Weekly Market Roundup

MG News | April 04, 2026 at 07:28 PM GMT+05:00

April 4, 2026 (MLN): Pakistan’s equity market

remained under pressure for the tenth consecutive week, as the benchmark

KSE-100 Index closed at 150,398.71 on 3 April 2026, down from 151,707.52

recorded on 27 March 2026. The index shed 1,308.81 points, translating

into a 0.86% week-on-week (WoW) decline.

Investor sentiment weakened due to rising US-Iran

tensions, which spurred fears of prolonged conflict and triggered oil

price spikes, creating uncertainty and broad-based selling in the market._20260404122931392_e75ac4.jpeg)

Market Capitalization

Total market capitalization declined in line with the

benchmark index. On 3 April 2026, market cap stood at Rs4.376 trillion,

compared to Rs4.403tr on 27 March 2026, marking a contraction of Rs27.98

billion or 0.64% WoW.

In USD terms, market capitalization fell to $15.68bn

from $15.77bn a week earlier. _20260404122910855_ce9641.jpeg)

Dollar-adjusted returns also deteriorated slightly, moving

from -0.6480% to -0.8376% WoW, showing a faster pace of decline on a

dollar basis._20260404122900144_197244.jpeg)

On the macroeconomic front, Pakistan’s

trade deficit narrowed to $2.73bn in March 2026, down 9.36% MoM due to a

sharper fall in imports.

However, the deficit widened on a yearly and cumulative

basis, highlighting persistent external sector pressures.

SBP raised Rs828.63bn

in its latest auction, with the bulk coming from Treasury Bills amid strong

demand, particularly in the 3-month tenor.

Pakistan’s

economy grew by 3.89% in Q2 FY26, driven by a strong rebound in the

industrial sector despite continued weakness in agriculture.

Pakistan’s CPI

inflation rose to 7.3% YoY in March 2026, with a sharp monthly acceleration

indicating broadening price pressures across the economy.

SBP

purchased $1.02bn from the interbank market in December 2025, nearly

doubling YoY and signaling strong inflows during the month.

However, cumulative FX purchases in 1HFY26 remained lower

than last year, indicating relatively softer inflow momentum overall.

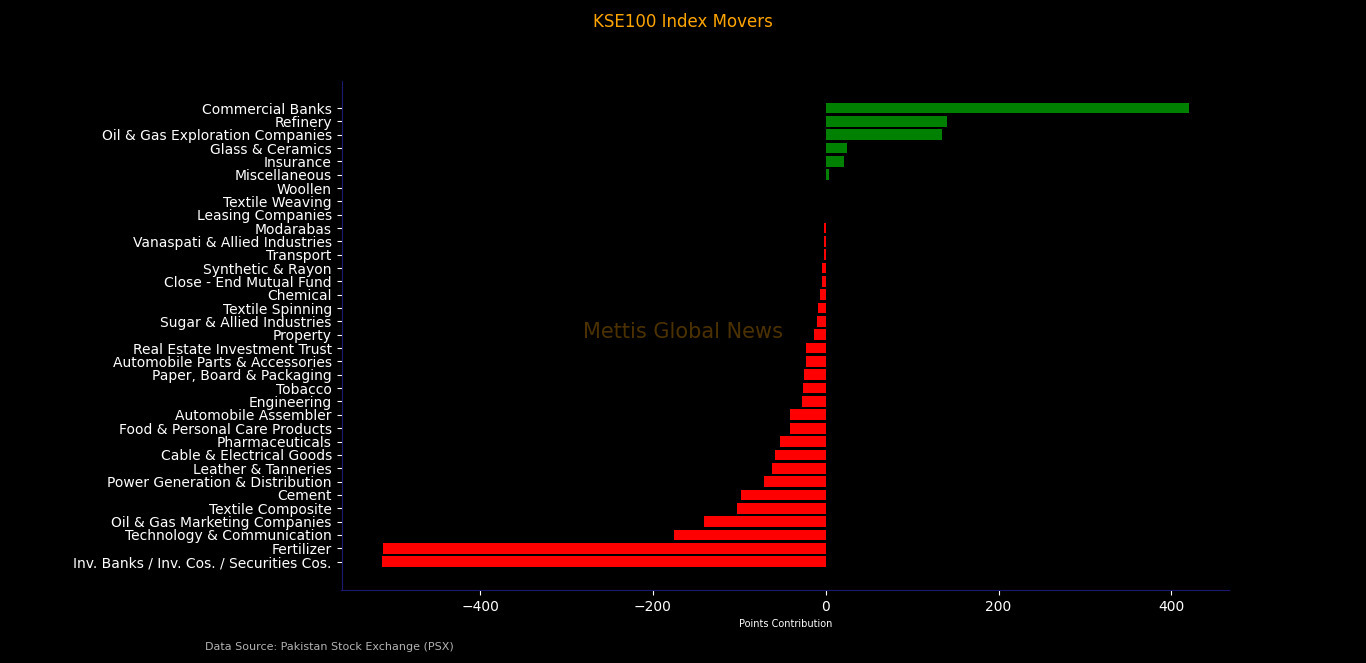

Index Movers

Sector-wise, commercial banks emerged as the largest

positive contributor, adding 420.41 points to the benchmark, supported

by strong performances from MEBL, BAHL, HBL, and BAFL.

Oil and gas exploration companies added 134.31 points,

while refinery stocks contributed 140.55 points. Insurance and glass

& ceramics sectors provided marginal support, adding 21.61 and 24.11 points

respectively.

On the downside, investment banks, investment companies, and

securities companies were the biggest drag, wiping out 513.74 points,

followed closely by fertilizer (-512.77 points) and technology &

communication (-175.73 points).

