PSX's May Magic

MG News | June 01, 2026 at 03:40 PM GMT+05:00

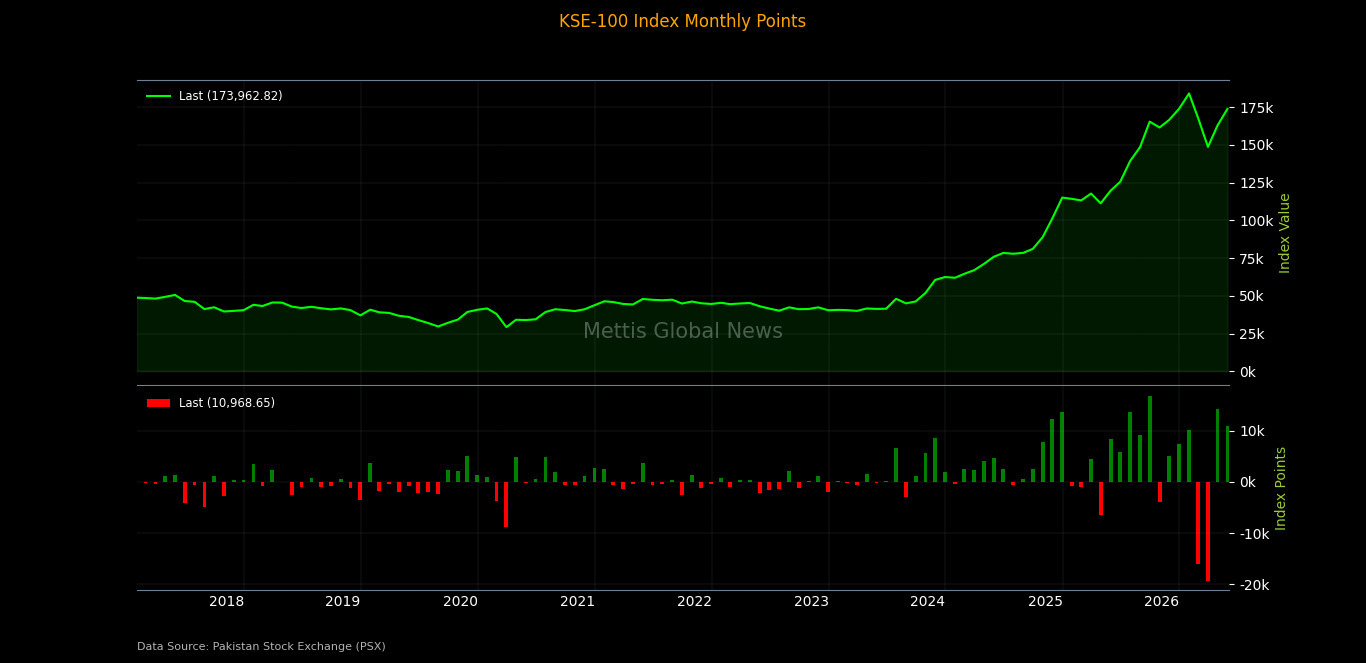

June 01, 2026 (MLN): The KSE-100 Index staged an impressive rally in May 2026, surging 10,969 points, equivalent to a gain of 6.73%, to close the month at 173,963 points.

This marked a significant recovery from the April 2026

closing level of 162,994 points, with the index reclaiming historic highs and

posting its strongest monthly performance in several months.

Compared to April 2026, when the index rose 9.58% (contributing 14,251 points), May's gains were slightly more moderate in percentage terms, yet still commanding given the broader context.

On a year-on-year basis, the index has surged sharply from May 2025's close.

The PKR return heatmap shows that May 2025

registered a 4.96% gain, whereas May 2026 delivered a 6.73% return in PKR terms, underscoring the sustained bullish momentum in Pakistani equities over the

past twelve months.

The primary catalyst for May's rally was progress in US-Iran diplomatic negotiations, with Pakistan playing a constructive facilitating role.

Investor sentiment was further underpinned by a 60-day extension of the US-Iran ceasefire announced towards the end of the month, easing concerns over potential oil supply disruptions.

Trading volumes, however, moderated in the latter part of the month owing to the Eid holidays, with average daily trading volumes falling to 708.6 million shares, a 23.7% decline on a month-on-month basis.

