, with 0.5% and 1% MoM CPI, it will decline towards 12.3% and 17.4% respectively.

Meanwhile, if the last 12-month average of 2.32% MoM is taken, it shows a darker picture.

.png)

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 171,021.20 228.53M | -0.42% -718.25 |

| ALLSHR | 103,836.39 572.65M | -0.41% -422.85 |

| KSE30 | 50,951.99 89.47M | -0.52% -264.77 |

| KMI30 | 240,633.87 93.99M | -0.31% -756.80 |

| KMIALLSHR | 66,572.75 300.61M | -0.28% -185.59 |

| BKTi | 48,673.23 31.18M | -0.70% -343.86 |

| OGTi | 33,702.25 6.35M | -0.61% -205.57 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 64,070.00 | 64,215.00 64,070.00 | -145.00 -0.23% |

| BRENT CRUDE | 98.70 | 101.19 95.13 | -1.99 -1.98% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.55 -1.44% |

| ROTTERDAM COAL MONTHLY | 121.10 | 121.10 121.10 | 0.70 0.58% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 90.47 | 92.83 87.68 | -1.72 -1.87% |

| SUGAR #11 WORLD | 14.76 | 14.79 14.54 | 0.07 0.48% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|