Oil and gas marketing companies (-140.36 points), textile

composite (-102.52 points), and cement (-98.45 points) also contributed to the

decline.

Power generation & distribution (-71.81 points), leather

& tanneries (-62.66 points), cable & electrical goods (-59.31 points),

pharmaceuticals (-52.93 points), and food & personal care products (-41.30

points) added further pressure.

Other sectors such as automobile assemblers, engineering,

tobacco, paper & packaging, and miscellaneous also weighed on the index,

reflecting broad-based selling across the market.

At the individual stock level, MEBL led the gainers, adding 307.78

points, followed by BAHL (+268.76 points) and HBL (+247.99 points).

Other notable contributors included BAFL (+157.33 points),

LUCK (+133.75 points), OGDC (+110.49 points), ATRL (+104.69 points), and TRG

(+90.63 points).

Additional support came from POL, HMB, MARI, CNERGY, ATLH,

FCCL, NBP, AICL, POWER, MCB, KEL, GHGL, SEARL, PSEL, AKBL, TGL, UPFL, GLAXO,

DCR, SSGC, MTL, AHCL, PABC, HCAR, MUREB, ABL, and BNWM.

Despite these gains, several large-cap stocks remained under

heavy selling pressure, keeping the benchmark subdued.

UBL emerged as the largest drag, erasing 533.88 points,

followed by ENGROH (-478.39 points), FFC (-363.12 points), SYS (-131.02

points), PSO (-116.34 points), MLCF (-94.69 points).

FATIMA (-87.27 points), PPL (-83.22 points), PTC (-81.74

points), HALEON (-20.67 points), KOHC (-18.94 points), NML (-19.54 points),

MEHT (-14.07 points), ILP (-28.49 points), and other index-heavy stocks,

highlighting persistent selling across major sectors.

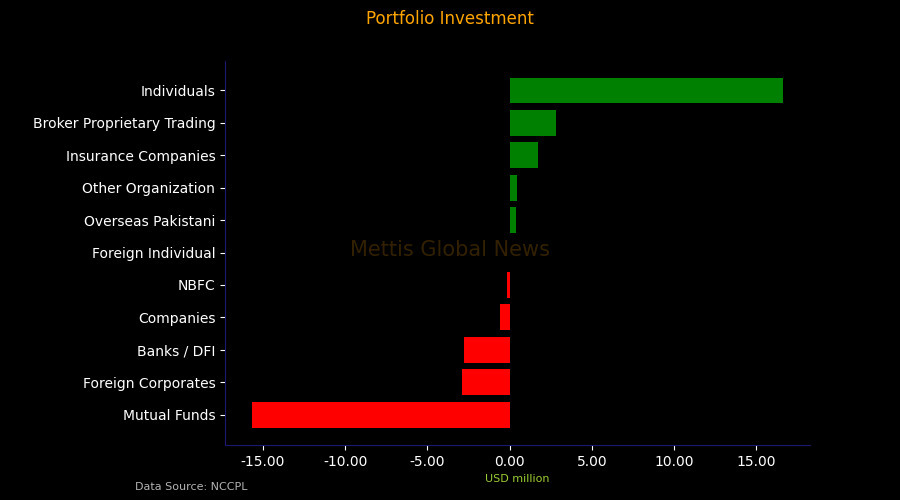

FIPI / LIPI

Foreign investment flows continued to weigh on the market.

Under Foreign Institutional Portfolio Investment (FIPI), foreign

investors remained net sellers with an outflow of Rs697.11m ($2.50m).

The majority of the selling came from foreign corporates,

which offloaded Rs806.46m, while overseas Pakistanis provided modest

support with net buying of Rs109.17m.

Foreign individuals remained largely neutral, contributing a

minor net inflow of Rs182,498.

Local investors absorbed the foreign outflow, resulting in a

matching net inflow of Rs697.11m ($2.50m) under Local Portfolio

Investment (LIPI).

Among local participants, individuals emerged as the largest

buyers with net purchases of Rs4.64bn, followed by broker proprietary

trading desks (+Rs786.95m) and insurance companies (+Rs492.74m).

Conversely, mutual funds (-Rs4.38bn), banks & DFIs (-Rs764.24m),

NBFCs (-Rs45.91m), and companies (-Rs165.87m) remained net sellers.

Copyright Mettis Link News

Related News

_20260529073616622_a5048c.jpeg?width=280&height=140&format=Webp)

_20260711124603464_8ff65f.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 179,927.05 365.01M | -1.27% -2314.73 |

| ALLSHR | 109,270.69 838.76M | -1.19% -1312.98 |

| KSE30 | 53,705.71 89.34M | -1.33% -726.00 |

| KMI30 | 253,531.92 109.38M | -1.32% -3382.29 |

| KMIALLSHR | 70,152.63 543.97M | -1.25% -888.68 |

| BKTi | 50,997.50 18.73M | -1.38% -715.26 |

| OGTi | 36,216.08 8.18M | -1.21% -443.50 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,210.00 | 64,680.00 62,605.00 | -875.00 -1.37% |

| BRENT CRUDE | 78.44 | 79.80 77.28 | 2.43 3.20% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -1.15 -1.08% |

| ROTTERDAM COAL MONTHLY | 118.00 | 0.00 0.00 | 0.65 0.55% |

| USD RBD PALM OLEIN | 1,135.00 | 1,135.00 1,135.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 73.76 | 75.08 72.61 | 2.35 3.29% |

| SUGAR #11 WORLD | 14.71 | 14.98 14.65 | -0.17 -1.14% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|