Weekly Market Roundup

MG News | May 01, 2026 at 03:55 PM GMT+05:00

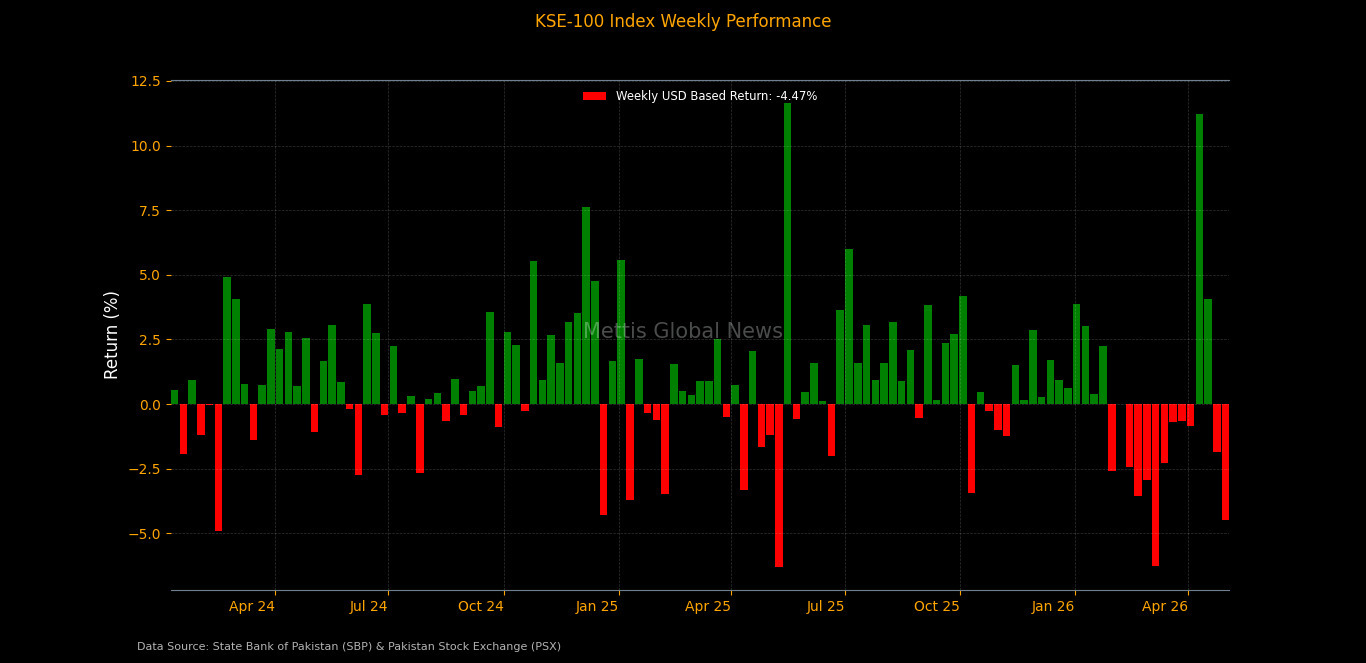

May 01, 2026 (MLN): Pakistan’s equity market extended its decline during the week ended

May 01, 2026, with the benchmark KSE-100 Index closing at 162,994.17, down

sharply from 170,672.04 recorded on April 24, 2026.

The index plunged

7,677.87 points, translating into a 4.50% week-on-week (WoW) decline,

marking an acceleration in selling pressure after the previous week’s

correction.

Investor sentiment

is likely to remain sensitive to geopolitical tensions and developments in

global risk appetite, which may continue to drive volatility in the market._20260501105037204_132b46.jpeg)

Market Capitalization

Total market

capitalization declined significantly in line with the index performance. As of

May 01, 2026, market cap stood at Rs4.695 trillion, compared to Rs4.923tr

on April 24, 2026, marking a decrease of Rs228.25bn or 4.64% WoW.