The month's trading pattern was characterised by a strong opening surge in the first week, a mid-month correction, and a late recovery towards month-end, driven largely by ceasefire-extension news.

May 6 was the standout session of the month, with the index posting a single-day gain of approximately 4.23%, adding roughly 7,200 points in a single session.

The rally on this day was primarily driven by euphoria around Pakistan's diplomatic engagement in the US-Iran talks and the broader optimism surrounding the ceasefire.

The index surged from approximately 165,000 to above 171,000 in that session, accompanied by robust volumes of over 500 million shares, the highest volume day of the month.

The sharpest single-day decline occurred on May 18, with the index shedding approximately 2.29%. This sell-off came amid a broader mid-month correction following the sharp rally in early May.

Profit-taking by investors who had accumulated positions during the opening surge was the dominant driver, compounded by a moderation in volumes as market activity slowed ahead of the Eid holidays.

The index briefly touched the

162,000 level before stabilising and recovering in subsequent sessions.

Overall, the month saw 16 advancing sessions and 9 declining sessions, reflecting a broadly positive trading environment underpinned by macro-diplomatic tailwinds.

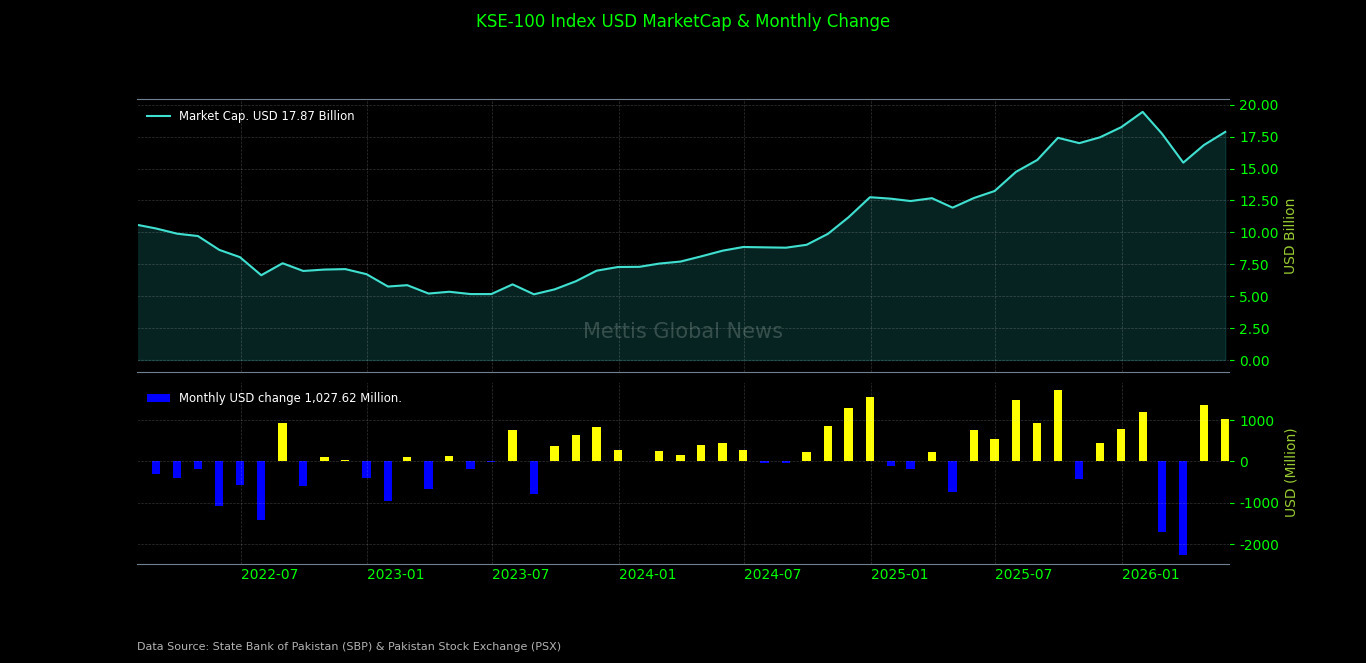

Market Cap:

The KSE-100 Index market capitalisation rose to PKR 4,976.42 billion in May 2026, compared to PKR 4,694.79 billion at the end of April 2026, representing a monthly increase of PKR 281.63 billion.

