Weekly Market Roundup

By Rafay Malik | December 07, 2024 at 12:04 PM GMT+05:00

December 07, 2024 (MLN): Pakistan stocks were unstoppable this week, breaking records every day and extending their gains to close above the 109,000 level.

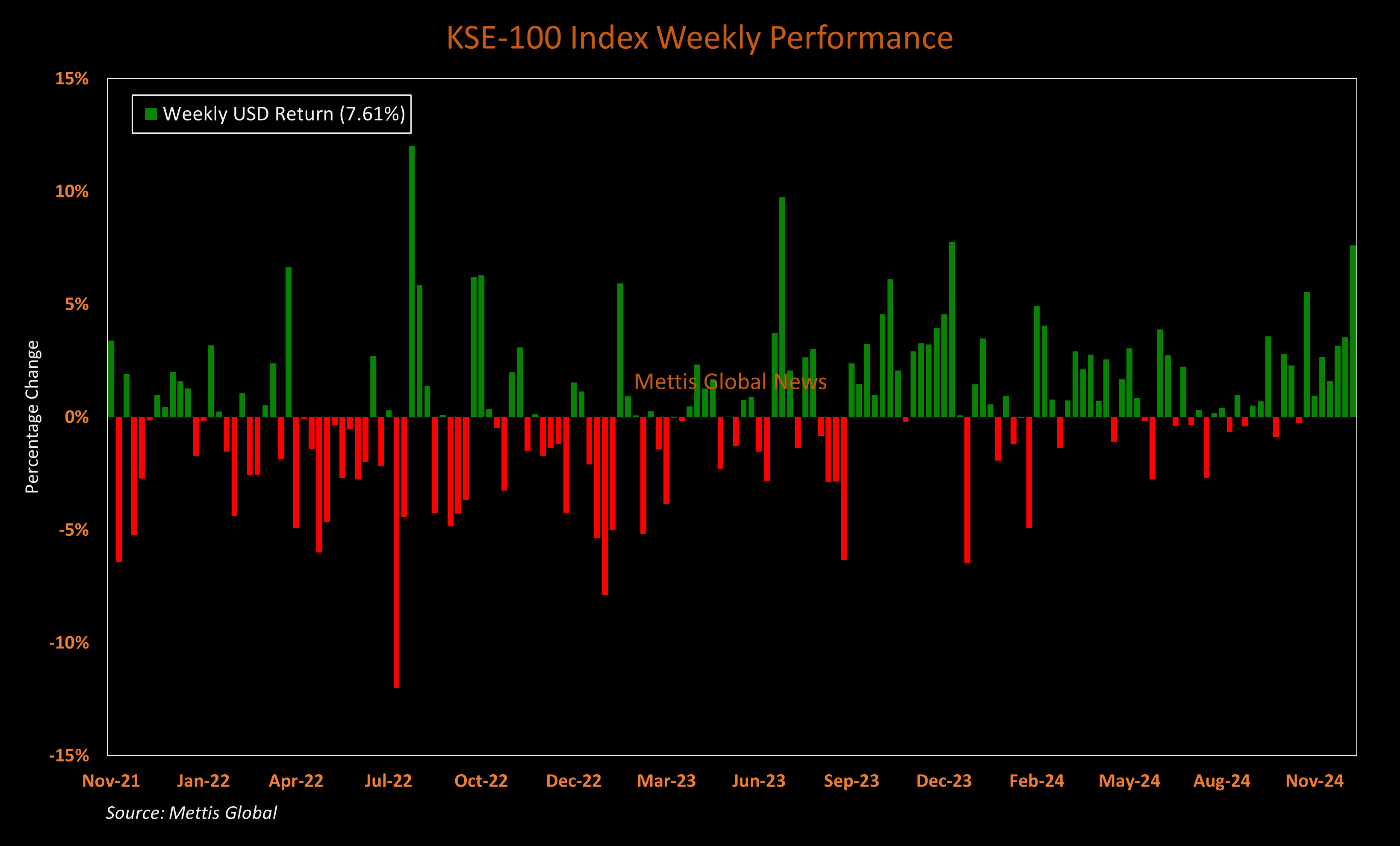

The benchmark KSE-100 posted a weekly gain of 7.59% or 7,697pts, the seventh addition to the rally and the highest weekly gain since April 2020, when it surged 12.49%.

