Pakistan’s transition from: Debt Free to Debt Sustainability

_20260424113129482_5b110f.jpeg?width=950&height=450&format=Webp)

Abu Ahmed | April 23, 2026 at 05:29 PM GMT+05:00

April 23, 2026 (MLN): “Retire the debt, save the country” once a popular political slogan-now a relic of the past. The vision of a debt-free nation has shifted from a plausible goal to a distant aspiration, drifting further out of reach over time, much like an ever-expanding universe.

This realization led to recasting of the narrative toward a more pragmatic concept of “debt sustainability”: not eliminating debt, but to sustain it responsibly, and leverage it as a tool for economic growth.

To this end, maintaining an optimal balance between the maturity structure and the borrowing cost of outstanding debt is essential. The former entails lengthening the maturity profile, while the latter focuses on keeping borrowing costs within sustainable limits. This balance is achieved by tilting the debt portfolio toward longer-term instruments.

As the average maturity lengthens, the debt profile becomes more stable: rollover frequency declines, and the risk of refinancing obligations at elevated rates is significantly reduced.

Has Pakistan aligned itself with this evolving paradigm? Examination of Domestic debt management offers a compelling lens through which to assess any strategic shift in maturity structure.

Unlike external debt, whose terms are significantly shaped by creditors and global financial conditions, domestic debt lies largely within sovereign control, making it a clearer expression of the government’s fiscal strategy and policy intent in advancing debt sustainability.

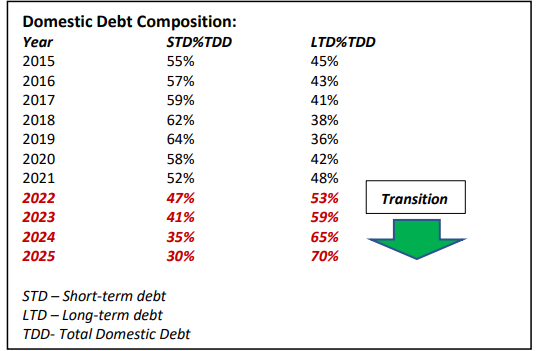

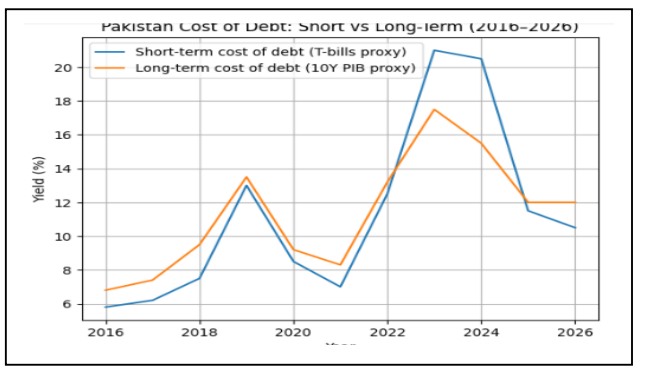

State Bank of Pakistan data shows a clear maturity transformation in domestic debt profile, from short-term to long-term instruments.

Over the past decade, the share of short-term det has declined from 28% to 16%, while the proportion of long-term debt has increased from 72% to 84%. This structural transformation extended maturity profile of domestic debt from 2.7 years to 3.8 years.