This month-on-month expansion reflects the broad-based price appreciation across index constituents, particularly in the heavyweight Commercial Banks, Fertilizer, and Oil & Gas Exploration sectors.

On a year-to-date basis for FY26, market capitalisation has grown considerably from PKR 4,316.46 billion at end-March 2026, the low point of the FY26 cycle, emphasizing the meaningful recovery underway in Pakistani equities.

In US dollar terms, the KSE-100 market capitalisation stood at USD 17.87 billion at end-May 2026, up from USD 16.84 billion in April 2026.

This translates to a monthly increase of USD 1.03 billion, driven by index gains. The USD market cap remains significantly recovered from the February and March 2026 lows of USD 17.73 billion and USD 15.46 billion, respectively, when the index underwent a sharp correction.

The improvement in market cap in USD terms is further underpinned by relative rupee stability, with the PKR/USD rate holding around 278.50 at month-end.

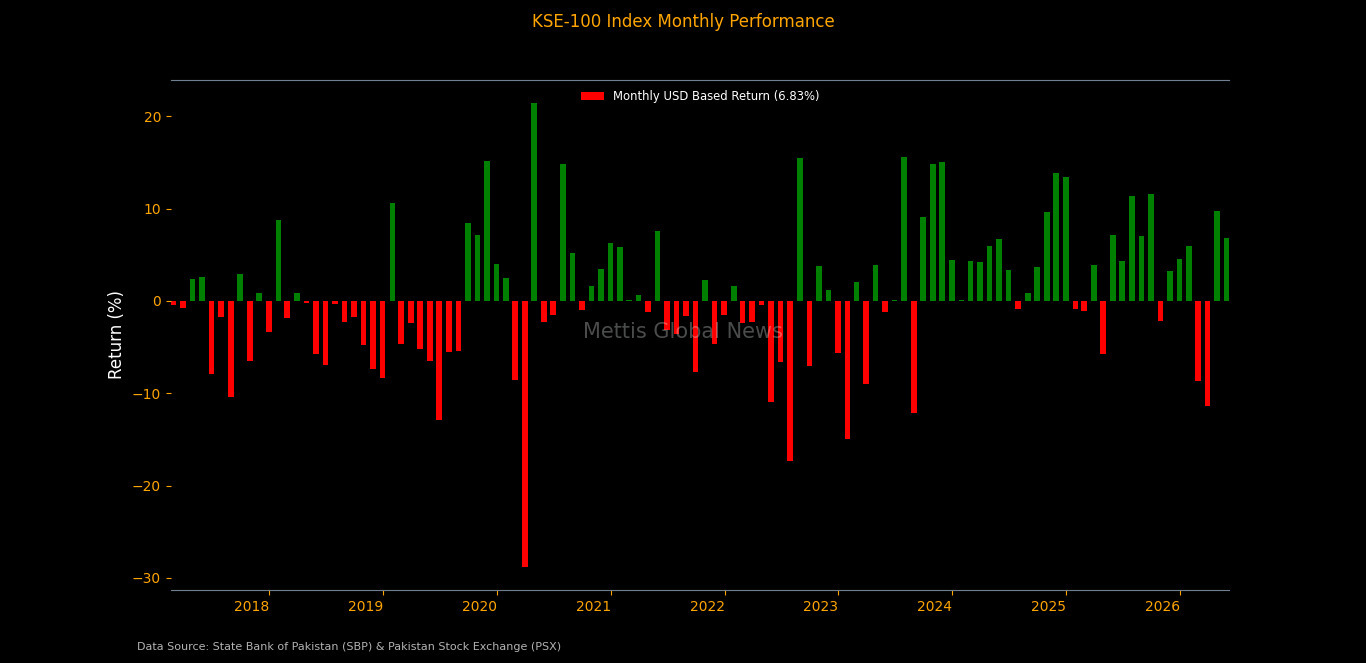

The KSE-100 Index delivered a USD-based return of 6.83% in May 2026, compared to 9.73% in April 2026 and 4.31% in May 2025. The month-on-month moderation from April's strong USD return reflects the relatively smaller absolute index gain in May versus the prior month, as well as marginal rupee depreciation (PKR 278.77 in April to PKR 278.50 in May, practically flat).

On a

year-on-year basis, the USD return has nearly doubled from the 4.31% recorded

in May 2025.

