Central banks to keep rates high, slow economies in 2024: Moody's

MG News | November 01, 2023 at 11:31 AM GMT+05:00

November 01, 2023 (MLN): Central banks will keep rates higher for longer to keep a lid on core inflation, which will gradually increase borrowing costs, slow economies and uncover pockets of risk, as revealed in Moody’s outlook report for 2024.

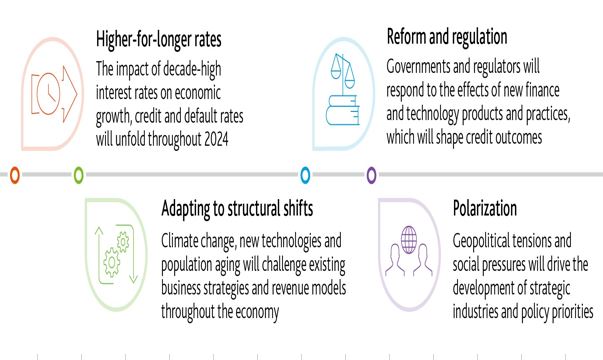

The report highlights four themes that will shape the new normal in 2024. The first theme is that central banks will keep interest rates higher and the impact of decade-high interest rates on economic growth will unfold throughout 2024.

Secondly, structural shifts tied to climate risks, new technologies and demographics will challenge existing business and revenue models.

Additionally, companies will also need to adjust to new reforms and regulations in response to financial and social pressures.

Going forward, polarization at the global level will shape industrial policies and investment decisions. At a domestic level, it will slow policy formation.

Moody’s proprietary indicators suggest financial conditions are near historical averages in the US, but are tightening in the euro area and are weak in emerging markets (EMs).

Falling loan demand and tightening credit standards have led to a large slowdown in bank lending globally. Bond markets in the US and euro area have remained supportive, but financial conditions in EMs have tightened more broadly.

Moreover, as high rates start to bite, the refinancing risks will grow for high-yield corporate issuers next year.

The global default rate will peak at around 4.5%-5% in the first quarter of next year, well below levels recorded in 2007 or during the pandemic.

However, the effects of higher borrowing costs and lower earnings will be felt more by companies with mostly unhedged floating rate debt capital structures rated B2 or lower, and in sectors suffering from weak demand.

The Higher-for-longer rates will also weigh on bank credit.

The inflationary shock will eventually catch up with consumers and companies; combined with higher rates, this will weaken asset quality. Liquidity will also tighten. Net interest margins will decline in the US and China.

Nevertheless, capital levels will remain healthy, and regulatory developments will push them higher in the US.

Debt dynamics are not weighing on most governments' credit quality, but rising interest payments will reduce fiscal space.

Moody expects more frontier market sovereign defaults as a result of tight financial conditions and social risks from high inflation and slow growth

Long-term yields could soften economic activity faster than we expect, lead to asset losses and trigger stress in parts of the financial system.

Flaring of geopolitical risk and oil price spikes can have wide credit effects across EMs. China's economic outlook also remains highly uncertain.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 134,299.77 290.06M |

0.39% 517.42 |

| ALLSHR | 84,018.16 764.12M |

0.48% 402.35 |

| KSE30 | 40,814.29 132.59M |

0.33% 132.52 |

| KMI30 | 192,589.16 116.24M |

0.49% 948.28 |

| KMIALLSHR | 56,072.25 387.69M |

0.32% 180.74 |

| BKTi | 36,971.75 19.46M |

-0.05% -16.94 |

| OGTi | 28,240.28 6.19M |

0.21% 58.78 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 118,140.00 | 119,450.00 115,635.00 |

4270.00 3.75% |

| BRENT CRUDE | 70.63 | 70.71 68.55 |

1.99 2.90% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

1.10 1.14% |

| ROTTERDAM COAL MONTHLY | 108.75 | 108.75 108.75 |

0.40 0.37% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.75 | 68.77 66.50 |

2.18 3.27% |

| SUGAR #11 WORLD | 16.56 | 16.60 16.20 |

0.30 1.85% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|