In USD terms, the index posted a remarkable rise of 7.61%. Notably, a USD percentage gain of this magnitude or higher was last seen a year ago.

The index traded within a wide yet consistently positive range of 7,557 points, reaching a high of 109,478 (+8,120.77) and a low of 101,921 (+563.89).

The surge was buoyed by strong expectations that another rate cut would be announced at the upcoming Monetary Policy Committee (MPC) meeting.

Pakistan’s inflation for November eased significantly to 4.9%, marking the lowest price increase since April 2018 and falling well within the central bank's target range of 5-7%.

Market consensus suggests a potential rate cut of 150 to 250 basis points, giving bulls another cheerful moment.

During the week, the central bank reported that its reserves surpassed the $12bn mark, standing at the highest level since March 2022.

Meanwhile, Saudi Arabia extended the term for the deposit of $3 billion maturing on December 05, 2024 for another year to help maintain the foreign currency reserves of Pakistan and contribute to the economic growth of the country.

Another positive sign for the economy was that the central government's total debt saw its second consecutive drop, down 0.66% to Rs69.11 trillion in October 2024.

Positive economic triggers strengthened the confidence of the bulls and surged the KSE-100 index calendar year's returns to 74.62%, while for the fiscal year, they stand at 39.02%.

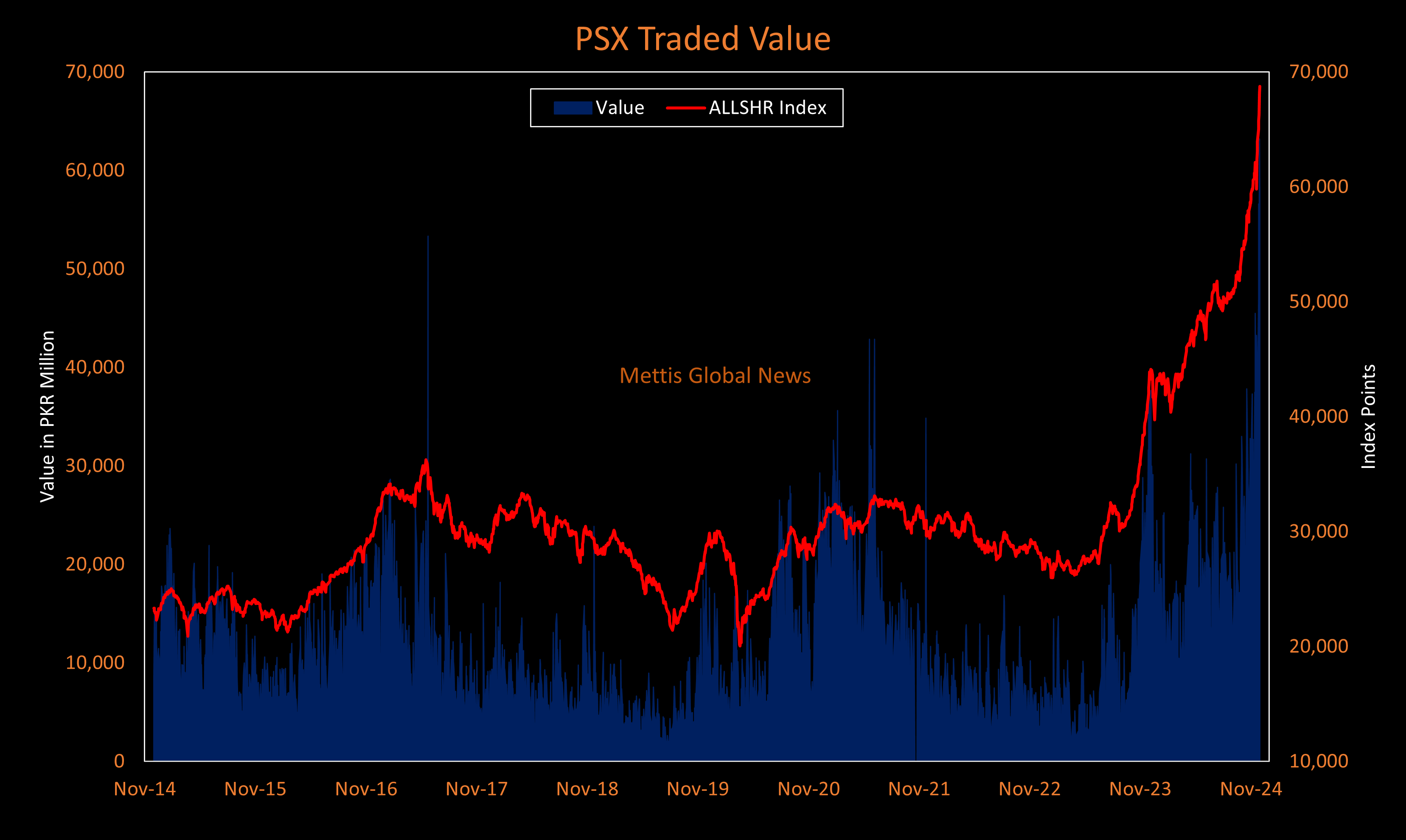

The local bourse achieved another milestone as its average traded volume surged to an all-time high of 1.68bn, substantially up by 72% compared to last week. Meanwhile, traded value also peaked to Rs54.97bn, rising 49.19% WoW.

Market capitalization jumped by $3.5bn or 7.55% to $49.84bn over the week. In PKR terms, market capitalization stood at Rs13.86 trillion.