Since the start of FY26 (July 2025), the KSE-100 has delivered a cumulative USD return of 41.09%, highlighting the exceptional performance of the Pakistani market in dollar terms.

This compares favourably to FY25's total USD

return of 57.09% and FY24's 94.44%, with the index continuing to offer

attractive dollar-denominated returns relative to global emerging market peers.

The modest currency impact in May, with the PKR depreciating by roughly 0.10% against the USD during the month, meant that the USD return closely tracked the PKR return of 6.73%.

On the economic front, Pakistan's real GDP grew 3.99% in 3QFY26, supported by broad-based sectoral expansion. The industrial sector led growth at 4.7% YoY, while services grew 4.2% and agriculture expanded 3.0%.

Cumulatively, the LSMI output rose 11% YoY in March 2026, although it declined 9.3% on a MoM basis.

Pakistan's headline CPI inflation accelerated to 11.7% YoY in May 2026, up from 10.9% in April 2026, and substantially higher than the 3.5% recorded in May 2025. On a MoM basis, inflation rose 0.5%, a deceleration from the 2.5% MoM rise in April 2026 and a reversal from the 0.2% MoM decline in May 2025.

The re-acceleration in

inflation warrants monitoring by the State Bank of Pakistan in its monetary

policy deliberations.

Pakistan recorded a current account deficit of USD 252 million during 10MFY26, compared to a surplus of USD 1,662 million in the same period last year.

In April 2026, the deficit widened

to USD 324 million, from a surplus of USD 1,134 million in March 2026 and a

deficit of USD 12 million in April 2025.

The budget deficit for 9MFY26

stood at PKR 856 billion, equivalent to 0.7% of GDP. FBR revenue reached PKR

9,306 billion, reflecting a 10% YoY increase.

Pakistan successfully

priced its inaugural USD 250 million 3-year Panda Bond in China at a coupon

rate of 2.5%. The offering was oversubscribed more than five times, reflecting

strong Chinese investor confidence in Pakistan's credit story.

Workers' remittances rose 11% YoY to USD 3.5 billion in April 2026 (vs. USD 3.2 billion in April 2025), though declined 8% MoM. Cumulatively, remittances increased 8% YoY to USD 33.9 billion in 10MFY26.

