AI Economy to hit $3tr by 2030

MG News | July 06, 2026 at 10:45 AM GMT+05:00

July 06, 2026 (MLN): Global AI revenues are projected to reach $3.1tr by 2030, split across an application layer of co-pilots, agents and customer service tools worth $990bn, an intelligence layer of text, image and video models worth $495bn, and an enabling layer of GPUs, memory, data centre infrastructure and cloud worth $1.65tr.

AI adoption and monetization continue to accelerate and

justify the scale of capital spending already underway. This is according to

"The AI Economy: A Roadmap," a report by UBS Chief Investment

Office's Jason Draho, Andrew Dubinsky and Paul Hsiao.

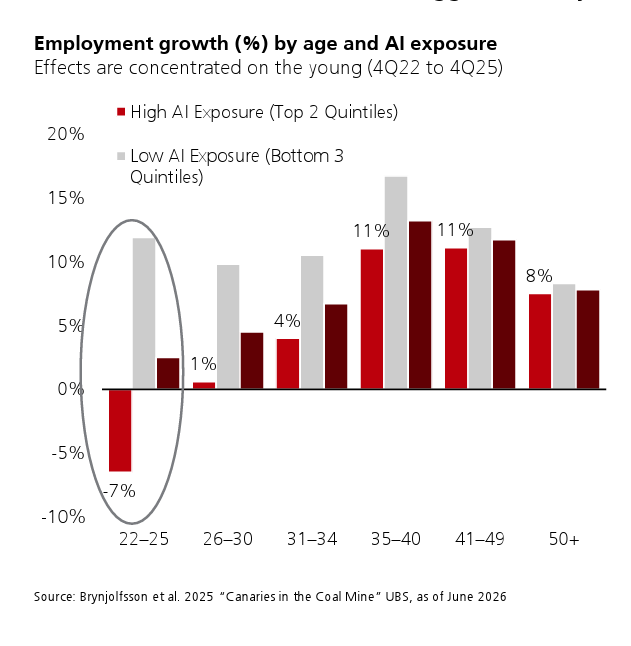

Employment growth for workers aged 22-25 in roles with high

AI exposure contracted by roughly 7% between the fourth quarter of 2022 and the

fourth quarter of 2025, even as their low-exposure peers in the same age

bracket grew nearly 12% over the same period.

Every other age cohort recorded positive employment growth

regardless of exposure level, making young workers the clearest casualty of AI

adoption so far.

Part of the divergence may be tied to a decline in remote,

AI-exposed entry-level positions rather than automation alone, based on

separate research into remote-work patterns and youth unemployment.

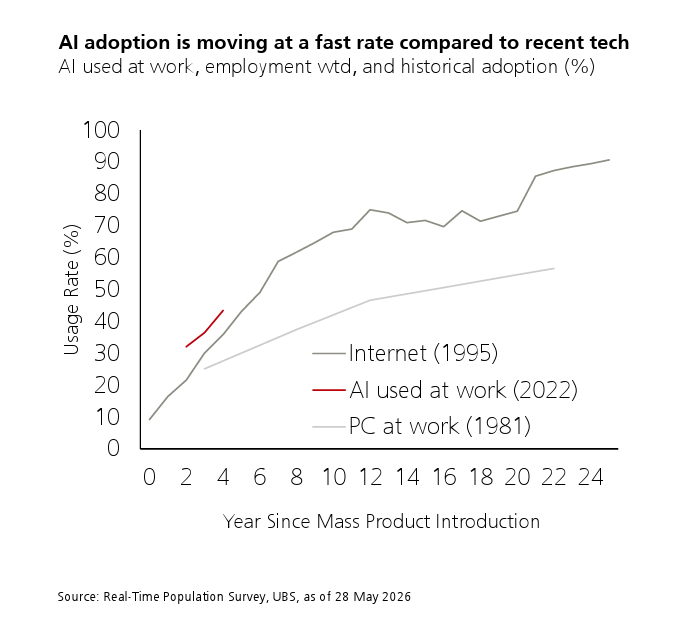

Workplace use of artificial intelligence has crossed 40% and

is rising at roughly 11 percentage points a year, a pace ahead of both the

personal computer and the internet at the same stage after their mass

introduction.