Top Index Movers

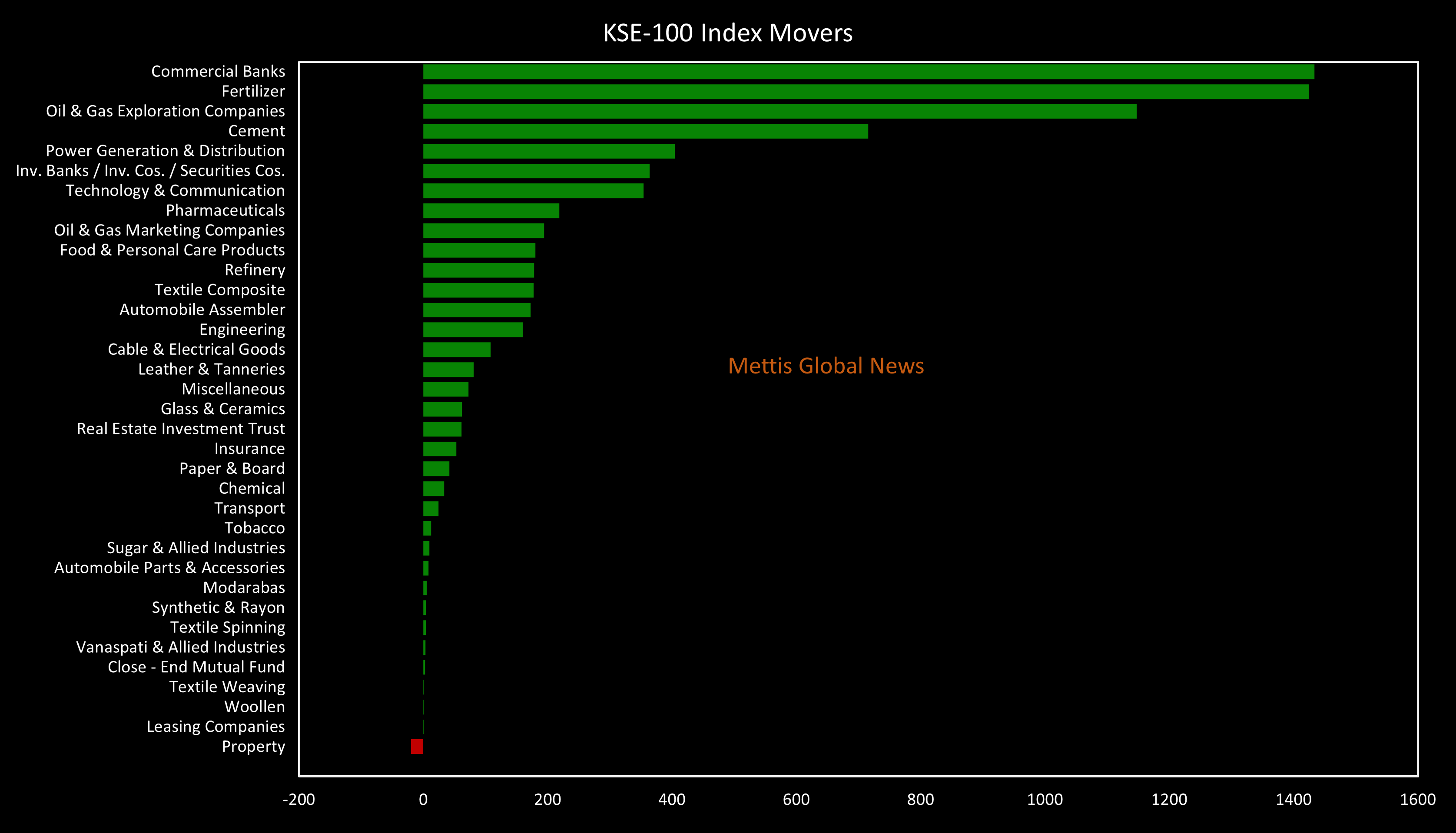

Sector-wise, top positive contributors were Commercial Banks (+1,433.51pts), Fertilizer (+1,424.27pts), Oil & Gas Exploration Companies (+1,148.05pts), Cement (+715.71pts), and Power Generation & Distribution (+404.84pts).

Contrary to that, negative contributions came from only one sector —property—which dragged the benchmark index down by a modest 20 points.