In USD terms, market

capitalization fell to $16.84bn from $17.65bn in the previous

week, reflecting a notable erosion in overall market value._20260501105020799_1a094a.jpeg)

Dollar-adjusted

returns remained firmly negative, clocking in at -4.47% WoW, compared to

-1.85% in the prior week, indicating a sharp deterioration in investor

returns in both local and foreign currency terms amid intensified market

correction.

On the macroeconomic

front, the State Bank of Pakistan raised Rs1.37tr

through its Market Treasury Bills auction on April 30, 2026, driven by strong

demand across short-term tenors.

However, it rejected all bids in the 10-year floating-rate

Pakistan Investment Bond auction, resulting in zero mobilization from the

long-term instrument.

Pakistan’s total money supply

rose to Rs47.69tr in March 2026, showing a 2.2% MoM and 13.57% YoY

increase, driven mainly by higher currency in circulation and deposit growth.

The uptick highlights continued cash demand amid

inflationary pressures, with currency in circulation posting a notable 16.29%

annual rise.

The State Bank of Pakistan purchased

$728m from the interbank market in January 2026, lower than December’s

$1.02bn but significantly higher than $154m a year ago, showing improved inflow

conditions despite a slight monthly moderation.

The State Bank of Pakistan raised its policy rate by 100

basis points to 11.5% in

April 2026, marking the first increase in nearly three years, as rising

inflation and higher fuel prices worsened the inflation outlook.

The move reflects a shift toward tighter monetary policy,

with the MPC aiming to anchor inflation expectations amid geopolitical risks,

fiscal pressures, and mounting external uncertainties.

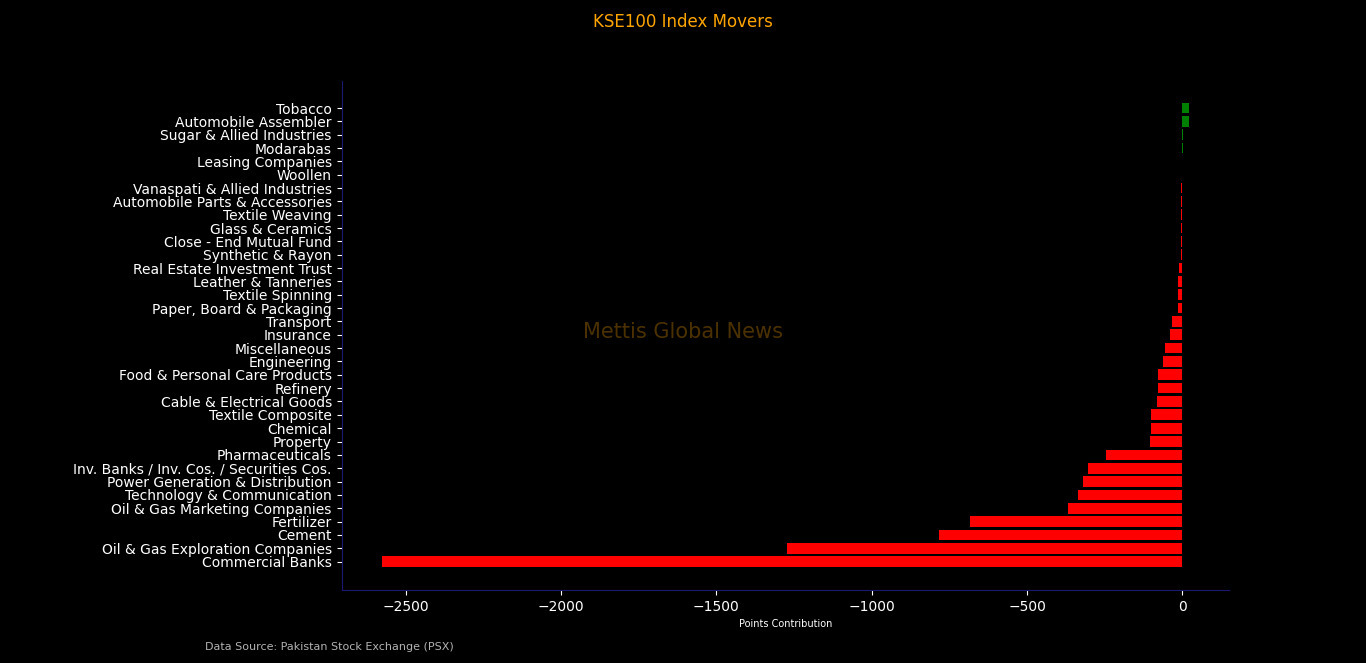

Index Movers

Sector-wise, the decline remained heavily concentrated in index-heavy sectors.