About 13% of workers are now everyday AI users, up 2

percentage points year-on-year, while firm-level adoption stands near 20% on a

count-weighted basis, led by large firms and by information technology,

finance, and professional services industries.

The eventual labour market impact of AI depends on four

linked factors: how many tasks are exposed to AI tools, how quickly firms adopt

them, and whether the technology substitutes for or augments workers.

Estimates of job-level automation risk vary widely by

methodology, ranging from 4% of jobs under a framework combining high AI

exposure with low adaptive capacity, to as much as 19% when considering both

current and anticipated tools with 50%-plus task exposure.

Exposure is highest in computer/math occupations, followed

by sales, business, and office/administrative roles, and rises with educational

attainment: median exposure among jobs requiring a college degree is 45%, more

than triple the 14% median for jobs that do not require one.

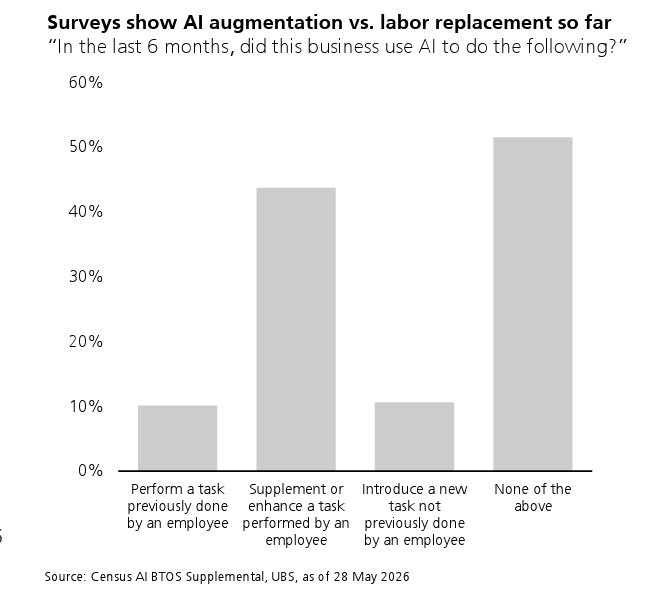

Despite that exposure, business surveys indicate AI is still

overwhelmingly supplementing rather than replacing labour.

Asked whether AI had been used in the last six months to

perform a task previously done by an employee, only about 10% of firms said

yes, compared with roughly 44% reporting it was used to supplement or enhance

an existing task, and just over half reporting no use at all.

The correlation between AI adoption or exposure and job growth has been low in aggregate: AI-exposed technology employment has been falling relative to private service-sector jobs excluding healthcare and AI-tech, while employment in AI-exposed construction categories tied to data centre build-out has been growing faster than the rest of the construction sector.

Total factor productivity growth has typically added to

aggregate labour demand through final-demand and upstream effects that outweigh

direct labour displacement, and periods of strong productivity growth,

including the late-1990s IT integration era that averaged 2.5% annual

productivity growth, have been neutral to positive for real worker

compensation, according to OECD-based research cited in the report.

Behind the labour market data sits an investment cycle the

report describes as an AI "flywheel": productivity gains drive

adoption, adoption lifts compute demand, compute demand requires capex, and

falling costs from that capex unlock further use cases, restarting the cycle.

Energy supply and financing access are identified as the two most likely

constraints on the loop.

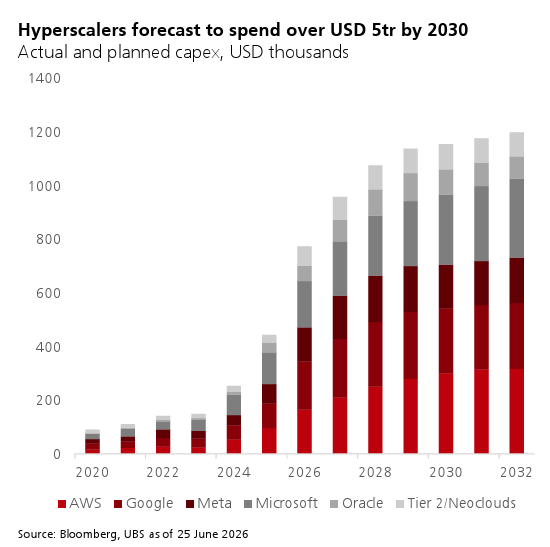

Hyperscaler capital expenditure across AWS, Google, Meta,

Microsoft, Oracle and Tier 2/neocloud providers is forecast to exceed $5tr

cumulatively by 2030, with AI-related capex now accounting for a growing share

of total US fixed investment and technology-sector capex rising to roughly 37%

of total S&P 500 capital spending.