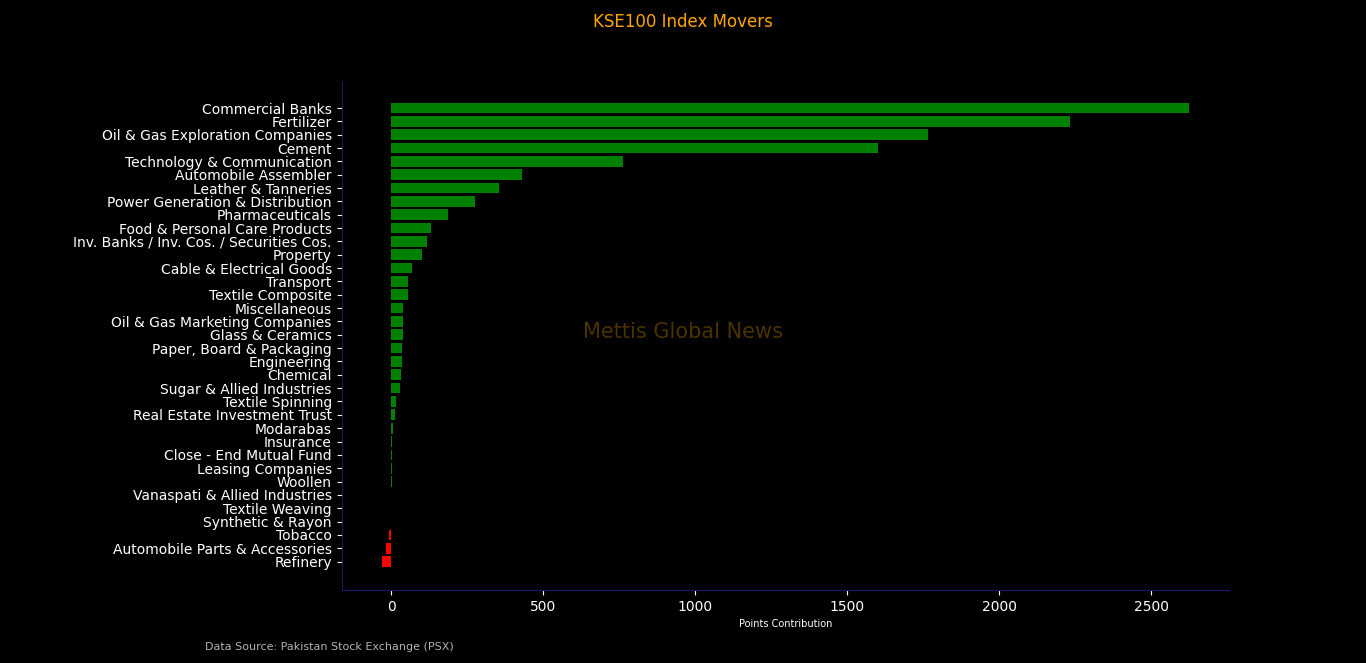

The May 2026 rally was driven by broad-based sector participation, with all major heavyweight sectors recording positive contributions. Commercial Banks led the charge, contributing 2,623.92 index points, followed by Fertilizer (+2,230.97 pts) and Oil & Gas Exploration Companies (+1,764.24 pts).

The Cement sector added 1,599.70 points, while Technology & Communication contributed 762.72 points.

On the negative side, only Refinery (-31.70 pts), Automobile Parts & Accessories (-18.64 pts), and Tobacco (-7.40 pts) dragged on the index.

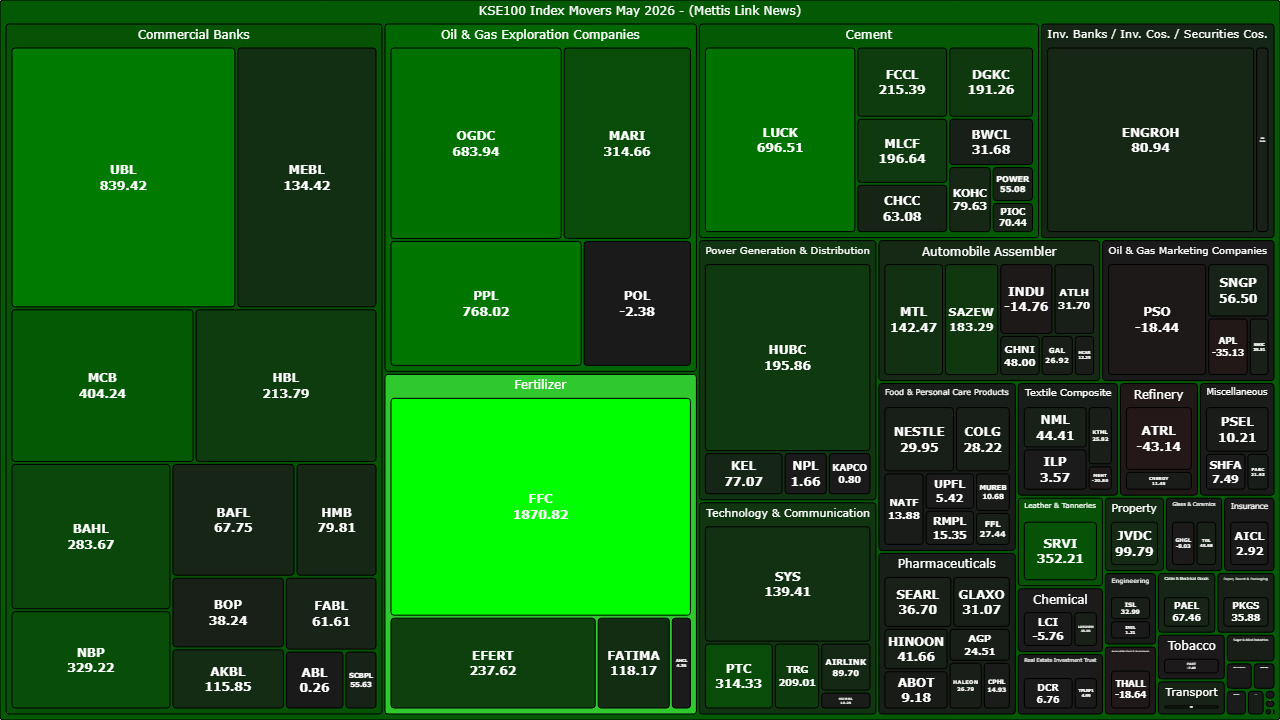

Scrip-wise:

FFC (Fauji Fertilizer Company) was the top index contributor in May, adding a remarkable 1,870.82 points, the single largest individual scrip contribution of the month, driven by strong urea demand data and improving earnings outlook.