Commercial banks

emerged as the largest drag, shaving off 2,576.60 points, followed by

oil & gas exploration companies (-1,272.13 points), highlighting

pressure on major index drivers.

Cement contributed a

decline of 782.71 points, while fertilizer (-684.36 points) and

oil & gas marketing companies (-368.93 points) further weighed on

the benchmark.

Technology &

communication (-337.05 points) and power generation & distribution (-320.10

points) also remained under pressure, reflecting widespread selling across

cyclical and growth sectors.

Other notable

negative contributors included investment banks/securities (-304.21 points),

pharmaceuticals (-246.92 points), and property (-103.58 points),

reinforcing the broad-based nature of the downturn.

On the positive

side, limited support came from tobacco (+21.13 points) and automobile

assemblers (+19.42 points), along with marginal contributions from sugar

and modarabas, indicating selective resilience in a weak market.

Scrip-wise, the downside was dominated by heavyweights.

United Bank Limited

led the decline, dragging the index by 1,066.79 points, followed by

National Bank of Pakistan (-663.04 points) and Pakistan Petroleum

Limited (-589.15 points).

Other major laggards

included Fauji Fertilizer Company (-562.54 points), Oil and Gas

Development Company (-508.75 points), and Lucky Cement (-339.45

points).

Additional pressure

came from Pakistan State Oil, Engro Holdings, Hub Power Company, Habib Bank

Limited, Mari Petroleum Company, and MCB Bank Limited, reflecting heavy selling

in banking, energy, and cement stocks.

On the upside, gains

remained limited and largely concentrated in automobile names, with Indus Motor

Company leading the pack (+64.61 points), followed by Honda Atlas Cars and

Millat Tractors.

Other contributors

included Pakistan Tobacco Company, Pakistan Oilfields Limited, and Attock

Petroleum Limited, highlighting selective buying in defensive and auto

segments._20260501104954123_5d4907.jpeg)

FIPI / LIPI

Foreign investment flows showed a modest net inflow during the week.

Under Foreign

Institutional Portfolio Investment (FIPI), overseas Pakistanis remained the key

buyers with a net inflow of Rs1.36bn ($4.86m).

However, foreign

corporates were net sellers, recording an outflow of Rs757.40m ($2.71m),

while foreign individuals posted a marginal inflow of Rs0.14m.

Overall, FIPI

recorded a net inflow of Rs598.42m ($2.14m), indicating slight foreign

support despite broader market weakness.

On the domestic

side, Local Portfolio Investment (LIPI) activity remained mixed.

Individuals emerged

as the largest buyers with a strong net inflow of Rs7.65bn, followed by

companies (+Rs398.93m) and banks & DFIs (+Rs326.39m),

providing liquidity support to the market.

On the flip side,

mutual funds led the selling with a significant net outflow of Rs7.97bn,

while broker proprietary trading (-Rs876.26m) and insurance companies (-Rs176.11m)

also contributed to the selling pressure.

Other participants

remained largely neutral, indicating a cautious stance across institutional

investors.

In the debt

market, activity remained relatively subdued, with individuals showing net

inflows, while mutual funds recorded outflows, reflecting selective

reallocation across asset classes._20260501104956384_d6bc8f.jpeg)

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

_20260711124603464_8ff65f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,210.00 | 64,680.00 62,605.00 | -875.00 -1.37% |

| BRENT CRUDE | 78.44 | 79.80 77.28 | 2.43 3.20% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.76 | 75.08 72.61 | 2.35 3.29% |

| SUGAR #11 WORLD | 14.71 | 14.98 14.65 | -0.17 -1.14% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|