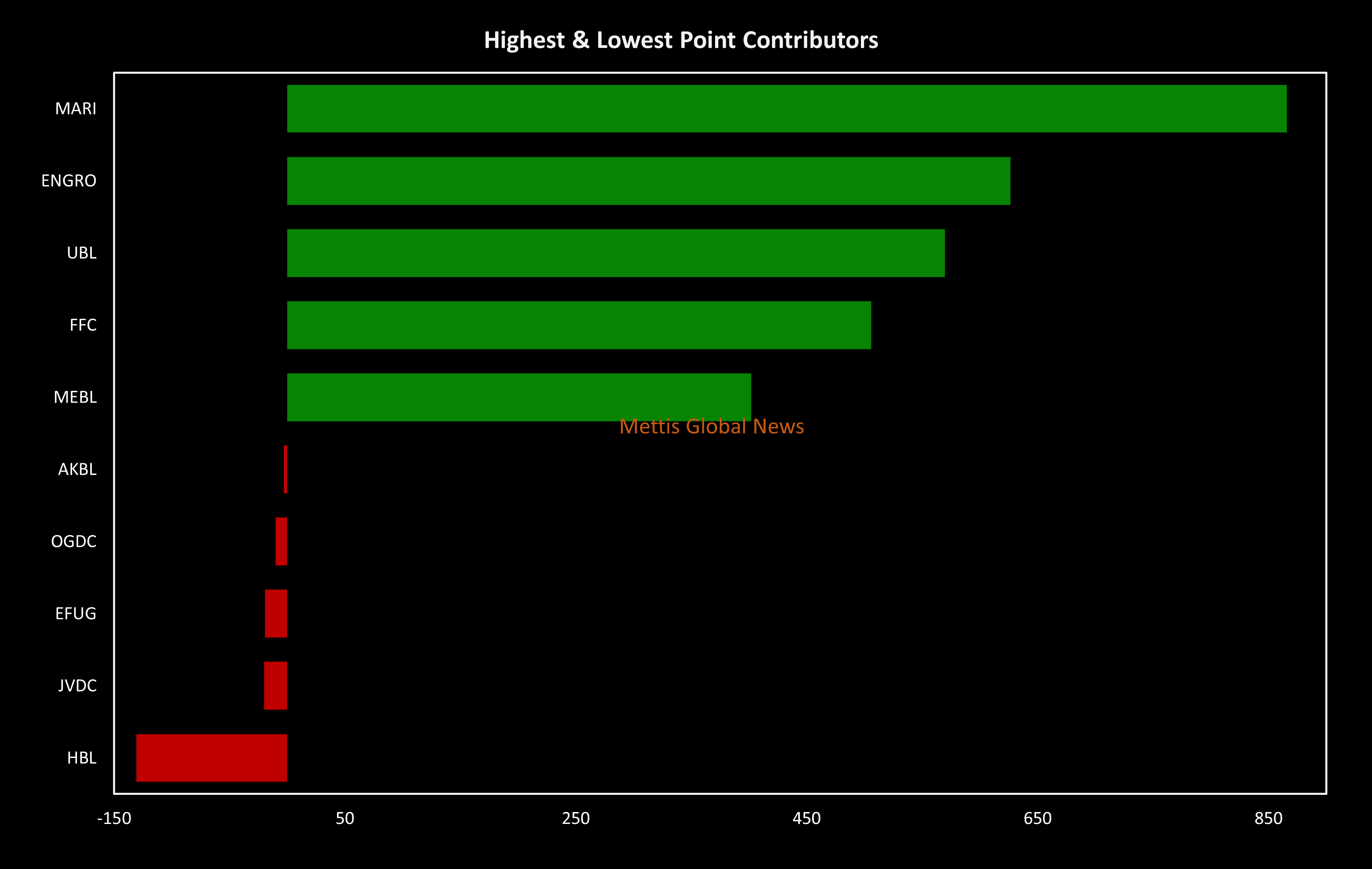

The best-performing stocks during the week were MARI (+865.79pts), ENGRO (+626.42pts), UBL (+569.54pts), FFC (+505.57pts), and MEBL (+401.7pts).

Whereas, the worst-performing were HBL (-130.75pts), JVDC (-20.06pts), EFUG (-19.40pts), OGDC (-9.88pts), and AKBL (-2.97pts).

FIPI/LIPI

Foreign investors were once again net sellers during the week, dumping a significant $14.18m worth of equities.

Flow-wise, the leading sellers were Foreign Corporates with a net sale of $8.3m. Their most substantial sales activity was in Food and Personal Care Products, amounting to $3.69m.

On the other hand, mutual funds were the dominant buyers, with a net investment of $43.95m. They allocated the majority of their capital, $8.4m, to Oil and Gas Exploration Companies.

Copyright Mettis Link News

Related News

.png)

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 132,678.00 96.26M |

-0.54% -725.19 |

| ALLSHR | 83,008.62 534.62M |

-0.22% -179.44 |

| KSE30 | 40,370.07 34.73M |

-0.69% -281.39 |

| KMI30 | 190,999.16 39.10M |

-0.56% -1084.76 |

| KMIALLSHR | 55,734.95 273.41M |

-0.20% -112.74 |

| BKTi | 36,179.99 6.10M |

-0.67% -242.88 |

| OGTi | 28,272.76 7.18M |

-0.58% -164.85 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 109,240.00 | 109,545.00 108,625.00 |

25.00 0.02% |

| BRENT CRUDE | 70.09 | 70.10 69.85 |

-0.06 -0.09% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

2.05 2.15% |

| ROTTERDAM COAL MONTHLY | 106.65 | 106.65 106.25 |

0.50 0.47% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.27 | 68.29 67.78 |

-0.06 -0.09% |

| SUGAR #11 WORLD | 16.15 | 16.37 16.10 |

-0.13 -0.80% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|