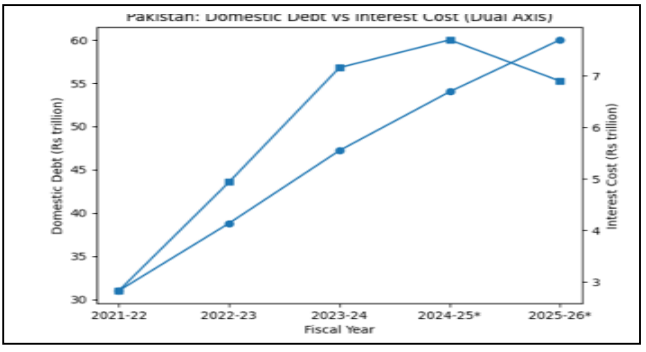

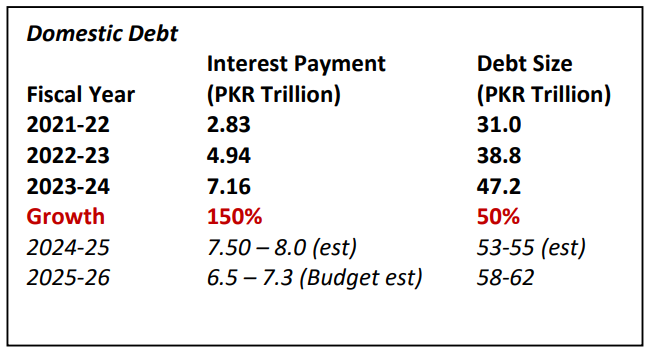

This shift, however, has come at a cost: frequent repricing of maturing debt at elevated interest rates, particularly during the period from 2021 to 2024. A period marked by sharp increase in cost of borrowing across both short & long-term instruments. As per the Federal Budget 2023-24, nearly 60% of government revenue were used in debt servicing.

With approximately 85% to 90% interest payment attributed to domestic servicing, domestic borrowing has emerged as a central source of vulnerability for debt sustainability. In the Budget for the fiscal year 2025-2026, total interest payments are estimated at PKR 8.2 trillion of which PKR 6.5 to 7.3 trillion is allocated as interest payment on domestic debt.

Despite unsustainable debt dynamic in between 2021 to 2024, when interest payment grew to 150% compared to only around 50% growth in domestic debt, Pakistan demonstrated resilience and commitment to debt sustainability by lengthening maturity profile of domestic debt from 2.7 years to 3.8 years, with marginal term-premium on long-term debt.

Despite the clear shift in domestic debt composition toward long-term instruments, debt sustainability remains an elusive for Pakistan. The persistent expansion of the domestic debt stock has altered the fundamental nature of the fiscal deficit-what was once a structurally driven deficit has transformed into an interest-driven deficit.

As a result, a significant portion of new borrowing is directed toward debt servicing rather than to finance economic growth.

_20260423122847476_769df8.jpeg)

What does this transition—from a debt-free narrative to a debt sustainability framework—mean for investors, particularly those in fixed income?

With a policy tilt toward longer-term instruments and rising borrowing needs driven by debt

servicing, Pakistan’s fixed-income landscape is evolving under tight monetary conditions and an

upward shift in term premia. In this environment, a barbell strategy becomes more relevant, allowing investors to exploit short-term rate volatility while capturing structural value at the long

end of the curve.

Copyright Mettis

Link News

Related News

_20260513052023717_7e8bb5.jpeg?width=280&height=140&format=Webp)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 181,430.02 376.06M | -0.19% -346.57 |

| ALLSHR | 109,168.67 713.66M | -0.13% -139.83 |

| KSE30 | 54,263.26 125.13M | -0.24% -128.56 |

| KMI30 | 255,651.73 86.61M | -0.19% -483.04 |

| KMIALLSHR | 69,991.04 446.60M | -0.05% -33.30 |

| BKTi | 52,205.98 60.34M | -0.31% -161.74 |

| OGTi | 35,363.45 11.64M | 0.17% 60.63 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 65,495.00 | 65,500.00 64,975.00 | 320.00 0.49% |

| BRENT CRUDE | 84.82 | 84.97 83.55 | 1.27 1.52% |

| RICHARDS BAY COAL MONTHLY | 105.50 | 0.00 0.00 | -0.90 -0.85% |

| ROTTERDAM COAL MONTHLY | 116.25 | 0.00 0.00 | -0.50 -0.43% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 79.25 | 79.43 78.32 | 1.07 1.37% |

| SUGAR #11 WORLD | 16.49 | 16.50 15.49 | 0.92 5.91% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|