UBL came second with 839.42 points, underscoring the dominance of Commercial Banks in the month's rally. PPL added 768.02 points amidst improved E&P sector sentiment tied to easing oil supply concerns.

LUCK (Lucky Cement) and OGDC rounded out the top five, contributing 696.51 and 683.94 points, respectively.

Foreign portfolio flows recorded a net outflow of USD 17.08 million in May 2026 (Grand Total, equity + debt).

On the equity side, Foreign Corporates were the dominant sellers, registering a net sell of USD 20.79 million, while Foreign Individuals also sold, albeit marginally at USD 0.06 million.

The only net buyer within the FIPI universe was Overseas Pakistanis, who injected a net USD 3.68 million into equities, partially cushioning the foreign corporate sell-off. Total FIPI equity net outflow amounted to USD 17.16 million.

Local institutions were the dominant net buyers in May 2026, absorbing the foreign sell-off with a total equity net inflow of USD 17.16 million. Insurance Companies led local buying with a net inflow of USD 12.83 million, the largest single category of net buying in the month, reflecting the sector's appetite for equity accumulation at attractive valuations.

Broker Proprietary Trading added USD 5.53 million, while Other Organizations and NBFCs contributed USD 2.14 million and USD 1.28 million, respectively. Individuals were marginal net buyers (USD 0.60 million).

On the sell side, Companies were the largest local net sellers (USD 3.88 million), followed by Banks/DFI (USD 0.93 million) and Mutual Funds (USD 0.41 million).

_20260601103205386_1e01a5.jpeg)