Financing this build-out is drawing on the full capital

structure, from free cash flow and public equity down to private credit and

infrastructure funds, with big-five hyperscaler senior unsecured bond issuance

surging past $150bn in 2026.

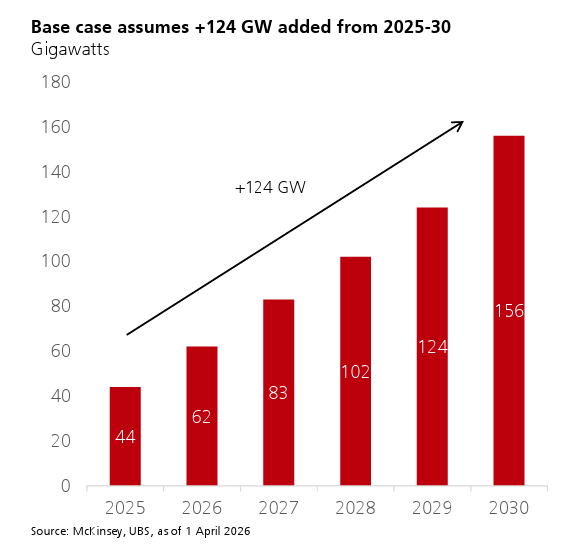

Data centre energy demand is expected to rise from 44

gigawatts in 2025 to 156 gigawatts by 2030, with associated energy investment

estimated at $300bn in a base case, ranging from $200bn in a bear scenario to $600bn

in a bull scenario.

Token usage, the basic unit of AI compute, has risen from

near zero in October 2024 to nearly 8tr tokens by late 2025, with enterprise

adoption governed by a straightforward cost-benefit calculation between the

price of running AI models and the value of time saved on tasks.

AI's ultimate transformation of the economy hinges on the

size of the productivity gains it can generate, since the same level of

adoption produces a larger GDP boost the bigger those gains are.

US labour productivity has grown at 2.7% annualised over the

past three years, more than a percentage point above the 2010s average, though

the gain is attributed mainly to post-pandemic normalisation rather than AI,

since adoption rates and efficiency gains have so far been too small to explain

the increase.

Academic studies of AI's effect on task-level productivity

find gains of roughly 25-30% across functions including coding, professional

writing, customer service and business consulting, but translating these

micro-level gains into macroeconomic productivity growth is contested.

Estimates of the aggregate annualised boost range from as

low as 0.1 percentage points to as high as 2.8% points across separate studies

by the OECD, IMF and Goldman Sachs.

Two distinct effects are possible: improved worker

efficiency, considered highly likely, would level-shift output higher without

permanently raising the productivity growth rate, while a boost to the pace of

innovation itself, considered less likely, would sustainably raise the growth

rate rather than simply shifting the output level.

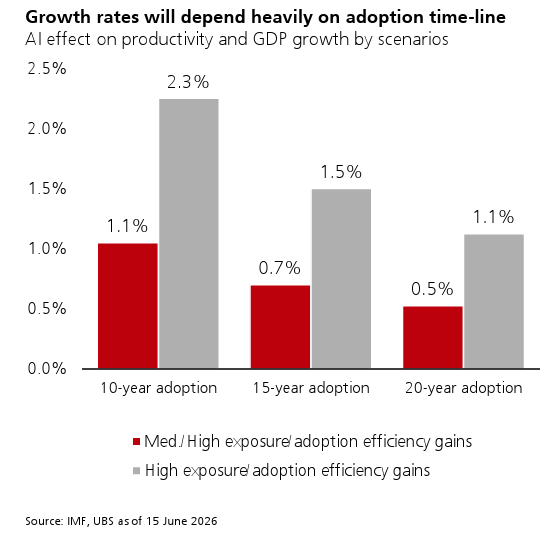

The scale of any GDP effect is highly sensitive to

assumptions about adoption timelines and efficiency gains: annual GDP growth

effects range from as low as 0.5% under a 20-year adoption timeline to 2.3%

under a 10-year timeline with high exposure and efficiency gains.

