Towards the end of Hawkish Cycle

Muhammad Ghazanfar Sakrani | July 30, 2023 at 11:43 AM GMT+05:00

July 30, 2023 (MLN): The State Bank of Pakistan (SBP) is all set to announce the policy rate on July 31, 2023. This would be the first Monetary Policy Committee (MPC) meeting after availing the Stand by Arrangement (SBA) from IMF which helped avert the default chances in the near term as well as unlocked funding from friendly countries.

This led to the increase in SBP’s forex reserves from $4.52 billion in the first week of July to $8.73 billion in the week ending July 14, 2023.

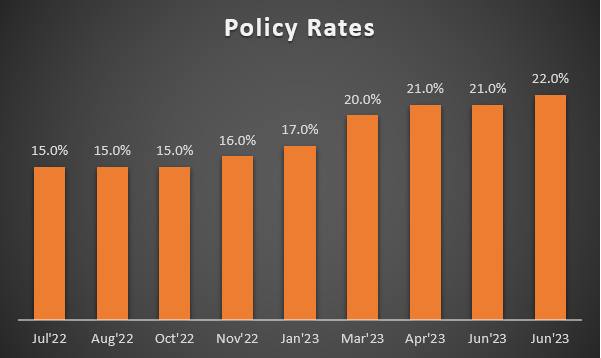

The SBP convened its last MPC meeting on June 26 where it announced a hike of 100bps in the policy rate which was maintained at 21% in the meeting held just a couple of weeks back.

The emergency meeting convened before the Eid holidays was viewed as a means to comply with the preconditions of IMF in the ‘decider week’, consequently leading to the signing of SBA between the country and the fund.

The upcoming monetary policy remains interesting with market participants divided over a status quo or a hawkish stance. As per a survey conducted by CFA Society Pakistan, almost 44% of the participants expect up to a 100bps hike whereas 42% of participants believe the status quo would prevail. However, none of the participants as per the survey expect a dovish stance.

The central bank is faced with a tough call. On one hand, IMF in its country report recommends keeping a tighter monetary policy to counter inflation, re-anchor expectations, and encourage external sector rebalancing through the exchange rate. On the contrary, inflation has started to decelerate since June’23 when CPI was recorded at 29.4% compared to May’23 CPI recorded at 38%.

This decrease was mainly observed due to the high base effect. CPI in the month of July is also expected to be recorded at lower levels of 25%-27% with further reduction in the upcoming months.

Consequently, the decline in inflation rates may lead to positive real interest rates on a forward-looking basis which justifies the stance of participants expecting a status quo.

The policy rate is already recorded at the highest levels which is haunting the businesses. The higher cost of borrowing makes the export sector uncompetitive, leads to increased unemployment, and can also increase the proportion of non-performing loans (NPLs) of the banks.

The high cost of borrowing prevented the private sector from approaching the debt market as bank lending to the private sector shrunk by 98% to a paltry Rs28 billion from July 1 to May 19 FY2023 compared to Rs1.414 trillion borrowed a year ago. The country also witnessed a negative GDP growth for FY2023 as per the IMF report.

Any further hike in the policy rate would make things worse for the business community already suffering from the slowdown for more than a year.

The case study of Pakistan and its monetary policy in recent times remains very interesting. The central bank of the country is raising interest rates to counter inflation. However, this may work well for countries where inflation is demand-driven.

In a country like Pakistan, this policy doesn’t seem to work as inflation is mostly cost-push, exacerbated by high food prices amid floods and high prices of petroleum products along with energy prices. These components make up a significant portion of CPI. The supply of commodities cannot be enhanced by raising interest rates.

This ineffectiveness is apparent from the fact that the SBP raised policy rates by 600bps from Oct 22-May’23; however, at the same time, CPI increased from 26.3% in Oct’22 to 38% in May’23.

Another interesting observation stems from the fact that an increase in policy rates by the SBP indirectly increases inflation for the consumers rather than decelerating it. Let’s examine how this double whammy sets in. When SBP increases the policy rates, the government’s financing costs increase as the government remains the largest borrower.

As per the Ministry of Finance (MoF), the government’s budget deficit during the first nine months of FY2023 increased by Rs3.5 trillion owing to high debt servicing and defense. The government borrowing for budgetary support increased by 93.8% during the Jun-May FY2023 clocking in at Rs3,043.3 billion compared to Rs1,570.0 billion during the same period last year. The public debt at March end 2023 stood at Rs59,274 billion, up by 33.6% compared to Rs44,366 billion public debt recorded at March end 2022.

The government also plans to borrow a record Rs11.1 trillion rupees through t-bills and bonds in the first quarter of FY2024. Mark-up expenses are also expected to grow by 85% in FY2024 reaching Rs7.3 trillion.

This enhanced financing cost increases the government’s current expenditure which in turn leads to an amplified budget deficit demanding for raise in taxes to cover the shortfall. High taxes on electricity, gas, and fuel prices further burden the masses by increasing inflation and the cycle of raising interest rates leading to rising inflation continues.

Increased taxes also increase the cost of doing business and makes the products less competitive in international markets which further dampens exports and jeopardizes the economic growth.

The upcoming monetary policies remain interesting with SBP to decide whether to move towards a dovish stance in anticipation of declining inflation or keep the high rates intact. Another survey conducted by CFA Society Pakistan reveals that almost 70% of market participants expect the policy rate to remain in the range of 20%-24%.

Considering the inflation figures, the SBP may be towards the end of its hawkish cycle with the policy rate to retreat at most from the next calendar year.

Copyright Mettis Link News

Related News

| Name | Price/Vol | %Chg/NChg |

|---|---|---|

| KSE100 | 134,299.77 290.06M |

0.39% 517.42 |

| ALLSHR | 84,018.16 764.12M |

0.48% 402.35 |

| KSE30 | 40,814.29 132.59M |

0.33% 132.52 |

| KMI30 | 192,589.16 116.24M |

0.49% 948.28 |

| KMIALLSHR | 56,072.25 387.69M |

0.32% 180.74 |

| BKTi | 36,971.75 19.46M |

-0.05% -16.94 |

| OGTi | 28,240.28 6.19M |

0.21% 58.78 |

| Symbol | Bid/Ask | High/Low |

|---|

| Name | Last | High/Low | Chg/%Chg |

|---|---|---|---|

| BITCOIN FUTURES | 118,140.00 | 119,450.00 115,635.00 |

4270.00 3.75% |

| BRENT CRUDE | 70.63 | 70.71 68.55 |

1.99 2.90% |

| RICHARDS BAY COAL MONTHLY | 97.50 | 0.00 0.00 |

1.10 1.14% |

| ROTTERDAM COAL MONTHLY | 108.75 | 108.75 108.75 |

0.40 0.37% |

| USD RBD PALM OLEIN | 998.50 | 998.50 998.50 |

0.00 0.00% |

| CRUDE OIL - WTI | 68.75 | 68.77 66.50 |

2.18 3.27% |

| SUGAR #11 WORLD | 16.56 | 16.60 16.20 |

0.30 1.85% |

Chart of the Day

Latest News

Top 5 things to watch in this week

Pakistan Stock Movers

| Name | Last | Chg/%Chg |

|---|

| Name | Last | Chg/%Chg |

|---|