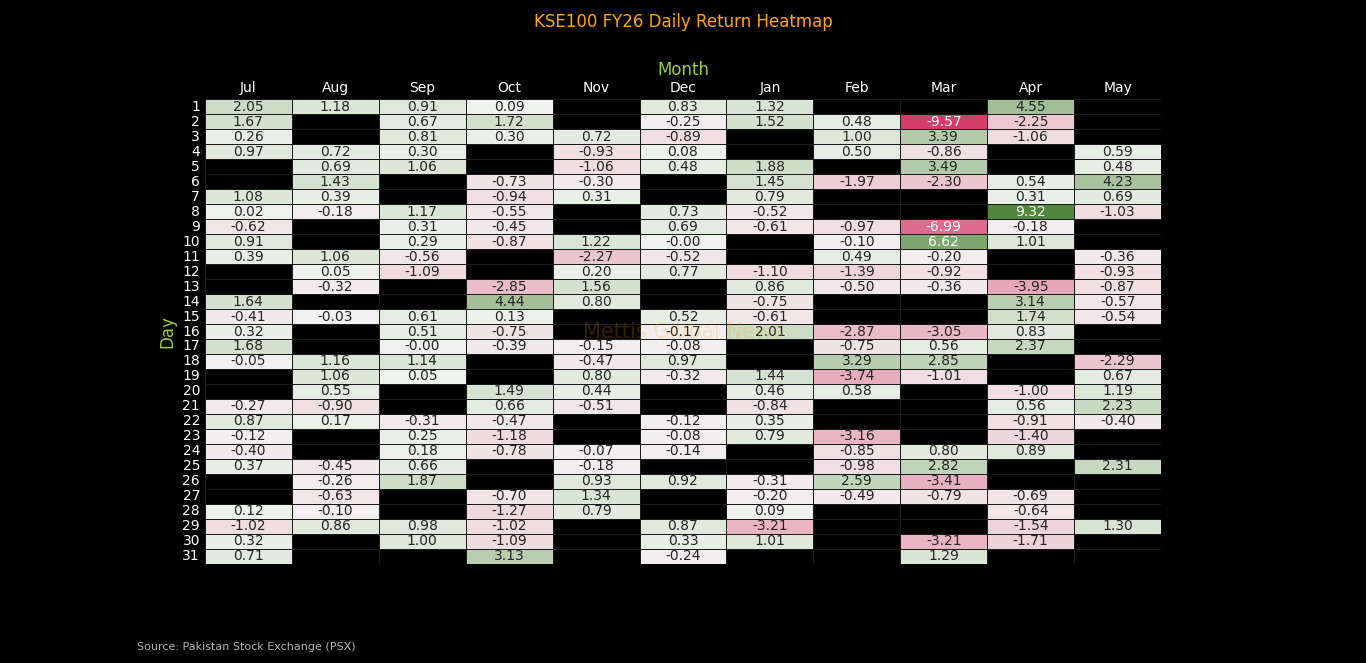

The KSE-100 Monthly & FY PKR Return Heatmap and the KSE-100 Monthly & FY USD Return Heatmap together offer one of the most complete pictures of Pakistani equity market performance across time.

The PKR heatmap measures returns purely in rupee terms, stripping out any currency effect. It reveals the raw index performance that a domestic investor would experience.

The standout observation from the historical data is the dominance

of FY2024, which delivered a remarkable 89.24% PKR return, the highest

full-year return on record, with virtually every month recording a green cell.

FY2025 followed with a 60.15% PKR return, reflecting sustained bullish

momentum into the following year.

By

contrast, FY2019 (−19.11%) and FY2023 (−0.21%) stand out as the weakest

periods, characterised by persistent red cells across multiple months. FY2018

(−10.00%) and FY2022 (−12.28%) also reflect difficult market environments.

For FY2026, the year-to-date PKR return stands at +38.48% through May 2026, with May alone contributing +6.73%. Historically, May has been a positive month for the KSE-100, the PKR heatmap shows green cells in May for 10 out of the 14 financial years displayed, making it one of the more consistently bullish months of the fiscal calendar.

The

USD heatmap applies the same index data but converts returns into US dollar

terms, incorporating the impact of PKR/USD exchange rate movements. This is the

lens through which foreign and overseas Pakistani investors evaluate

Pakistani equity performance, and it often tells a materially different story

from the PKR heatmap.

The

most striking divergence appears in FY2019, where a PKR return of −19.11%

translated into a devastating −38.60% USD return — losses nearly doubled by

simultaneous index weakness and sharp rupee depreciation. Similarly, FY2023's

near-flat PKR return of −0.21% masked a USD loss of −28.52%, driven almost

entirely by currency devaluation. These episodes underscore how currency risk

can dramatically amplify equity losses for dollar-based investors.

The reverse dynamic is equally evident. FY2024's USD return of 94.44% actually exceeded its PKR return of 89.24%, as the rupee held relatively firm during much of that fiscal year. FY2026's USD return of 41.09% similarly exceeds the PKR return of 38.48%, suggesting the rupee has modestly appreciated against the dollar on a net basis since July 2025 — a positive signal for foreign portfolio investors.

_20260601103127527_020f56.jpeg)

In May 2026 specifically, the PKR return of +6.73% and the USD return of +6.83% were almost identical, a spread of just 10 basis points.

This near-parity reflects the near-flat rupee during the month (PKR moved from approximately 278.77 to 278.50 against the USD), meaning foreign investors earned virtually the same return as domestic investors.

For a market that has historically suffered significant currency leakage, this convergence is a noteworthy positive for Pakistan's attractiveness to international capital.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 178,256.64 152.01M | 1.23% 2162.52 |

| ALLSHR | 107,706.10 457.89M | 1.10% 1175.21 |

| KSE30 | 53,195.17 54.71M | 1.36% 714.95 |

| KMI30 | 250,941.08 66.06M | 1.51% 3743.02 |

| KMIALLSHR | 69,018.01 236.35M | 1.23% 839.48 |

| BKTi | 50,913.82 15.01M | 1.18% 594.64 |

| OGTi | 34,811.27 4.40M | 1.44% 494.81 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 62,755.00 | 63,970.00 62,430.00 | -375.00 -0.59% |

| BRENT CRUDE | 83.36 | 84.55 81.55 | -4.57 -5.20% |

| RICHARDS BAY COAL MONTHLY | 107.75 | 0.00 0.00 | -0.50 -0.46% |

| ROTTERDAM COAL MONTHLY | 121.60 | 0.00 0.00 | -0.40 -0.33% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 79.48 | 81.30 78.78 | -5.19 -6.13% |

| SUGAR #11 WORLD | 14.65 | 0.00 0.00 | -0.01 -0.07% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|