AI is currently lifting both growth and inflation, keeping

the macro regime in reflation as a byproduct, but its longer-run effect is

expected to shift toward disinflationary growth as productivity gains outweigh

the inflationary impulse from capex and input costs.

AI-related investment contributed an estimated 25 basis

points to GDP growth on average in 2025, though a substantial portion of that

capex is spent on imported chips and equipment, which drags on net exports and

reduced the net AI contribution to GDP to roughly zero over the course of 2025.

On inflation, AI is adding upward pressure in the near term

through three channels: rising prices for data centre inputs such as memory and

batteries, higher software and digital goods prices, with computer software and

accessories prices up 14% year-on-year, and increased electricity demand

pushing up utility costs faster than broader core inflation.

Medium to long term, these pressures are expected to ease as

high input prices incentivise supply expansion and productivity gains begin to

outweigh inflationary effects.

The impact on monetary policy is similarly two-sided.

Current growth and inflation impulses are keeping the Federal Reserve from

cutting rates as quickly as it otherwise might, while structural disinflation

and potential labour market weakening from AI displacement are reasons to

expect rate cuts further out.

On the neutral rate, higher productivity growth should raise

it, but increased AI-related labour market and income uncertainty could raise

household savings rates and reduce it, with the net effect assessed as likely a

modestly higher neutral rate depending on the pace of adoption.

On fiscal policy, a one-percentage-point AI productivity

shock could reduce the US deficit-to-GDP ratio by up to roughly 2 percentage

points and debt-to-GDP by up to 18 percentage points by 2035, though weaker

labour force participation could partly offset these gains.

Regulatory risk is also rising: survey data shows majorities

across generations, from 81% of Gen Z to 57% of the Silent Generation, believe

AI will reduce job opportunities, while opposition to local data centre

construction exceeds support across Republican, independent and Democratic

respondents alike.

AI is now treated as a macro factor affecting every asset

class rather than a standalone investment theme. In equities, a group of

AI-linked mega-cap names now makes up more than 30% of S&P 500 market

capitalisation, raising concentration risk, while a clear performance gap has

opened between perceived AI leaders and laggards.

In rates, AI capex is lifting growth and inflation in a way

that tilts the Federal Reserve toward hiking rather than cutting in the near

term, while long-end Treasury yields have historically fallen around major AI

model release announcements.

In credit, hyperscalers have issued more than $100bn of

investment-grade debt in 2026 alone, and high-yield technology sector spreads

have widened relative to the broader US corporate average as investors demand a

premium for financing the capex build-out.

In currencies, the US dollar has shown a strengthening

correlation with AI-linked equity performance, showing capital inflows tied to

US dominance in AI investment relative to China and the European Union.

In commodities, surging compute demand combined with limited

near-term supply flexibility has lifted industrial metals and energy prices, a

trend expected to continue as data centre energy usage rises more than fourfold

by 2030 relative to 2020 levels.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 177,623.88 478.02M | -0.36% -638.45 |

| ALLSHR | 107,472.27 954.45M | -0.34% -365.17 |

| KSE30 | 53,131.56 115.62M | -0.41% -216.11 |

| KMI30 | 250,814.93 150.64M | -0.28% -695.43 |

| KMIALLSHR | 68,971.49 608.41M | -0.29% -202.37 |

| BKTi | 50,769.48 23.80M | -0.58% -295.25 |

| OGTi | 34,999.12 6.26M | -0.71% -249.30 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 63,820.00 | 64,810.00 62,680.00 | -1145.00 -1.76% |

| BRENT CRUDE | 83.70 | 88.06 82.52 | -4.66 -5.27% |

| RICHARDS BAY COAL MONTHLY | 105.75 | 0.00 0.00 | -0.50 -0.47% |

| ROTTERDAM COAL MONTHLY | 120.00 | 0.00 0.00 | 0.25 0.21% |

| USD RBD PALM OLEIN | 1,175.00 | 1,175.00 1,175.00 | 0.00 0.00% |

| CRUDE OIL - WTI | 78.93 | 82.43 77.78 | -3.68 -4.45% |

| SUGAR #11 WORLD | 14.56 | 14.70 14.50 | -0.02 -0.14% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|